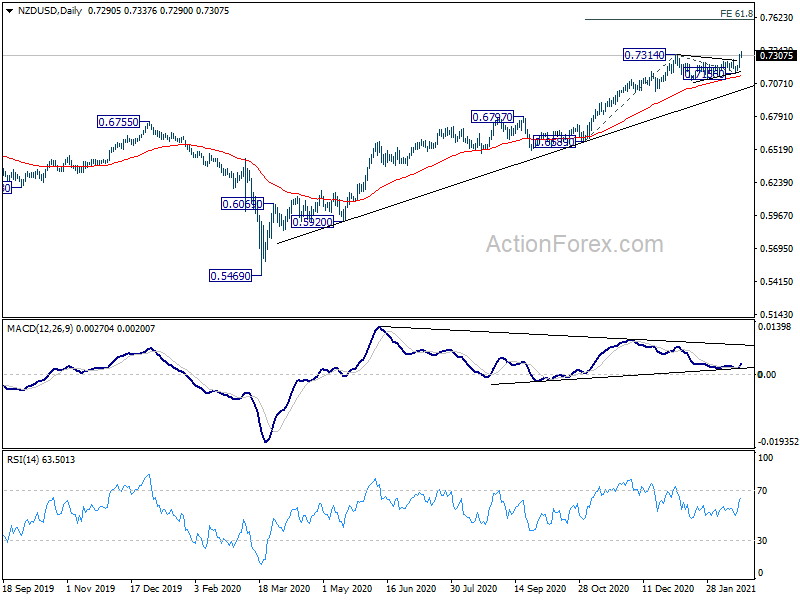

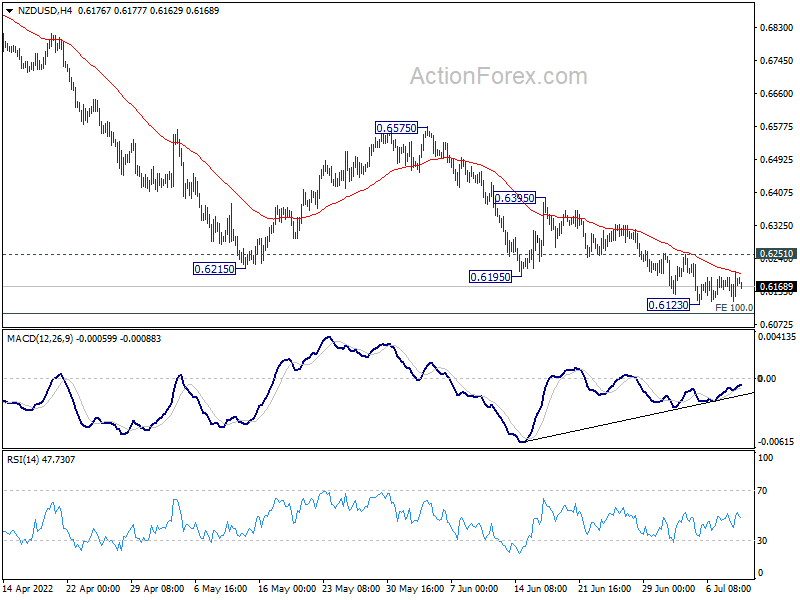

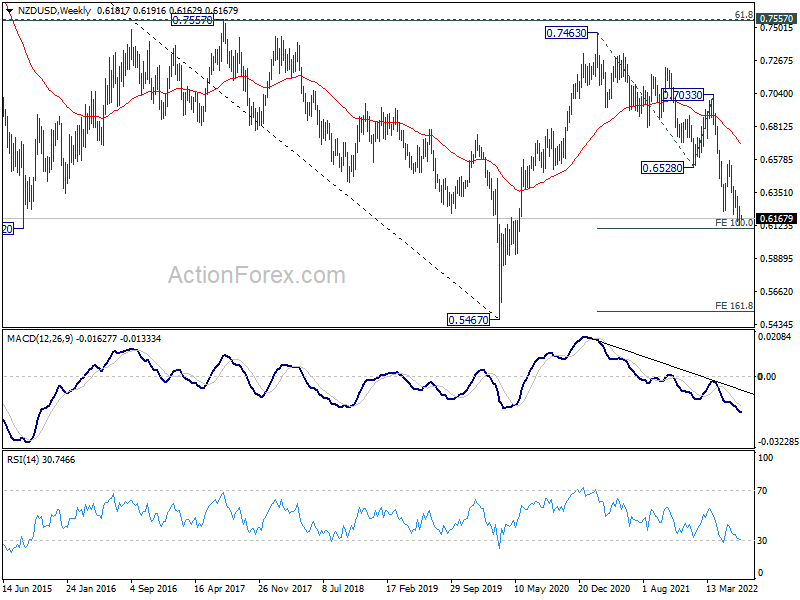

NZD/USD’s up trend resumes by breaking through 0.7314 resistance today and hits as high as 0.7337 so far. From a near term perspective, current rise from 0.5469 should target 61.8% projection of 0.6589 to 0.7314 from 0.7156 at 0.7604 next.

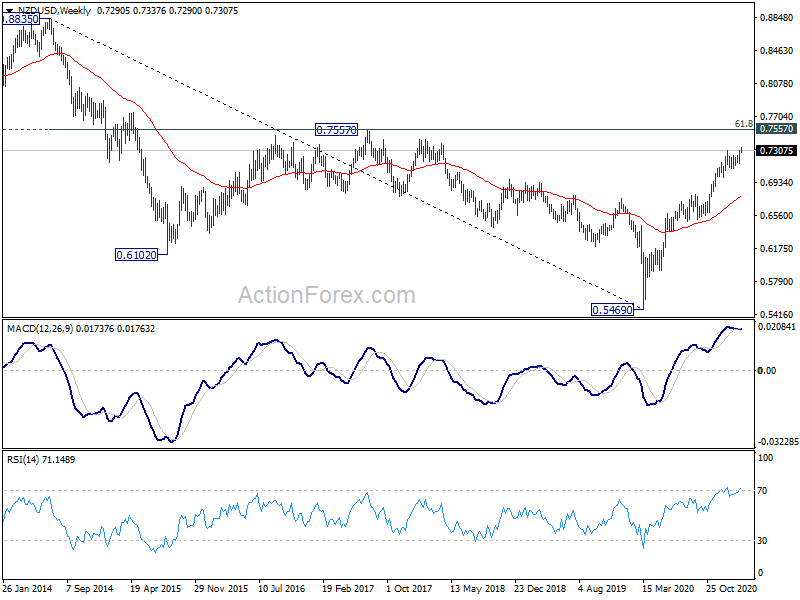

However, a key cluster resistance at 0.7557, 61.8% retracement of 0.8835 (2014 high) to 0.5469 (2020 low) at 0.7549, comes just before above mentioned 0.7604 projection target. Additionally, RBNZ statement poses a slight risk to the Kiwi, in the sense that it may want to talk down the strong exchange rate.

So we’d pay close attention to the momentum of next move. But in any case, outlook will stay bullish as long as 0.7156 support holds, even in case of deep retreat.

Fed George: Inflation expectations can move quickly

Kansas City Fed Esther George said in Helsinki today that inflation expectations “can move quickly”. “It doesn’t look like it will happen in the near term,” but she also emphasized “I never say never… because you don’t know how those expectations might shift.”

Meanwhile, George also noted the median forecast for long-term interest rates has fallen. And, demographic trends have forced a reassessment of the economy.