The financial world was abuzz last week with discussions of oil potentially breaking the 100 mark. While some pundits deem this as a stretch, the consensus is that no one can entirely dismiss the possibility.

The recent spike in oil prices brings with it a myriad of concerns, particularly about its ripple effect on the broader economy. As central banks globally grapple to suppress rising inflation, the surge in energy costs, with gasoline taking the lead, is becoming a pressing issue. Notably, August’s inflation readings surpassed expectations in several countries, with energy prices being the main instigator.

Tracing back to late June, energy prices have witnessed a consistent rise. This surge can be attributed to crude output reductions by major oil producers in OPEC+, coupled with additional cuts from Saudi Arabia. These decisions have propelled crude futures by approximately 30% over the past quarter.

With the possibility of OPEC+ announcing another surprise cut, bullish momentum could very well drive oil prices beyond 100. Contrarily, some anticipate that if prices climb above 95 per barrel, there might be a significant dip in demand, causing oil price to recalibrate and settle within a more balanced range.

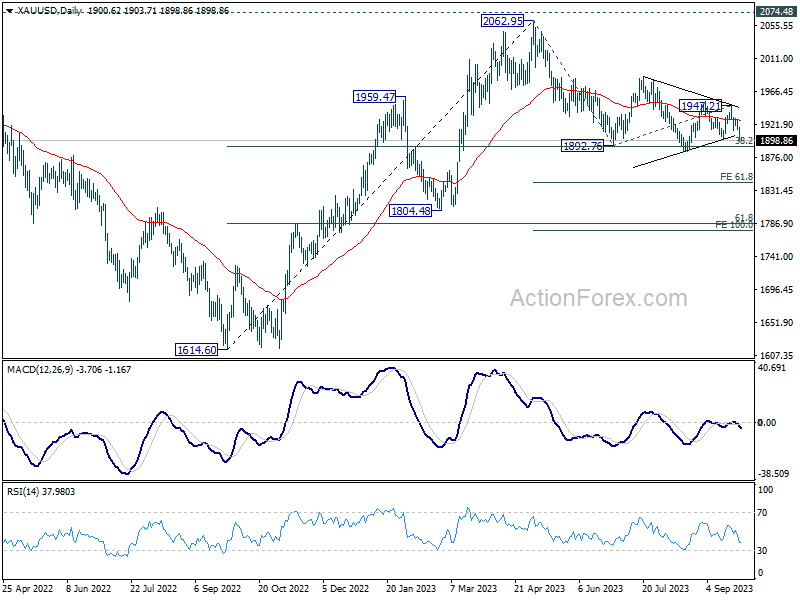

From a technical perspective, WTI crude seems to have hit a near-term ceiling at 93.07 last week. Given that D MACD has already slid beneath the signal line, the prevailing bullish momentum may have been exhausted for the near term.

Nevertheless, decisive drop below 84.91 resistance turned support is essential to counteract the uptrend that began at 66.94. If this doesn’t materialize, the prospects of a continued rally remain. Break of 93.07 will put key resistance level at 50% retracement of 131.82 to 63.67 at 97.74 into focus.

ECB’s Elderson: Policy rates have peaked? Not necessarily

In an MNI interview, ECB Executive Board Member Frank Elderson responded to the speculation on whether interest rates have reached their pea. He noted, “Does that mean policy rates have peaked? Not necessarily. There is still a lot of uncertainty.”

Elderson emphasized the efficacy of the decisions taken by ECB, remarking, “we consider that, with the decisions we’ve made and on the basis of our current assessment, the current interest rate levels will make a substantial contribution to us reaching our inflation target in the medium term.”

Refraining from speculation, he underscored the bank’s methodical approach: “we take these decisions meeting by meeting, on a data-dependent basis. Making any predictions about what we will do next would not be consistent with that approach.”

Highlighting the challenges in the euro area’s economic performance, Elderson revealed, “What we’re seeing is a more protracted period of sluggish growth than we were expecting.” He pointed out several contributing factors to this slowdown, including “lower demand for euro area exports, the impact of tighter financing conditions, lower residential and business investment, and the weakening services sector.”

Yet, not all indicators spell caution. Offering a balanced view, Elderson noted the resilience in certain sectors. “On the other hand, labour markets are still strong and disposable income is expected to rise, which would have a stabilising effect on overall GDP growth.”

Full interview of ECB Elderson here.