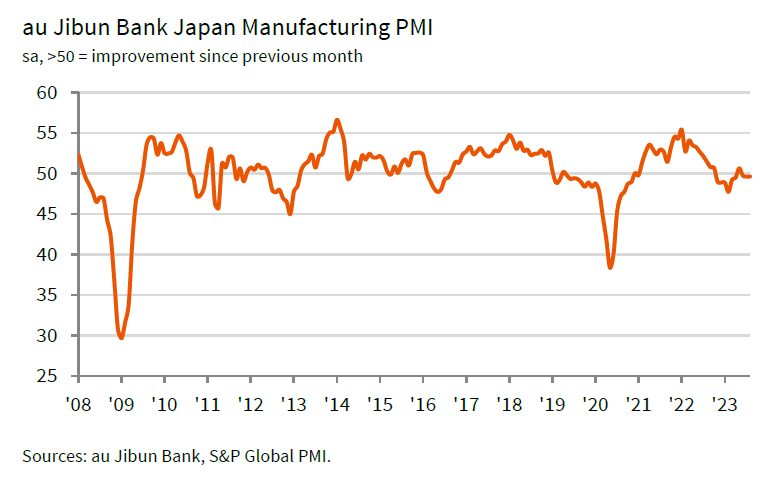

Japan’s industrial production took a hit in July, falling by a worse-than-expected -2.0% mom, versus consensus forecast of -1.4% mom. The seasonally adjusted production index stumbled to 103.6, based on 2020 base of 100.

Production was primarily pulled down by substantial drops in electronic parts and devices, which declined -by 5.1% mom. Also, production machinery output shrank by -4.8% mom, with semiconductor manufacturing equipment segment plunging a stark 16.4% mom. However, not all was grim. Production of automobiles showed a modest uptick of 0.6% mom, attributed to the easing of supply chain bottlenecks.

A Ministry of Economy, Trade, and Industry official remarked that the slump in output across various sectors was largely due to diminishing domestic and overseas orders. Consequently, METI has revised its assessment of industrial output from “showing signs of moderately picking up” to “fluctuated indecisively.”

Despite the grim industrial landscape, manufacturers surveyed by METI are optimistic, projecting a 2.6% rise in output for August and a 2.4% increase in September.

In contrast to the industrial sector’s lackluster performance, retail sales exhibited considerable strength. Sales surged 6.8% yoy in July, beating expectations of a 5.4% yoy increase. This marks the 17th consecutive month of expansion since March 2022. Additionally, retail sales increased 2.1% mom in July, recovering from a -0.6% mom decline in the previous month.

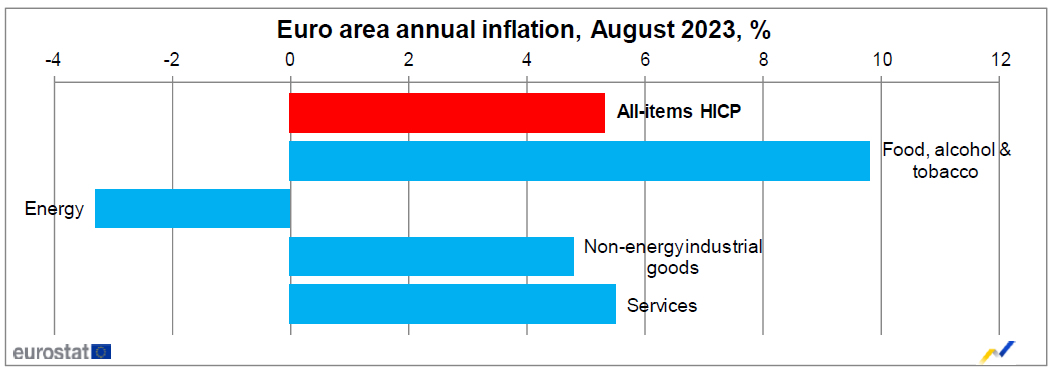

Eurozone PMI manufacturing finalized at 43.5, glimmers of hope despite persistent weakness

Eurozone PMI Manufacturing was finalized at 43.5, marking a slight uptick from July’s 38-month low of 42.7. Country-level readings reveal that Germany, the largest economy in the Eurozone, remains a cause for concern. Although it reported a two-month high, its PMI of 39.1 underscores its struggles. Spain (46.5), France (46.0), the Netherlands (45.9), Italy (45.4), and Austria (40.6) remained in contraction. Greece and Ireland were above 50-mark at 52.9 and 50.8 respectively.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, commented on the situation, stating, “These numbers aren’t as terrible as they might look at first glance.”

Despite the obvious weakness signaled by a PMI below 50, de la Rubia pointed out that all twelve subindices either improved or remained stable. “This indicates that the downward trend from the past few months is starting to lose steam across the board,” he added.

However, the cloud over Germany continues to darken. “Germany remains a negative outlier among the big euro countries,” de la Rubia noted. This latest data will likely rekindle debates about Germany being the “sick man of Europe”, even though it remains one of the most diversified economies in the region.

Full Eurozone PMI manufacturing release here.