BoE Andrew Bailey, in an interview with Bloomberg TV, suggested that the central bank could soon hit a plateau in its cycle of rate hikes. However, he underscored the need for clear evidence before making such a call.

“We are approaching a point when we should be able to in a sense rest in terms of the level of rates,” Bailey stated. However, he was quick to caution that BoE hadn’t seen sufficient evidence yet to make that determination. “We have to be evidence driven,” he emphasized.

When queried if BoE was nearing a pause in rate increases, Bailey responded, “Well, I’m going to say I hope we are because this is the 12th consecutive increase in rates.” He reiterated, however, BoE’s dependence on tangible data, adding “we will be guided by the evidence as it comes to us.”

Bailey’s comments reflect a careful balancing act. While he hints at a potential easing in rate hikes, he firmly anchors this possibility to empirical data, thereby preventing premature conclusions. He also clarified that BOE is not “giving a direction one way or the other” on rates and that their future moves would be “shaped by the evidence.”

Germany Economy Minister Peter Altmaier said he expected the economy to start growing again from October or November. Also, he noted that the European Commission has given its approval for the country’s Economic Stabilization Fund.

With the fund’s key framework approved, the would has capital of up to EUR 600B for offsetting the coronavirus pandemic’s impact on German economy. The ministry is already in information talks with some 50 firms about tapping assistance from the fund.

In a speech, BoC Governor Tiff Macklem said current inflation, close to 5%, is “too high”. But that is “not the result of generalized excess demand in the Canadian economy”. Inflation “largely reflects global supply problems, most of which stem from the pandemic”. As the pandemic recedes, “conditions around the world should normalize, taking pressure off global goods prices.”. BoC expects inflation to “come down relatively quickly” in H2 2022 to 3% by the end of the year.

Macklem added, “to get inflation the rest of the way back to its 2% target, we need a significant shift in monetary policy”. The economy will need “higher interest rates to moderate growth in spending and bring demand in line with supply”, and “keep inflation expectations well anchored”. And, “we signalled with unusual clarity that Canadians should expect a rising path for interest rates.”

Global spread of China’s Wuhan coronavirus continues to accelerate as it’s now affecting 90% countries and territories. Total infections reached 98424, with 3386 deaths. China’s increase in cases continue stabilize at low level, with 143 new cases yesterday to accumulated total of 80552. 30 new deaths were reported, bringing total to 3042.

South Korea remains the most affected country with 6284 cases and 40 deaths. Italy’s cases surged to 3858, with 148 deaths. Iran reported a total of 3513 cases with 108 deaths. Other countries are also catching up, including Germany (545 cases), France (423 cases, 7 deaths), Japan (364 cases, 6 deaths), Spain (282 cases, 3 deaths), USA (226 cases, 13 deaths), Switzerland (120 cases, 1 death), Singapore (117 cases), UK (116 cases, 1 death) and Hong Kong (105 cases). Sweden (94 cases), Norway (91 cases), (Netherlands 82 cases), will break 100 level soon.

WHO Director-General Tedros Adhanom Ghebreyesus urged the world to pull out “all the stops” top slow the spread of the coronavirus. He said, “This is not a drill. This is not the time for giving up. This is not a time for excuses. This is a time for pulling out all the stops.” “Countries have been planning for scenarios like this for decades. Now is the time to act on those plans.” There is a global online petition calling for resignation of Tedros for breaking WHO’s political neutrality. More than 440k people have signed.

China’s Vice Premier Liu He was interviewed by the CGTN TV network after the trip to Washington.

He noted the trade talks were “constructive, positive and fruitful”, and “very practical”. There were “lots of concrete consensus” reached in terms of trade and structural issues.

The concrete issues include agricultural and energy exports to China. Liu added that “the Chinese market will become the largest world market. So to increase imports, re-balance the economy and expand domestic demand is our national policy.” Also, Liu said “we expand our domestic market and increase imports because we want to serve the needs of our people, our economy, and our growth. Speeding reform and growth by means of opening up is a very important national strategy. It worked for China for the past 40 years, and we will continue down that path.”

