China announced retaliation tariffs on US importants, including soybean, agricultural products, automobiles. These products are valued at around USD 34B, will be subjected to 25% tariffs, starting July 6, 2018.

China would also impose 25% tariffs on other products, valued at around USD 16B, including chemicals, medical equipment, and energy products. Effective date is to be determined.

Below is the “google-translated” statement. Original statement in simplified Chinese could be found here.

Announcement on Imposing Tariff on Certain Products Originating in the United States

On June 15, 2018, the U.S. government announced that it would impose an import tariff of 25% on China’s 50 billion U.S. dollar products, including levied tariffs on about US$34 billion of Chinese exports to the US The measures will be implemented on July 6. Additional tariff measures for the remaining US$16 billion will further seek public opinions. The United States disregards China’s resolute opposition and solemn representations and insists on taking actions that violate the rules of the World Trade Organization. It seriously violates China’s legitimate rights and interests under the rules of the World Trade Organization and threatens China’s economic interests and security.

Regarding the emergency situation caused by the United States’ violation of its international obligations to China, and in order to defend its legitimate rights and interests, China decided to rely on the laws and regulations of the Foreign Trade Law of the People’s Republic of China and other basic principles of international law on soybean, agricultural products , automobiles , and water originating in the United States. Products and other imported goods are subject to tariff levying measures at a tax rate of 25%, involving about 34 billion U.S. dollars in imports from the United States in 2017 (see Annex 1). The above measures will take effect from July 6, 2018.

At the same time, China intends to impose an import tariff of 25% on commodities imported from the United States, including chemicals, medical equipment, and energy products, involving approximately US$16 billion in US imports from the United States in 2017 (see Annex 2), final measures, and effective time. Will be announced separately .

Annex:

List of Customs Tariff Commissions of the State Council Concerning the Collection of Customs Products for the United States and Canada.pdf

The Customs Tariff Commission of the State Council issues a list of tariffs on the United States and Canada.pdf

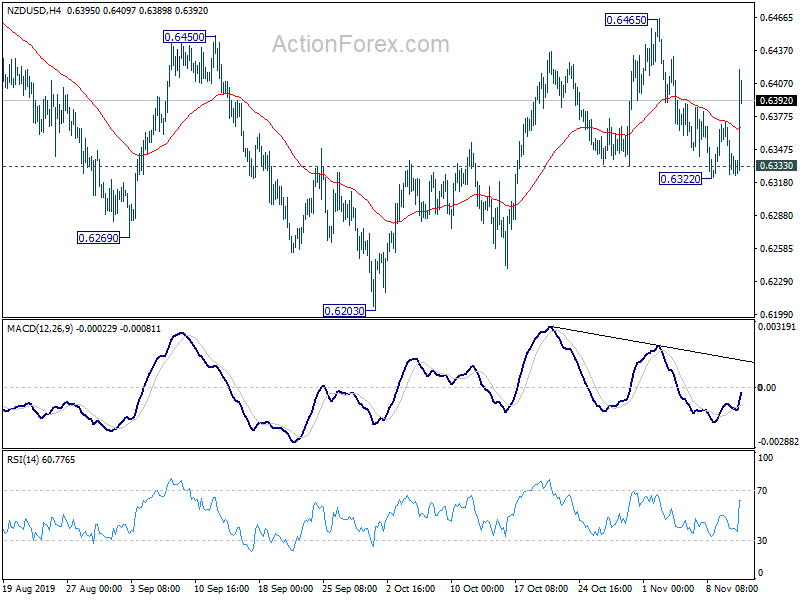

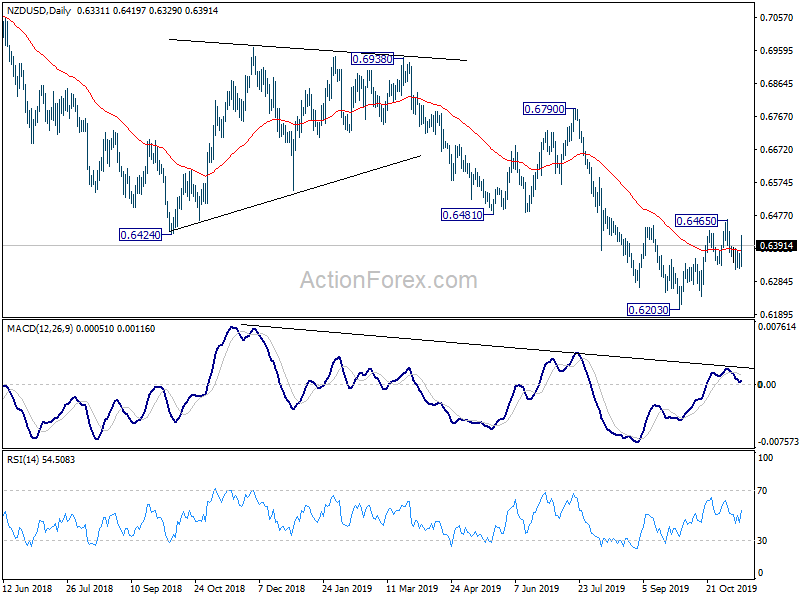

Gold heading back to 1959 high on weak Dollar

Gold prices surged in the Asian session today, following a 2% rally on Friday. At the same time, Dollar and Treasury yield were also trading lower. The market was rocked by the bankruptcy of Silicon Valley Bank, which triggered panic and furthered risk aversion. Moreover, it lowered expectations for interest rate hikes as the failure of the second-largest collapse of an American lender in history has raised concerns of potential spillover effects on the financial system.

Current development argues that Gold’s decline from 1959.47 has completed at 1804.48 already, on bullish convergence condition in 4 hour MACD. The rise back above 55 day EMA is also a bullish signal. Further rally is expected as long as 1858.06 resistance turned support holds. to retest 1959.47 high.

It’s still early to call for an upside breakout. But decisive break of 1959.47 will resume whole up trend from 1614.60 to 61.8% projection of 1614.60 to 1959.47 from 1804.48 at 2017.60.

However, break of 1858.06 will mix up the near term outlook.