Mark Sobel, a former top US Treasury Official criticized Trump’s remark regarding Chinese currency manipulation as “woefully wide of the mark”. And, Trump’s focus on bilateral balances as “silly”. And, to suspect a country of currency manipulation, there are criteria of “material ‘excessive’ current account surplus, an undervalued currency, and ample and rising reserves”.

In an article titled “Trump wide of mark on ‘manipulation‘”, Sobel point to facts that “China’s current account surplus is falling to under 1% of GDP. The renminbi, hit by capital outflows between early 2015 and the end of 2016, rose sharply against the dollar up to April 2018. The renminbi trade-weighted index rose too. Since then, the renminbi has fallen on both measures, but the depreciation reflects the dollar’s strength across the board. There is little evidence of more than scant Chinese foreign exchange market intervention.”

He noted “a currency manipulating country should have a significant current account surplus”. And, “the US Treasury in its foreign exchange reports uses a 3% of GDP threshold.” While a currency manipulating country might also have an “undervalued currency” one should “look at a country’s real effective exchange rate, not its bilateral dollar rate.” Additionally, the country may intervene heavily in the markets, “buying dollars to hold its currency down, resulting in an increase in its foreign reserve holdings.” But there might be “good reasons” to do so such as building up of reserves. There are many useful gauges of reserve adequacy to examine – reserves/GDP; reserves/short-term maturing debt; reserves/imports.

Sobel also completed that “a focus on bilateral balances is silly, even if the US Treasury is required to do so by statute and the president seems obsessed with them. Such an emphasis neglects to consider that certain countries specialize in certain goods and hold comparative advantage in such spheres.”

Mark Sobel is US Chairman of OMFIF. He is a former Deputy Assistant Secretary for International Monetary and Financial Policy at the US Treasury and until earlier this year US representative at the International Monetary Fund.

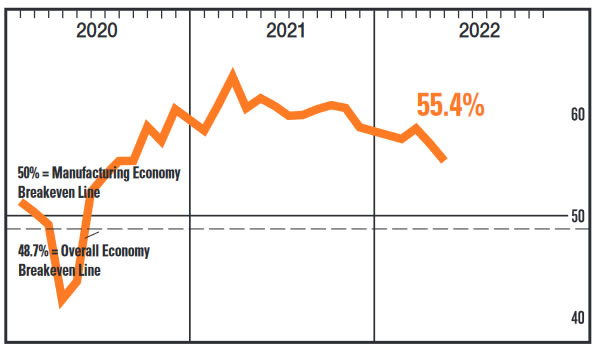

Australia AiG manufacturing rose to record 63.2, strength of recovery continued

Australia AiG Performance of Manufacturing Index rose to new record high at 63.2 in June, up from 61.8. That’s also the ninth consecutive month of rise. Looking at some more details, production dropped -3.8 to 60.7. Employment dropped -1.0 to 60.3. New orders jumped 5.7 to 70.6. Supplier deliveries rose 6.7 to 58.3. Exports rose 11.3 to 60.2. Input prices dropped -3.3 to 78.8. Selling prices rose 5.3 to 63.6.

Ai Group Chief Executive Innes Willox said: “The 2020-21 financial year closed on a high note for Australia’s manufacturing sector. Ai Group’s June Australian PMI pointed to record growth across the sector fueled by the fastest recorded pace of expansion in each of the food & beverages; machinery & equipment; building materials; and chemicals sectors. Production, employment, and sales exports were all higher than in May although the rate of acceleration generally eased. Exports of manufactured goods surged in June and new orders were also higher, pointing to the likelihood of further expansion in the months ahead. The strength of the recovery continued despite headwinds from COVID outbreaks and associated lockdowns and border restrictions, high freight costs and the widespread difficulties employers are experiencing in filling positions.”

Full release here.