But he emphasized that “exporting to China or making China buy more, one must make the Chinese consumers happy”.

Also, Liu noted that the strongest demand from both sides were to stop imposing more tariffs on each other’s products. And he said “this time, both sides pledged to stop the trade war and develop good relations, be it in trade or in investment. I think this is a major demand from both countries.”

Liu also pointed to resolutions of some of “our misunderstands from the past. He hailed that “these meetings will not just help bilateral economic and trade relations, but overall ties. It’s good for people in both countries.”

Mario Draghi, President of the ECB,

Luis de Guindos, Vice-President of the ECB,

Frankfurt am Main, 13 September 2018

INTRODUCTORY STATEMENT

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council, which was also attended by the Commission Vice-President, Mr Dombrovskis.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, we will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of this month. After September 2018, we will reduce the monthly pace of the net asset purchases to €15 billion until the end of December 2018 and we anticipate that, subject to incoming data confirming our medium-term inflation outlook, we will then end net purchases. We intend to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of our net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The incoming information, including our new September 2018 staff projections, broadly confirms our previous assessment of an ongoing broad-based expansion of the euro area economy and gradually rising inflation. The underlying strength of the economy continues to support our confidence that the sustained convergence of inflation to our aim will proceed and will be maintained even after a gradual winding-down of our net asset purchases. At the same time, uncertainties relating to rising protectionism, vulnerabilities in emerging markets and financial market volatility have gained more prominence recently. Significant monetary policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term. This support will continue to be provided by the net asset purchases until the end of the year, by the sizeable stock of acquired assets and the associated reinvestments, and by our enhanced forward guidance on the key ECB interest rates. In any event, the Governing Council stands ready to adjust all of its instruments as appropriate to ensure that inflation continues to move towards the Governing Council’s inflation aim in a sustained manner.

Let me now explain our assessment in greater detail, starting with the economic analysis. Euro area real GDP increased by 0.4%, quarter on quarter, in the second quarter of 2018, following growth at the same rate in the previous quarter. Despite some moderation following the strong growth performance in 2017, the latest economic indicators and survey results overall confirm ongoing broad-based growth of the euro area economy. Our monetary policy measures continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by rising wages. Business investment is fostered by the favourable financing conditions, rising corporate profitability and solid demand. Housing investment remains robust. In addition, the expansion in global activity is expected to continue, supporting euro area exports.

This assessment is broadly reflected in the September 2018 ECB staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.0% in 2018, 1.8% in 2019 and 1.7% in 2020. Compared with the June 2018 Eurosystem staff macroeconomic projections, the outlook for real GDP growth has been revised down slightly for 2018 and 2019, mainly due to a somewhat weaker contribution from foreign demand.

The risks surrounding the euro area growth outlook can still be assessed as broadly balanced. At the same time, risks relating to rising protectionism, vulnerabilities in emerging markets and financial market volatility have gained more prominence recently.

According to Eurostat’s flash estimate, euro area annual HICP inflation was 2.0% in August 2018, down from 2.1% in July. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around the current level for the remainder of the year. While measures of underlying inflation remain generally muted, they have been increasing from earlier lows. Domestic cost pressures are strengthening and broadening amid high levels of capacity utilisation and tightening labour markets, which is pushing up wage growth. Uncertainty around the inflation outlook is receding. Looking ahead, underlying inflation is expected to pick up towards the end of the year and thereafter to increase gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion and rising wage growth.

This assessment is also broadly reflected in the September 2018 ECB staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.7% in 2018, 2019 and 2020, which is unchanged from the June 2018 Eurosystem staff macroeconomic projections.

