Live Comments

Gold eyes 5,300 after surviving shakeout, but longer-term reset will take more time

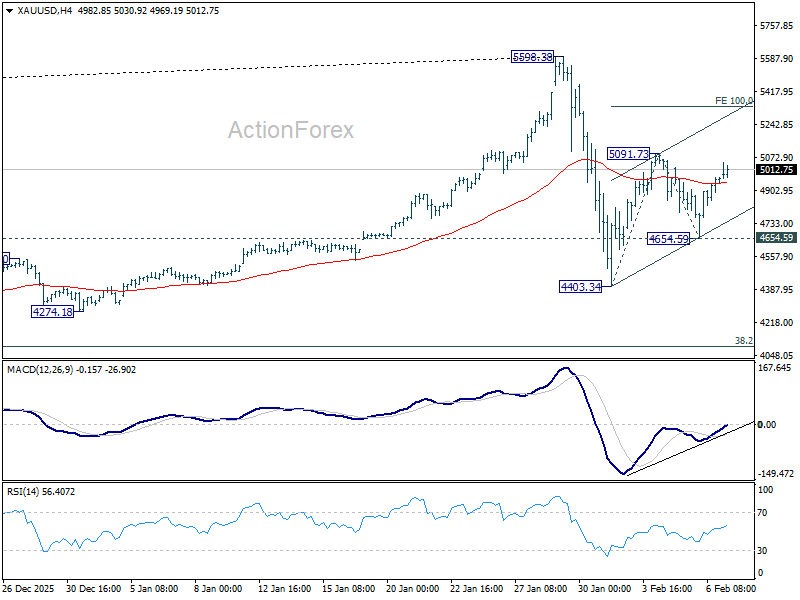

After two volatile weeks, Gold appears to have regained its footing. Prices have stabilized around the 4,400 area and have since pushed back above 5,000, signalling that the first wave of profit taking has likely run its course. The sharp pullback from the record high was forceful, but the subsequent price action suggests sellers have become less aggressive, opening room for a tradable rebound in the near term.

Technically, the decline from 5,598.38 to 4,403.34 is seen as the initial phase of a broader medium-term correction. That phase now appears complete. Price action since 4,403.34 marks the second phase of this corrective process, which can unfold in a more complex and time-consuming manner rather than a simple straight-line rebound.

For short-term traders, the outlook is constructive. The exhaustion of the initial profit-taking wave raises the prospect of further upside in the near term. As long as pullbacks remain contained, momentum favours additional gains before sellers re-emerge in force.

In this context, 4,654.49 serves as the key tactical line. Any near-term dip should be contained above this level. On the upside, decisive break of 5,091.73 would open the way toward 100% projection of 4,403.34 to 5,091.73 from 4,654.59 at 5,342.98. . That level is a natural target for the current rebound and represents the upper boundary of what short-term traders should reasonably expect from this phase.

However, strength into the 5,340–5,598 zone is likely to attract another round of profit taking, particularly from longer-term holders. That supply should cap near-term upside and prevent Gold from immediately resuming its larger bull trend.

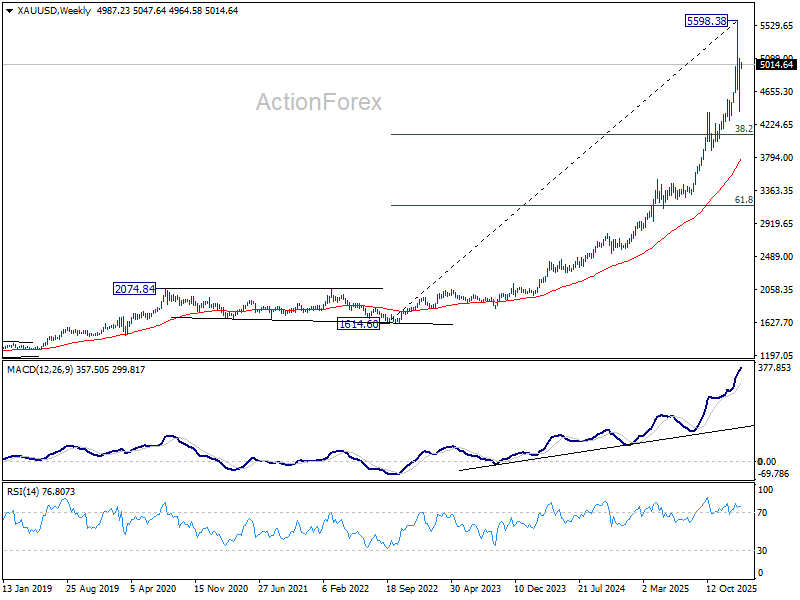

For long-term investors, patience is essential. The current rebound is not viewed as a trend resumption but as part of a broader consolidation correcting the entire advance from 1,614.50 (2022 low). While the long-term structure remains bullish, the market still needs time to absorb prior gains.

