In a today address to the European Parliament, ECB President Christine Lagarde noted that economic activity indicators have shown steady improvement in recent months, coinciding with diminished concerns over energy shortages and price hikes. However, she cautioned that accumulated price pressures are still spreading throughout the economy, albeit with some delay.

Lagarde observed, “Wage pressures have strengthened on the back of robust labor markets and employees aiming to recoup some of the purchasing power they have lost to high inflation.” She added that due to inflation remaining “too high for too long,” the ECB Governing Council decided to increase the three key interest rates by 50 basis points last week, demonstrating their commitment to returning inflation to the 2% medium-term target.

In light of the heightened uncertainty, Lagarde emphasized the importance of a “data-dependent” approach to policy rate decisions, stating, “Our policy rate decisions will be determined by our assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission.”

St. Louis Fed President James Bullard told Bloomberg TV that OPEC’s production cut was “a surprise.” But he added, “whether it will have a lasting impact I think is an open question.”

He noted the challenges in tracking oil prices, admitting that fluctuations “might feed into inflation and make our job a little bit more difficult.”

Regarding the current state of the global economy, Bullard pointed out that he had already expected higher oil prices given China’s faster-than-anticipated recovery and Europe narrowly avoiding a recession. He also cited strong US data as a bullish factor for the oil market.

RBA Assistance Governor Christopher Kent delivered a speech on “Financial Conditions and the Australian Dollar – Recent Developments” today. There he acknowledged that developments in Australian financial markets have been similar to those offshore, with falling equity prices, rising credit spreads and increased volatility. Such development is “a story of risk premia increasing from low levels and were associated with rising concerns about downside risks, both internationally and domestically.”

The outlook for domestic economy has “also shifted” with downward revision in both growth and inflation forecasts. And market expectations for the next move in cash rate have “switched signs too”. Kent noted that “markets have assessed that the next move is more likely to be down than up.”. And that’s reflected in lower bond yields.

Fall in Australian bond yields is “likely to have contributed somewhat to the modest depreciation of the Australian Dollar of late”. On the other hand, “higher commodity prices appear to have worked to limit the extent of Australian dollar depreciation”.

Chicago Fed President Charles Evans said, “inflation will stay more elevated in 2022”, but “we have time to be patient”. In his own view, Fed will not need to raise interest rates until 2023.

Nevertheless, in a speech, he said there are signs that inflation pressures could build up more broadly. “These developments deserve careful monitoring and present a greater upside risk to my inflation outlook than I had thought last summer.”

Separately, Fed Governor Michelle Bowman said, “housing supply issues are unlikely to reverse materially in the short term, which suggests that we are likely to see higher inflation from housing for a while.”

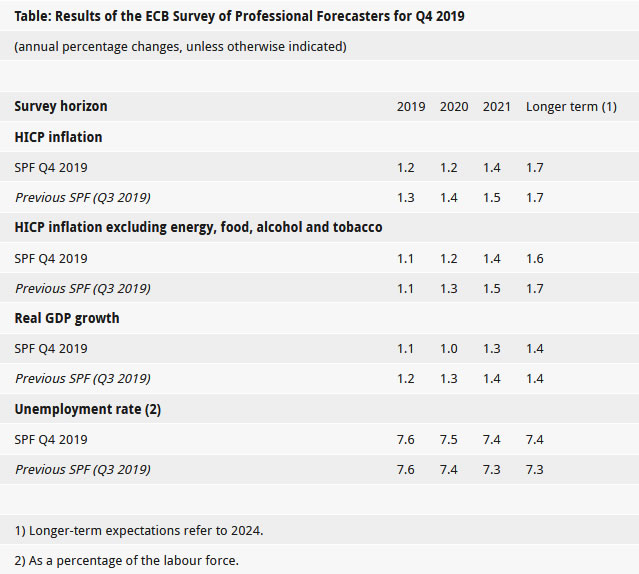

In the Q4 ECB Survey of Professional Forecasters, Eurozone inflation expectations were revised down on average across all horizons. Real GDP growth expectations was also revised down, particularly for 2020. Meanwhile, unemployment rate expectations were also revised up.

HICP inflation is projected to be at 1.2% in 2019 (vs Q3 projection of 1.3%), 1.2% in 2020 (vs 1.4%) and 1.4% in 2021 (vs 1.5%).

Core HICP is projected to be at 1.1% in 2019 (vs 1.1%) 1.2% in 2020 (vs 1.3%), and 1.4% in 2021 (vs 1.5%).

Real GDP growth is projected to be at 1.1% in 2019 (vs 1.2%), 1.0% in 2020 (vs 1.3%) and 1.3% in 2021 (vs 1.4%).

Unemployment rate is projected to be at 7.6% in 2019 (vs 7.6%), 7.5% in 2020 (vs 7.4%) and 7.4% in 2021 (vs 7.3%.

The minutes of RBA’s meeting on March 7 indicate that the central bank is considering a more cautious approach in tightening monetary policy, as uncertainty surrounding the economic outlook persists. The RBA members observed that “further tightening of monetary policy would likely be required to ensure that inflation returns to target.” However, they also noted the restrictive nature of current monetary policy and the economic uncertainty, stating that “it would be appropriate at some point to hold the cash rate steady.”