Turning to the monetary analysis, broad money (M3) growth declined to 4.0% in July 2018, from 4.5% in June. Apart from some volatility in monthly flows, M3 growth is increasingly supported by bank credit creation. The narrow monetary aggregate M1 remained the main contributor to broad money growth.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations stood at 4.1% in July 2018, while the annual growth rate of loans to households stood at 3.0%, both unchanged from June.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing – in particular for small and medium-sized enterprises – and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed that an ample degree of monetary accommodation is still necessary for the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute more decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Regarding fiscal policies, the broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt is high and for which full adherence to the Stability and Growth Pact is critical for safeguarding sound fiscal positions. Likewise, the transparent and consistent implementation of the EU’s fiscal and economic governance framework over time and across countries remains essential to bolster the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

At a Fed conference overnight, Dallas Fed President Lorie Logan said that inflation appears to be “trending toward 3%”, a figure still above the 2% target.

Despite a cooling labor market, Logan highlighted that it remains “too tight,” implying that the job market’s strength could continue to put upward pressure on wages and, consequently, inflation.

Logan emphasized the need “see tight financial conditions in order to bring inflation to 2% in a timely and sustainable way”. She will be looking at “data” and “financial conditions” as the next meeting in December approaches.

With a particular focus on recent retracement in 10-year Treasury yield and broader financial conditions, Logan suggests these elements will play a pivotal role in shaping Fed’s forthcoming monetary policy decisions.

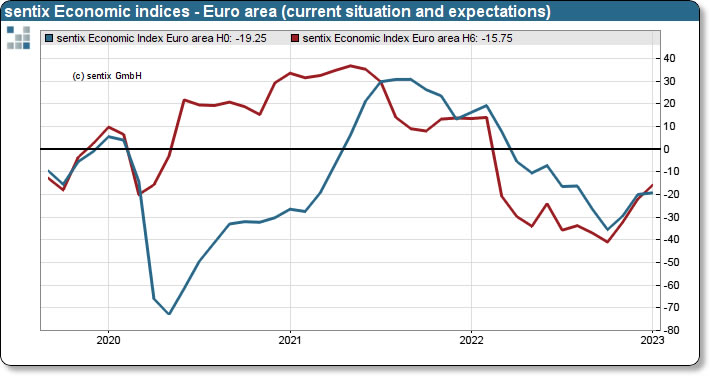

Eurozone Sentix Investor Confidence improved from -21 to -17.5 in January, slightly below expectation of -17.0. That’s nonetheless the highest since June 2022. Current Situation Index rose from -20.0 to -19.3, highest since last August. Expectations rose from -22.0 to -15.8, highest since last February.

Sentix said: “Investors are still assuming a recession, but it is expected to be much milder. The sharp economic downturn, which was expected by the majority of investors by October 2022, is therefore off the table (for now)…a

“Overall, the economic environment remains challenging. The latest increases should not be misinterpreted as a general turnaround. The risks of recession remain.”

In an interview with Reuters, ECB Governing Council member Robert Holzmann said that an interest rate cut in April is “not on my radar”. Instead, he highlighted June as a critical time for evaluating the bank’s next steps, emphasizing a commitment to data-driven decision-making regarding monetary easing.

“If the data allows it, a decision will be made,” he noted. “I don’t have an in-principle objection to easing in June, but I’d like to see the data first and I want to stay data-dependent.”

An intriguing aspect of Holzmann’s perspective is his consideration of Fed’s actions in relation to ECB’s. He mentioned, “If by June the data supports a strong case for a cut, and we’re a week before the Fed makes its decision, then it’s quite likely we’ll proceed, hoping the Fed follows suit.” However, if Fed doesn’t come along, “then it may reduce the economic impact of our move.”

Notably, Holzmann’s remarks signal a significant shift, especially considering his reputation as one of the more conservative voices within ECB, typically resistant to premature discussions of rate reductions. For him, the shift appears to be influenced by an increasingly benign inflation outlook. Also there were signs of economic fragility within Eurozone, which has been hovering on the brink of recession for multiple quarters.

