Bundesbank President Joachim Nagel said in a speech today, “the interest rate step announced (by ECB) for March will not be the last.”

“Further significant interest rate steps might even be necessary afterwards, too,” he added.

Regarding the timing of a rate cut, Nagel said, the impact of tightening has to be reflected in underlying inflation. Until that is the case, interest rate cuts are a non-starter.”

Nagel also said with the current pace of balance sheet reduction at EUR 15B a month, it will take too long to make a significant reduction. “I am therefore in favour of taking a steeper path of reduction starting in July in light of experience gained up to that point,” he said.

Regarding the economy, “although there could be a gradual pick-up in the second quarter, there is still no sign of any major improvement for now,” Nagel said. “Our experts are not expecting there to be a visible economic recovery until the second half of the year.”

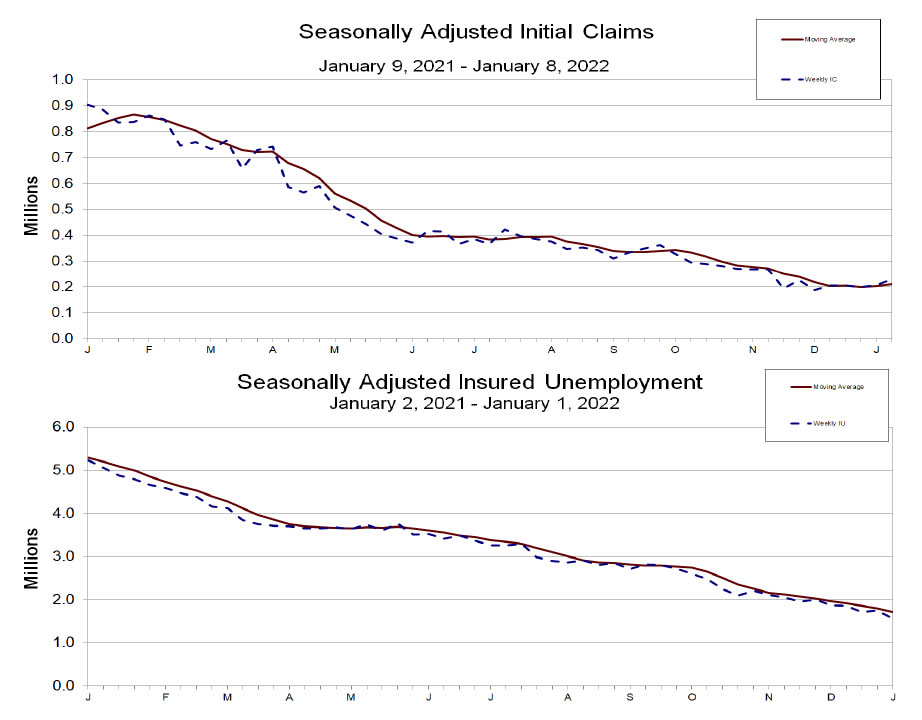

US initial jobless claims dropped to 212k, below expectation of 216k

US initial jobless claims dropped -6k to 212k in the week ending October 19, below expectation of 216k. Four-week moving average of initial claims dropped -0.75k to 215k. Continuing claims dropped -1k to 1.682m in the week ending October 12. Four-week moving average of continuing claims rose 6.5k to 1.677m.

Full release here.