During the meeting, RBA members agreed to “reconsider the case for a pause at the following meeting, recognizing that pausing would allow additional time to reassess the outlook for the economy.” The decision on when to pause will be determined by incoming data and the board’s assessment of the economic situation.

The RBA acknowledges that “the outlook for consumption remained a key source of uncertainty.” The central bank will closely monitor upcoming data releases on employment, inflation, retail trade, and business surveys, as well as developments in the global economy, to inform their decision-making.

Entering into US session, Australian Dollar is trading as the strongest one for today, as helped by easing risk aversion/return of risk appetite. China Shanghai SSE rose 2.47% to close at 2815.11 and it looks like 2700 key psychological level is now defended well. Nikkei closed up 1.21%, Hong Kong HSI up 1.32% Singapore Strait Times rose 1.16%. European Indices are also solid. At the time of writing, DAX is up 0.2%, CAC up 0.5%, FTSE up 0.4%.

Sterling is trading as the second strongest and markets seemed to be cheering the resignation of Brexit Minister David Davis. Former Minister of State for Housing Dominic Raab is appointed as the new Brexit Minister. Davis’ departure is probably the best for him and PM Theresa May.

Meanwhile, Dollar is trading as the weakest one, followed by the Japanese Yen.

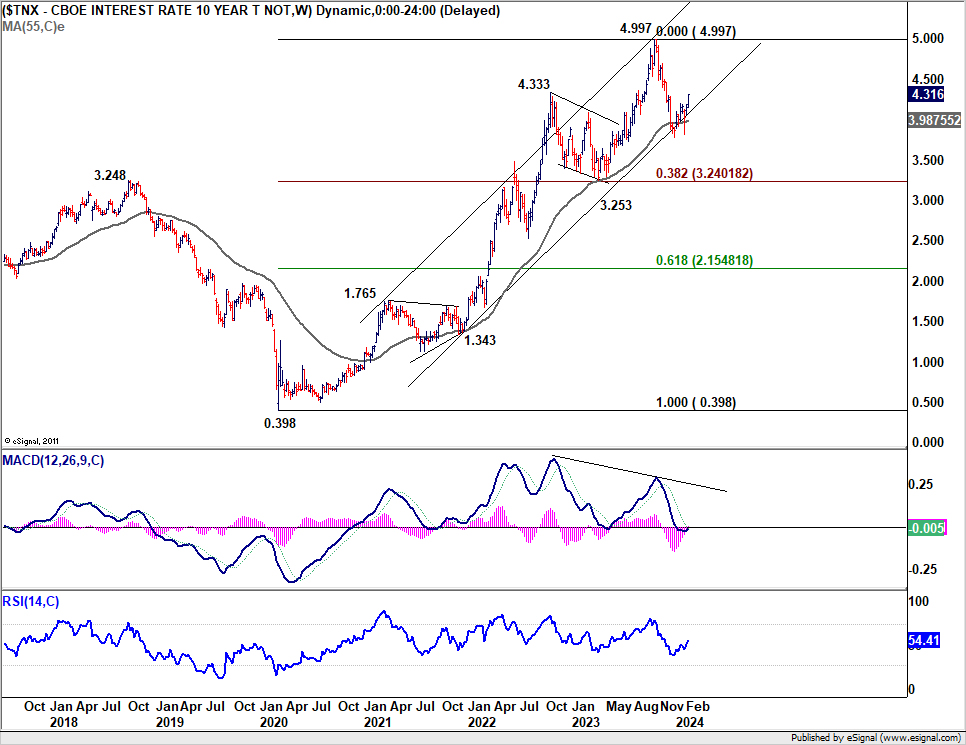

10-year yield rose 0.144 overnight to close at 4.316, breaking above 38.2% retracement of 4.997 to 3.785 at 4.247. A more important perspective is that strong support was seen from 55 W EMA and long term channel, as seen in the weekly chart. Combined, the development suggests that fall from 4.997 has completed at 3.785 already. Further rally is now expected as long as 55 D EMA (now at 4.143 holds), to 61.8% retracement at 4.534 and possibly above.

Nevertheless, there is no change in the view that price actions from 4.997 are developing into a medium term corrective pattern. Rise from 3.785 could be seen as the second leg. Upside should be capped by the 4.997 to bring the third leg down to 3.785 and below.

This technical scenario aligns with the prevailing expectation that Fed’s next move will be a rate cut. The duration and extent of the current rebound in 10-year yield will depend on when Fed decides to initiate policy relaxation. In essence, the more Fed postpones its initial rate reduction, the more prolonged and substantial the climb in 10-year yield could be. Still, this scenario would not push yield beyond 5% handle. However, decisive break of 5% would signal a significant shift in the underlying economic and monetary policy outlook and necessitate reevaluation of these expectations.

Japan national CPI core (all items less fresh food) slowed to 0.7% yoy in February, down from 0.8% yoy and missed expectation of 0.8% yoy. CPU core-core (all items less food and energy) remained sluggish at 0.4% yoy, unchanged from January. Headline all items CPI was unchanged at 0.2%.