Cleveland Fed President Loretta Mester said there’s more momentum in the economy then she anticipated. And, she’s been “upping” her forecasts, now expecting 2.75-3.00% for the year, and “probably close to 3%. She said that “the fiscal policy – the stimulus and the tax cuts – has been a positive for the economy in terms of demand growth and so that’s one of the factors.”

Mester also support the gradual path of monetary accommodation removal. But for now, it’s hard to judge whether the fed funds rate needs to go above neutral rate. But her neutral rate, at 3%, is higher than her fellows.

ECB rate decision and press conference is a main focus for today. No change is expected in monetary policy. And the main refinancing rate will be held at 0.00%.

As recent economic data pointed to further weakness in the Eurozone economy, ECB president Mario Draghi might turn a bit more cautious or even dovish in the press conference.

Market has already pushed back their expectations on the first rate hike to mid-2020. But, ECB is still unlikely to make any change to the forward guidance. That is, ECB will reiterate that interest rates will stay at present level at least through summer of 2019. ECB probably would wait for more incoming data before making such a change.

ECB Governing Council member Peter Kazimir said economic development in the Eurozone is “inline with the baseline scenario”. The central bank has “room to wait for hard data; which are reliable”, before making the decision on another policy move.

Kazimir also said ECB is “not obliged to use the whole envelope” of the EUR 1.3T Pandemic Emergency Purchase Programme (PEPP). For now, PEPP is “working” and it’s a very “appropriate response” to the crisis.

BoE Deputy Governor Dave Ramsden said in a speech that the news of coronavirus vaccine is “clearly encouraging”, even if there is still “some way to go” before delivery of vaccinations. He added that the central bank’s forecasts of recovery in Q1 2021 was already based on assumption of waning direct effect of the pandemic. Hence, vaccine development doesn’t immediately warrant an upward revision to forecasts.

Still, “assuming the recent positive developments do translate into delivery of vaccinations, then they could … bolster resilience and mitigate some of the risks of long-term scarring,”

Ramsden also reiterated that “negative rates remain in the toolbox” in the Q&A section. But, “they’re not something that we’re taking out of the toolbox and applying to the UK at present.”

US and China issued a joint statement on Saturday to conclude the trade talks with Chinese Vice Premier Liu He on May 17 and 18. There was no mentioning of any number, but the statement said there were “consensus on taking effective measures to substantially reduce” US trade deficit in goods with China. And, China agreed to “significantly increase purchase” of US goods and services.

Additionally, there would be “meaningful increases” in US agriculture and energy exports to China, “expanding trade” in manufactured goods and services, encouraging “two-way investment” with “fair, level playing field for competition”. China also pledged to work on laws and regulations on intellectually property protections.

The Chinese State-owned Xinhua news agency described the statement as “vowing not to launch a trade war against each other”.

Here is a graphical summary by Xinhua.

Full statement below:

THE WHITE HOUSE – Office of the Press Secretary

FOR IMMEDIATE RELEASE – May 19, 2018

Joint Statement of the United States and China Regarding Trade Consultations

At the direction of President Donald J. Trump and President Xi Jinping, on May 17 and 18, 2018, the United States and China engaged in constructive consultations regarding trade in Washington, D.C. The United States delegation included Secretary of the Treasury Steven T. Mnuchin, Secretary of Commerce Wilbur L. Ross, and United States Trade Representative Robert E. Lighthizer. The Chinese delegation was led by State Council Vice Premier Liu He, Special Envoy of President Xi.

There was a consensus on taking effective measures to substantially reduce the United States trade deficit in goods with China. To meet the growing consumption needs of the Chinese people and the need for high-quality economic development, China will significantly increase purchases of United States goods and services. This will help support growth and employment in the United States.

Both sides agreed on meaningful increases in United States agriculture and energy exports. The United States will send a team to China to work out the details.

The delegations also discussed expanding trade in manufactured goods and services. There was consensus on the need to create favorable conditions to increase trade in these areas.

