ECB President Christine Lagarde said in a speech, the impact of the factors driving up inflation currently “should fade over time”. But for the near term, “inflationary risks are tilted to the upside”. Over the medium-term, ” risks to the inflation outlook could arise if wages rise by more than anticipated, longer-term inflation expectations move above target or supply conditions durably worsen”.

But so far, “wage growth has remained muted – despite a strong labour market – and inflation expectations in the euro area stand around our target”.

On monetary policy, Lagarde said it will “depend on the incoming data and our evolving assessment of the outlook”. ECB would maintain “optionality, gradualism and flexibility” in the conduct of monetary policy.

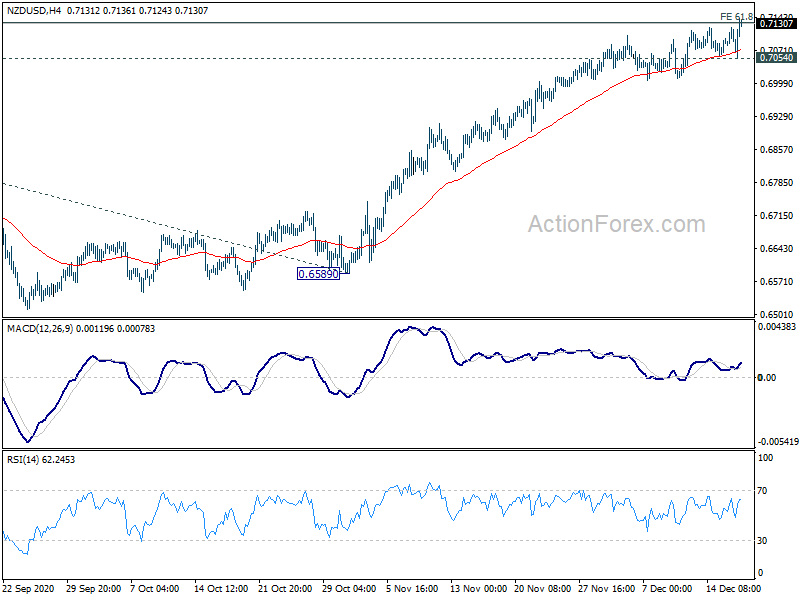

UK CPI slowed to 6.7%, BoE’s hike tomorrow could be the last

Sterling is facing headwinds after release of UK’s CPI inflation data, which came in lower than market forecasts. This development strengthens the speculation that BoE might be drawing curtains on its tightening cycle, with the one more hike expected tomorrow potentially being the concluding move.

The reported data illustrated deceleration in CPI from of 6.8% yoy to 6.7% yoy in August, a result that fell short of the projected escalation to 7.1% yoy. This is the lowest rate witnessed since February 2022.

A deeper dive into the components reveals that this softening of annual CPI into August 2023 emerged from six out of the 12 sectors. Notably, restaurants and hotels, along with food and non-alcoholic beverages, played a pivotal role in pulling down the numbers. However, the motor fuels category within the transport sector exerted upward pressure, somewhat counterbalancing the decline.

Furthermore, core CPI, which is calculated by excluding variables such as energy, food, alcohol, and tobacco, followed suit, decelerating from 6.9% yoy to 6.2% yoy. This stands significantly below anticipated rate of 6.8% yoy.

Breaking it down further, while CPI goods noted a slight acceleration from 6.1% yoy to 6.3% yoy, CPI services delineated a slowdown from 7.4% yoy to 6.8% yoy.

For the month. CPI rose 0.3% mom in August, below expectation of 0.7% mom.

Full UK CPI release here.