Ethereum extends recent down trend today and hit as low as 2927.20, just ahead of 61.8% retracement of 1715.62 to 4863.75 at 2918.20. Further decline is expected as long as 3245.45 resistance holds. Decline from 4863.75 is seen as in the same degree as the rise from 1715.62 to 4865.75. Deeper decline would be seen to or even further to 100% projection of 4863.75 to 3439.00 from 4126.20 at 2701.45, which is close to 2647.30 support, before forming a bottom.

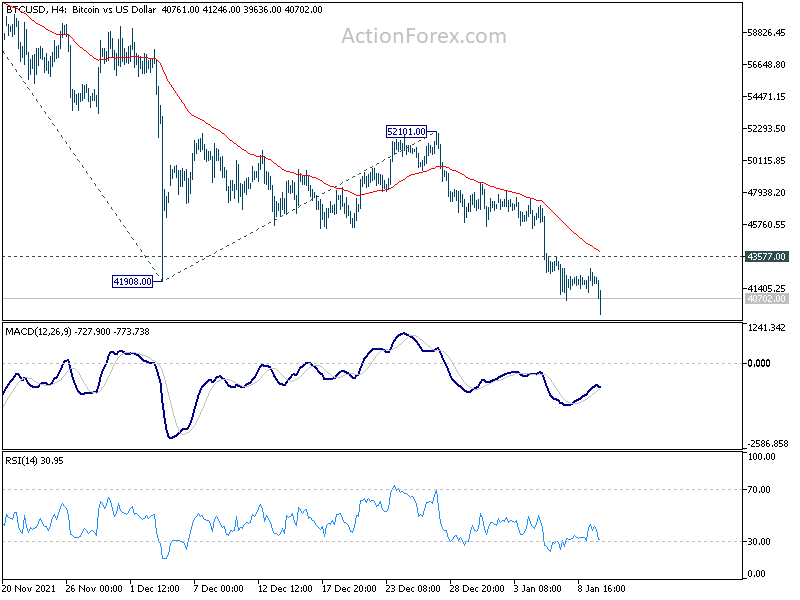

Similarly, Bitcoin is also extending recent fall and hit as low as 39636. Deeper fall is expected as long as 43577 resistance holds. Current fall from 68986 would target 61.8% projection of 68986 to 41908 from 52101 at 35366 before BTC/USD forms a bottom.

European Update: Sterling pares gain as Brexit optimism turns into cautiousness

Sterling reversed some of this week’s gain as Brexit optimism has now turned into cautiousness. UK Prime Minister Theresa May will hold a Cabinet meeting shortly to secure support for her agreement with the EU. And she plan to issue Commons statement after that. EU’s chief negotiator Michel Barnier also plans to make a statement today on the status, and hopefully, he would declare “decisive progress” for a November EU summit. The could be some more volatility in the pound in the upcoming hours.

For now, New Zealand Dollar remains the strongest one for today, followed by Canadian Dollar and then US Dollar. WTI crude oil dipped to as low as 54.84 but it’s now back above 56. The recovery is giving Canadian a breath but that could be temporary. Meanwhile, Swiss Franc is trading as the weakest one, followed by Australian Dollar and then Sterling.

Economic data released today saw US CPI and core CPI stalled at 2.4% yoy and 1.9% yoy respectively. German GDP and Japan GDP contracted in Q3 and both were attributed to global trade tensions. US CPI will be the next focus.

In European markets, major indices are trading mildly softer today. At the time of writing:

Earlier in Asia