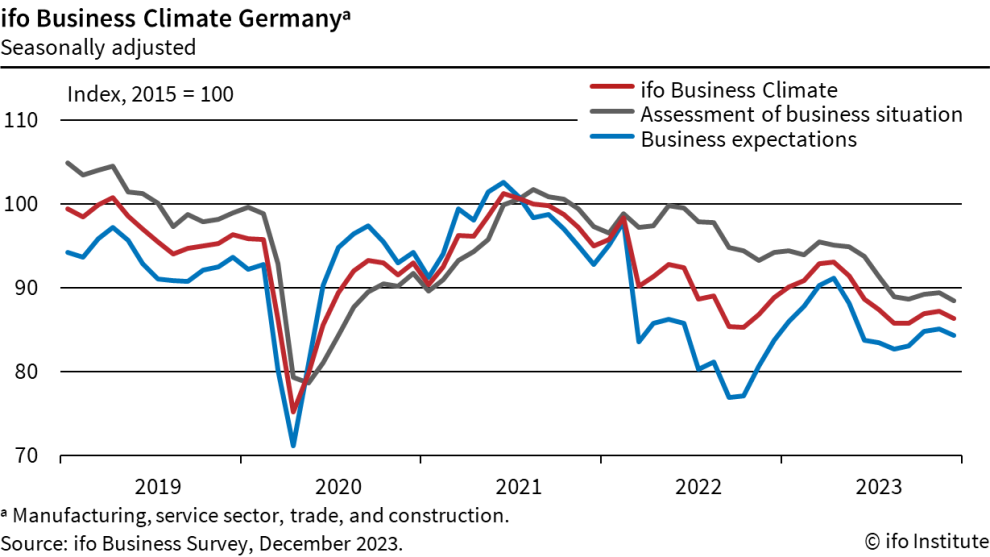

Germany’s Ifo Business Climate fell from 87.3 to 86.4 in December, below expectation of 87.8. Current Assessment index fell from 89.4 to 88.5, below expectation of 89.5. Expectations index fell from 85.2 to 84.3, below expectation of 85.8.

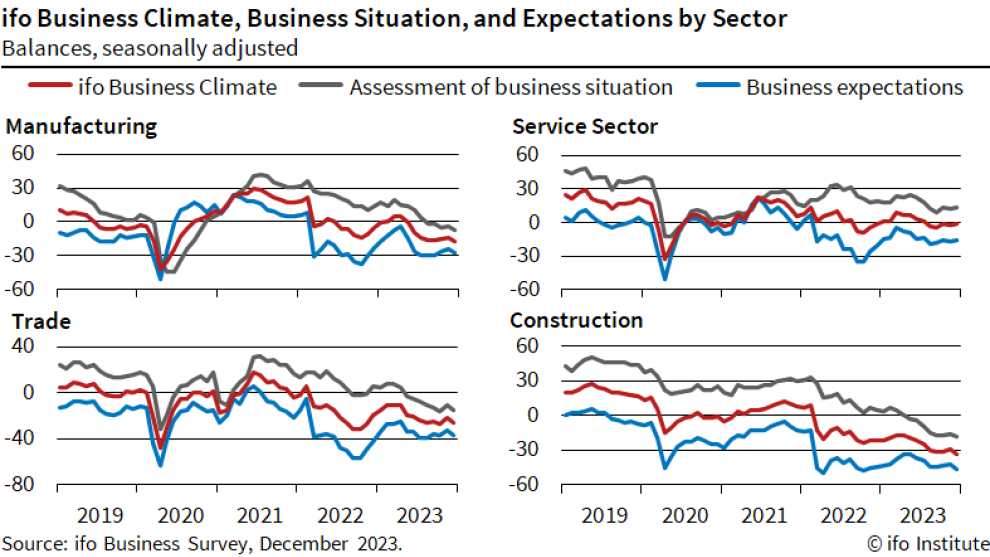

By sector, manufacturing fell from -13.8 to -17.2. Services rose from -2.5 to -1.7. Trade fell from -22.2 to -26.6. Construction fell from -29.5 to -33.1.

The Ifo Institute’s statement encapsulates the current sentiment, noting that “companies were less satisfied with their current business” and expressing a more skeptical view of the first half of 2024. The acknowledgment that “the German economy remains weak as the year draws to a close” is telling of the challenges facing Europe’s largest economy.

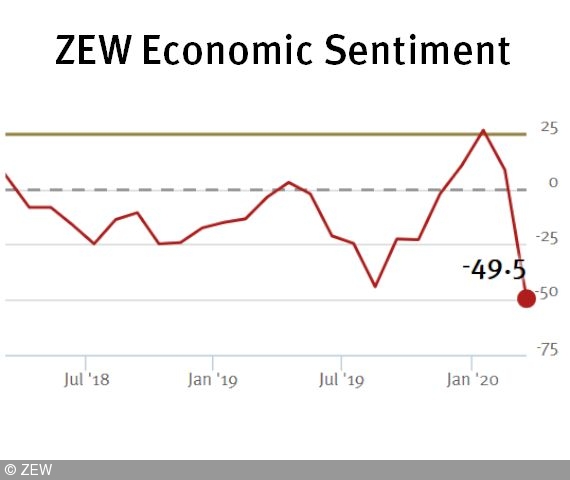

EU laid pre-conditions of lockdown exit, WHO suggests two-week staged approach

European Commission President Ursula von der Leyen urged members stage to take a “gradual approach” in exiting the coronavirus lockdown. And “every action should be continuously monitored”. Also, she laid down three main pre-conditions for the exit: 1. Significant decrease in the spread of the coronavirus 2. Sufficient health system capacity 3. Adequate surveillance and monitoring capacity

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

Load tweet

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

Load tweet

Separately, the WHO said lifting of lockdowns should be down in stages of two weeks. WHO said: “To reduce the risk of new outbreaks, measures should be lifted in a phased, step-wise manner based on an assessment of the epidemiological risks and socioeconomic benefits of lifting restrictions on different workplaces, educational institutions, and social activities… Ideally there would be a minimum of 2 weeks (corresponding to the incubation period of COVID-19) between each phase of the transition, to allow sufficient time to understand the risk of new outbreaks and to respond appropriately.”