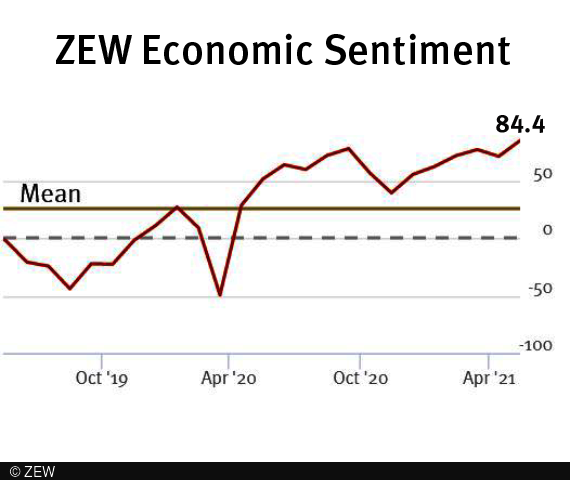

Germany ZEW Economic Sentiment jumped to 84.4 in May, up from 70.7, well above expectation of 71.0. That’s the highest level since in two decades since 2000. Germany Current Situation index improved to -40.1, from -48.8, above expectation of -42.6. Eurozone Economic Sentiment rose to 84.0, up from 66.3, above expectation of 71.2. Eurozone Current Situation rose 14.1 pts to -51.4.

“The slowing down of the third COVID-19 wave has made financial market experts even more optimistic. The ZEW Indicator of Economic Sentiment in the May survey has reached its highest level in more than 20 years. The assessment of the economic situation has also improved noticeably. The experts expect a significant economic upswing in the coming six months. The economic outlook for the euro area and the United States has improved considerably as well,” comments ZEW President Professor Achim Wambach on current expectations.

US oil inventories rose 1.3m barrels, WTI dives following broad based risk selloff

US commercial crude oil inventories rose 1.3m barrels in the week ending May 14, below expectation of 1.5m barrels. At 486m barrels, oil inventories are about 1% below the five year average for this time of year. Gasoline inventories dropped -2.0m barrels. Distillate dropped -2.3m barrels. Propane/propylene rose 0.4m barrels. Commercial petroleum inventories dropped -0.2m barrels.

WTI crude oil drops sharply today, following broad based risk selloff. The current development suggest rejection by 67.83 high as expected. Rise from 57.31, the second leg of the consolidation pattern from 67.83, should have completed at 66.98. Deeper fall would now be seen to 60.62 support first. Break would target 57.31 support and possibly below. Tentatively, we’re looking for support from 38.2% retracement of 33.80 to 67.83 at 54.83 to complete the consolidation pattern.