Any deeper pullback is expected to find stronger demand near the 4000–4400 accumulation zone, reinforced by 38.2% retracement of 1,614.60 to 5,598.38 at 4,076.57. Until fresh catalysts emerge, that area is the preferred zone for rebuilding long positions ahead of the next major uptrend, likely months rather than weeks away.

Nikkei celebrates Takaichi landslide, USD/JPY faces post-election reality check

Japan enters the week riding a powerful post-election wave after equities surged to fresh record highs. Nikkei jumped above 57,000 following Prime Minister Sanae Takaichi’s historic election victory. Although the index has since retreated modestly, it is still holding on to the bulk of its gains, up nearly 4.5% on strong domestic risk appetite.

Takaichi’s win was historic in scale. Her Liberal Democratic Party captured 315 seats in the lower house, its strongest showing ever, and together with coalition partner Ishin now controls 351 seats. That gives the ruling bloc a two-thirds supermajority, allowing it to override the upper house and advance legislation with unprecedented ease.

That supermajority significantly strengthens Takaichi’s hand. It opens the door not only to aggressive fiscal measures but also to constitutional changes, while easing the path for defense spending increases amid a more challenging global environment. For equity investors, political uncertainty has collapsed, and policy execution risk has been sharply reduced.

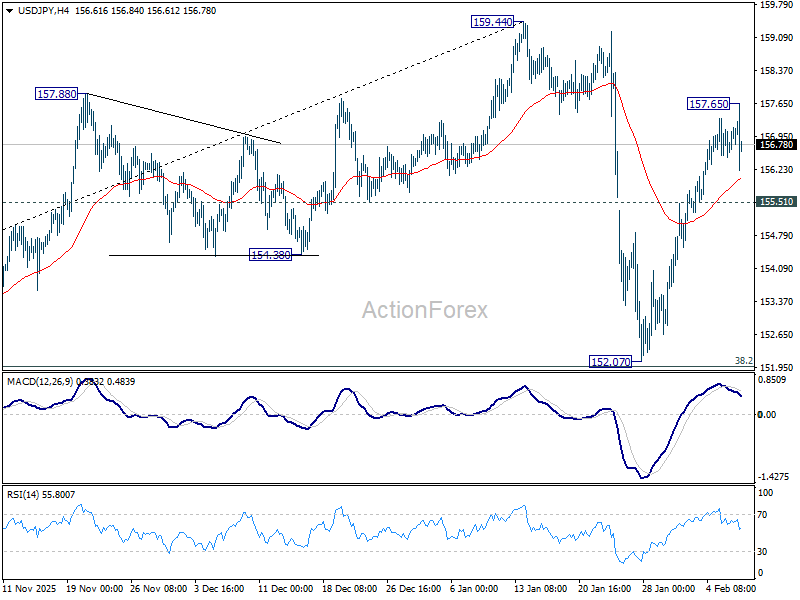

Yen, however, has not followed equities in a straight line. USD/JPY initially jumped at the Asian open but quickly retreated. Traders remain alert to the risk of intervention should the Yen weaken too sharply, limiting follow-through on election-driven selling. This leaves currency markets in wait-and-see mode. With the election result now fully realized, the question is whether Yen selling momentum can re-emerge as focus shifts back to fiscal expansion, or whether the pair has already priced in the bulk of the political shock.

Technically, momentum is already showing signs of fatigue. USD/JPY’s 4H MACD is falling below its signal line, indicating that the rebound from 152.07 is losing steam. That move is viewed as the second leg of a broader corrective pattern from 159.44. While further gains remain possible as long as 155.51 holds, strong resistance is expected near 159.44 high. A clear break below 155.51 would argue that the third leg of the correction is already underway, reopening the path back toward the 152.07 support ahead.

Japan’s nominal pay accelerates to 2.4% in December, but real wages still negative

Japan’s real wages fell -0.1% yoy in December, marking the 12th consecutive monthly decline, though the contraction was the smallest seen in 2025. While the pace of erosion is clearly slowing, the data underline how inflation continues to outpace pay gains for households.

Nominal wages rose 2.4% yoy, extending a 48-month streak of increases, but the outcome fell short of expectations for a 3.0% rise. The acceleration from November’s 1.7% growth points to improving momentum, but not yet at a pace sufficient to deliver sustained real income gains.

Breaking down the components, base salaries rose 2.2% yoy, picking up from November's 1.7% yoy. Overtime pay increased 0.9%, slightly slower than the prior month's 1.2%. Special payments, largely winter bonuses, rose 2.6% up from 1.5%.

Attention now shifts firmly to the upcoming spring wage negotiations. The key questions are whether large firms can again deliver pay hikes above 5% for the third straight years, and whether those gains finally spill over to smaller companies.