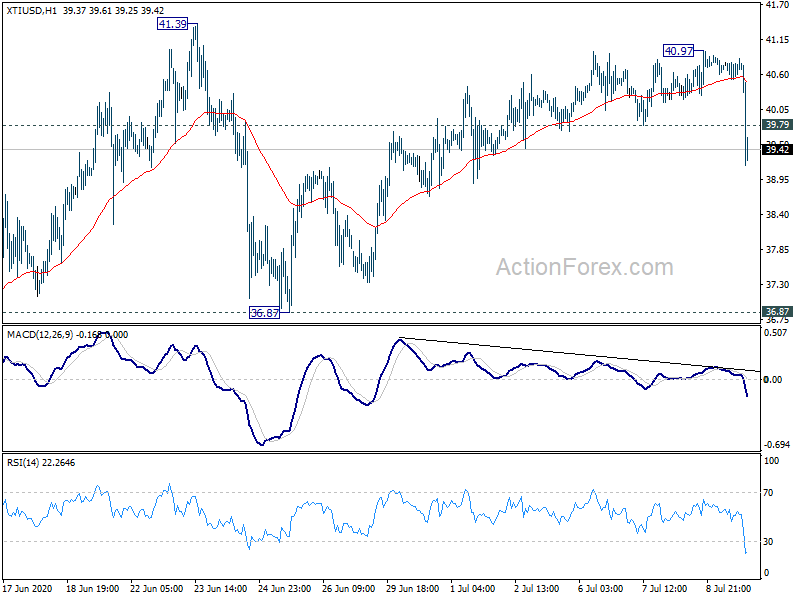

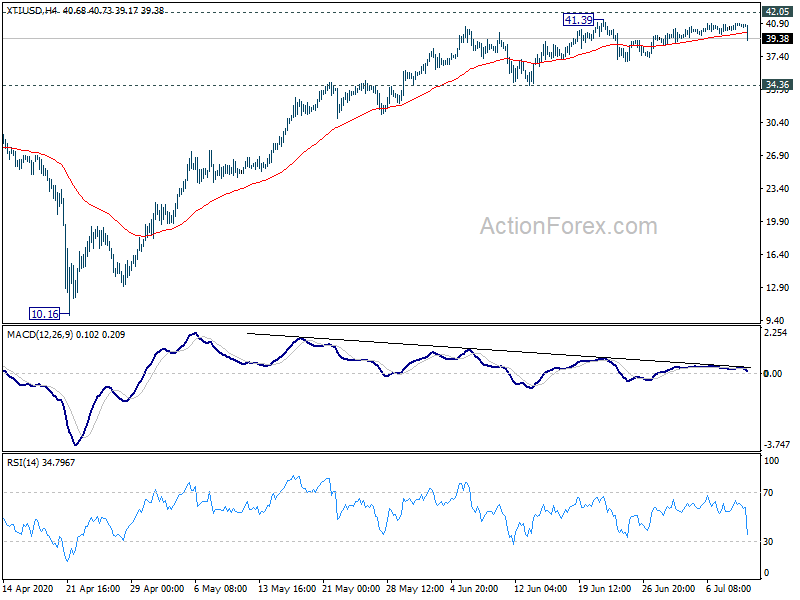

Both oil price and DOW drop notably in early US session today. WTI is now back at around 39.50 after hitting as high as 40.97 yesterday. Our view is unchanged that price actions from 41.39 are forming a corrective pattern. The break of 39.79 minor support argues that the second leg might have completed. Further fall would now be seen back towards 36.87 support level.

DOW is currently trading down over -500 pts or at around -2%. It’s now getting more likely that price actions from 24843.18 are merely a sideway pattern, as the second wave in the pattern from 27580.21. It’s still a bit far but focus is back on 24971.03 support. Firm break there should extend the corrective fall from 27580.21 to 38.2% retracement at 24002.18.

New Zealand BusinessNZ PMI dropped to 52.8 and production dipped again

New Zealand BusinessNZ Performance of Manufacturing Index dropped to 52.8 in June, down from 54.4. BusinessNZ’s executive director for manufacturing Catherine Beard said that the slow-down in expansion was mainly due to ongoing drops in a key sub-index.

“Production (51.8) experienced another decrease in expansion levels for June, which meant it was down to its lowest point since January 2017. On a positive note, the other key sub-index of New Orders (57.1) remained in healthy territory, which at least should feed through to production levels in the coming months.

In addition, the proportion of positive comments in June (51.7%) decreased from May (55.1%), and very similar to February (51.4%). Those who provided negative comments typically noted a general downturn and uncertainty in the market”.

BNZ Senior Economist, Craig Ebert said that “broadly speaking, the PMI has settled down into a trend-like pace this year, averaging 53.8 (excluding April’s spike). This is after outperformance through most of 2017, when it averaged 56.2”.

Full BusinessNZ Performance of Manufacturing Index release.