Both sides attach paramount importance to intellectual property protections, and agreed to strengthen cooperation. China will advance relevant amendments to its laws and regulations in this area, including the Patent Law.

Both sides agreed to encourage two-way investment and to strive to create a fair, level playing field for competition.

Both sides agreed to continue to engage at high levels on these issues and to seek to resolve their economic and trade concerns in a proactive manner.

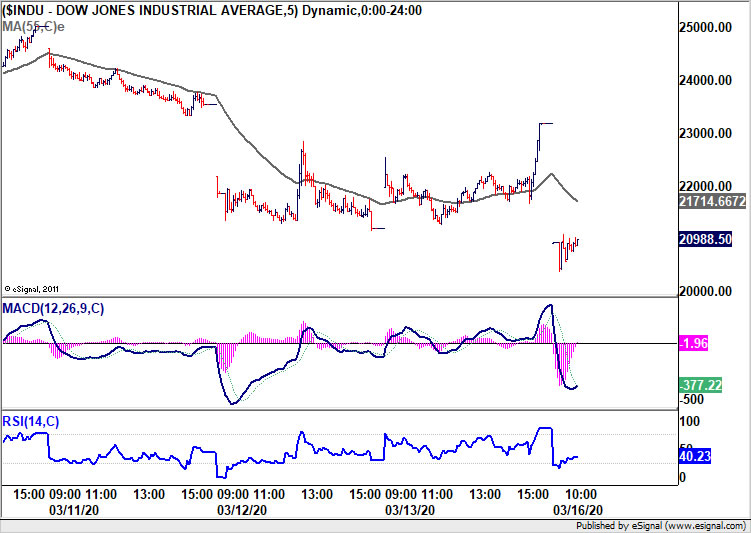

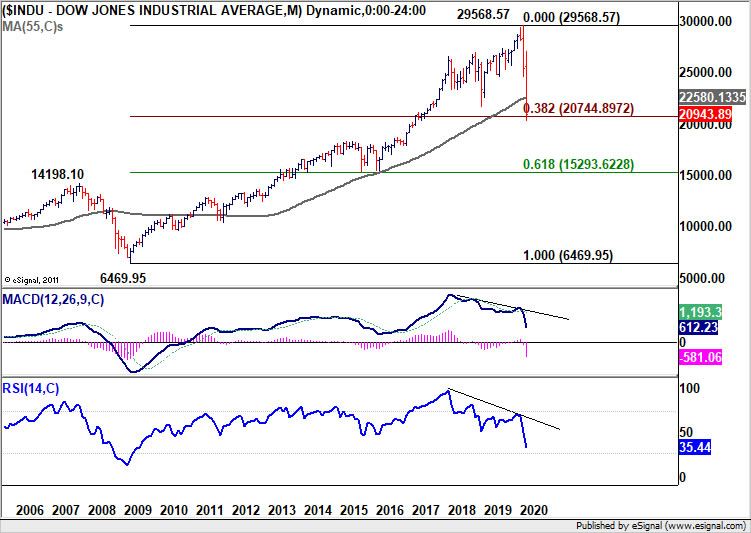

US stocks plunged deeply at open and hit the first circuit breaker immediately, halting trading of 15 minutes. There is no clear sign of any recovery after second open yet, with DOW currently down around -10%. We’d maintain DOW is close to a long term fibonacci support level of 38.2% retracement of 6469.96 to 29568.57 at 20744.89. And a rebound should be due.

However, sustained break of 20744.89 could trigger another round of position squaring. Decline could accelerate further to 61.8% retracement at 15293.62.

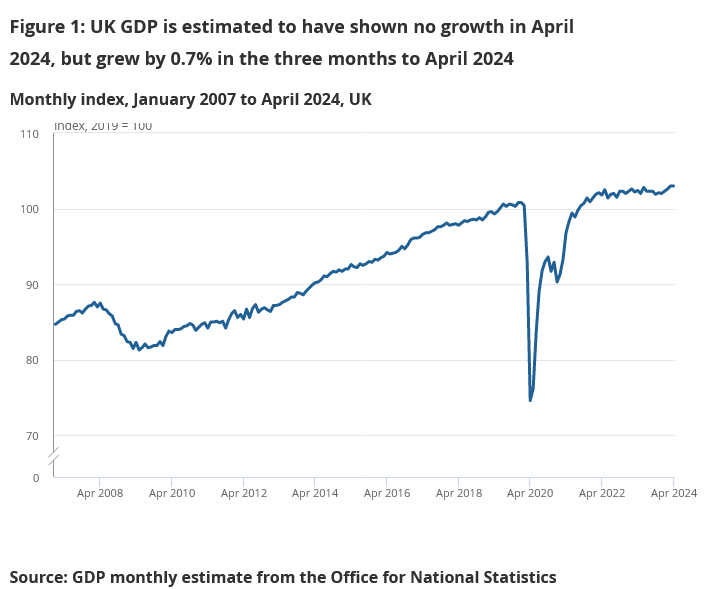

UK GDP showed no growth in April, aligning with market expectations. The data reveals a mixed picture, with certain sectors compensating for declines in others.

Services output grew by 0.2% mom, marking its fourth consecutive month of growth, underscoring the resilience of the services sector. Conversely, production output fell by -0.9% mom, reflecting ongoing challenges in the industrial sector. Construction output declined by -1.4% mom, continuing its downward trend for the third straight month.

Looking at the three-month period from February to April compared to the preceding three months from November to January, GDP grew by 0.7%. Within this period, services expanded by 0.9%, driven by consistent monthly gains. Production also showed a positive trend with a 0.7% increase, despite the monthly volatility. However, construction suffered a -2.2% decline, indicating sustained weakness in this sector.

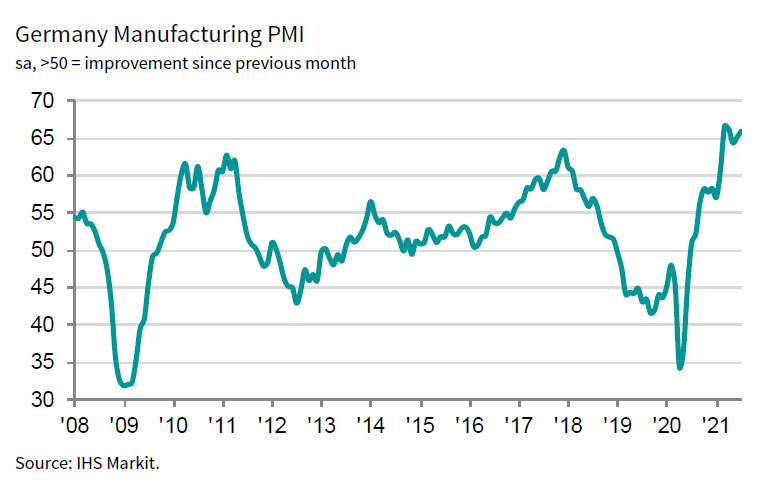

Germany PMI Manufacturing was finalized at 65.9 in July, up from June’s 65.1. The future was the third-highest since the survey began in 1996. There was survey-record increase in employment. Also, both price indices reached new record highs.

Trevor Balchin, Economics Director at IHS Markit, said: “Faster growth of new orders and employment boosted the German manufacturing sector in July… the latest survey results provided further evidence that output growth is being constrained by supply shortages….with overall demand for raw materials strengthening, input price inflation accelerated to a new survey record high. Consequently, the rate of output price inflation hit a new peak for the fifth month running.”

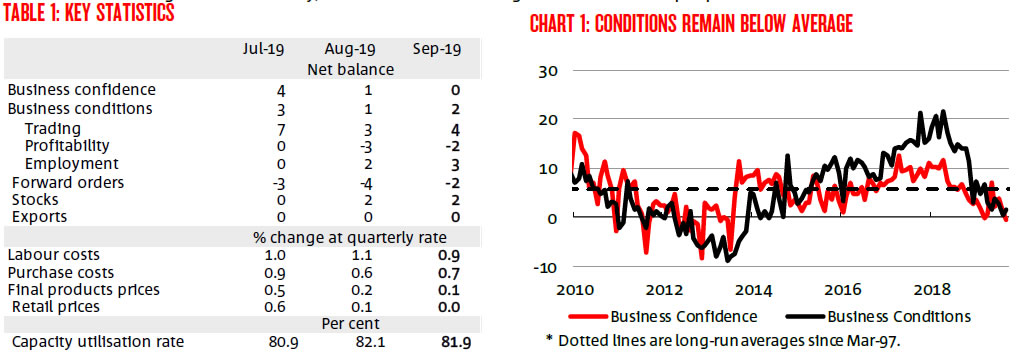

Australia NAB Business Confidence dropped to 0 in September, down from 1. On the other hand, Business Conditions improved to 2, up from 1. Looking at some details, Trading Condition rose from 3 to 4. Profitability Condition rose from -3 to -2. Employment Condition rose from 2 to 3.

Alan Oster, NAB Group Chief Economist “The results of the September survey suggest more of the same for the business sector. Conditions edged up, and confidence was marginally lower, but both remain below their long run average – well below the levels seen just over a year ago. This suggests that activity in the business sector has slowed and we fear the risk that this spreads to both investment and employment intentions”.

And: “We continue to watch the business sector closely – the housing downturn and the weakness in the retail sector are likely to continue to play out further, adding to private sector weakness in the economy. Rate cuts will help but will lag and with a weak consumer and higher global uncertainty, we are unlikely to see a material improvement in the short-term”

ECB said in its monthly economic bulletin that more recent information “points to a stabilisation in global growth”. In particular, survey-based data like PMI point to a “moderate recovery in manufacturing output growth and some moderation in services output growth”. Nevertheless, global recovery is projected to be “shallow”, reflecting moderation of growth in advanced economies and sluggishness in some emerging markets.

For Eurozone, however, ongoing weakness of international trade continues to weigh on manufacturing sector and is dampening investment growth. Survey-based data, while remaining weak overall, point to some stabilization of slowdown too.

Measures of underlying inflation in Eurozone “generally remained muted”. ECB added, that “market-based indicators of longer-term inflation expectations have remained at very low levels, while survey-based expectations also stand at historical lows.

New York Fed President John Williams said in a speech that US is “closing in on the longest economic expansion on record, unemployment is at historically low levels, and inflation is close to our 2 percent target “. And, from a “pure monetary policy perspective”, this is a “healthy economy”.

However, he also noted that Fed’s monetary policy decisions ” don’t affect the kinds of jobs that are created or who benefits from growth.”

BoE Bailey hints at possible pause in rate hikes

BoE Andrew Bailey, in an interview with Bloomberg TV, suggested that the central bank could soon hit a plateau in its cycle of rate hikes. However, he underscored the need for clear evidence before making such a call.

“We are approaching a point when we should be able to in a sense rest in terms of the level of rates,” Bailey stated. However, he was quick to caution that BoE hadn’t seen sufficient evidence yet to make that determination. “We have to be evidence driven,” he emphasized.

When queried if BoE was nearing a pause in rate increases, Bailey responded, “Well, I’m going to say I hope we are because this is the 12th consecutive increase in rates.” He reiterated, however, BoE’s dependence on tangible data, adding “we will be guided by the evidence as it comes to us.”

Bailey’s comments reflect a careful balancing act. While he hints at a potential easing in rate hikes, he firmly anchors this possibility to empirical data, thereby preventing premature conclusions. He also clarified that BOE is not “giving a direction one way or the other” on rates and that their future moves would be “shaped by the evidence.”