Despite BoJ’s massive monetary stimulus, there is no sign for CPI core to achieve the 2% target. And even worse, it’s actually moving farther away from the goal. Sluggish core-core reading is providing no help too. Moreover, there are risks of drag by slowdown in overseas economy. For now, there is practically no case for BoJ to exit ultra-loose policy any time soon.

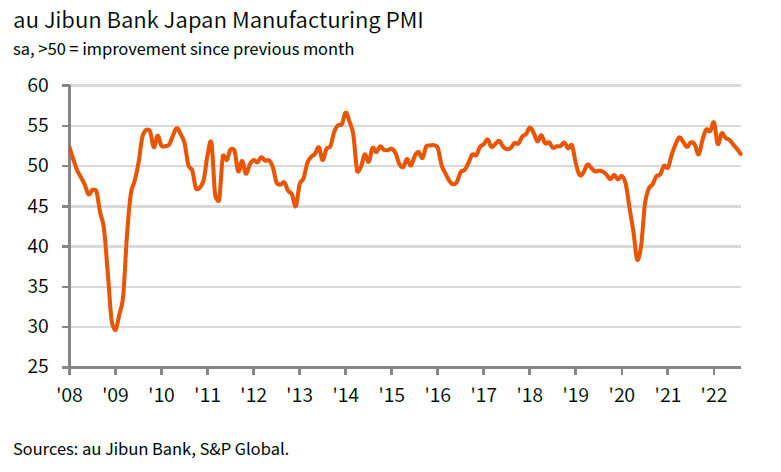

Japan PMI Manufacturing was finalized at 51.1 in August, down from July’s 52.1. The health of the sector that was the joint-weakest since February 2021. S&P Global also noted new orders had the sharpest reduction since October 2020. Backlogs of work decreased for the first time in 18 months. Rise in input prices was slowest for 8 months.

Usamah Bhatti, Economist at S&P Global Market Intelligence, said: “Latest PMI data pointed to deteriorating current activity in the Japanese manufacturing sector midway through the third quarter of 2022…. The dip is likely to continue in the near term… A benefit that has come from softer demand conditions is that pressure on supply chains has been given the opportunity to ease.”

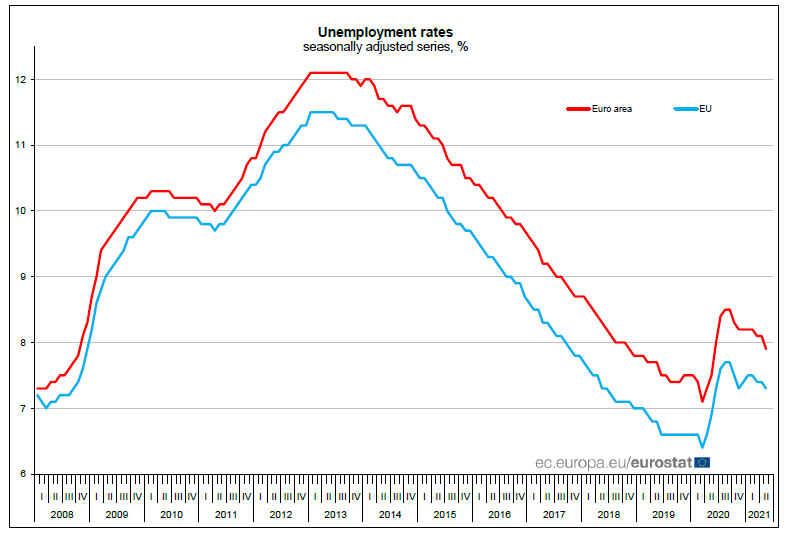

Eurozone unemployment rate dropped to 7.9% in May, down from 8.1%, better than expectation of 8.0%. EU unemployment dropped to 7.3%, down from 7.4%. It’s estimated that 15.278 million men and women in the EU, of whom 12.792 million in the euro area, were unemployed in May.

US ISM Services jumped to 63.7 in March, up from 55.3, above expectation of 58.5. Looking at some details, business activity/production rose 13.9 pts to 69.4. New orders rose 15.3 pts to 67.2. Employment rose 4.5 pts to 57.2. Prices rose 2.2 pts to 74.0.

ISM said: “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for March (63.7 percent) corresponds to a 5.1-percent increase in real gross domestic product (GDP) on an annualized basis.”

Sterling had a wild wide today. It’s firstly lifted by a Bloomberg report that Germany and UK dropped key Brexit demand, paving the way for a deal. But then, the Pound was knocked down after a German government spokesman said that the stance was not changed. After all the volatility, the Pound is trading as the second strongest one for the day so far, next to Kiwi and better than Euro. Euro is clearly supported by sharply narrowed Italian-German yield spread. Italian politician’s promise for not blowing up the public account was well taken by investors.

On the other hand, Dollar is trading as the weakest one for today after yesterday’s rally attempt failed. Canadian Dollar followed as the second weakest. BoC’s standing pat was widely expected. The statement showed much confidence in policymakers and BoC is still on track for an October hike. But the Loonie is troubled by the deadlock in trade negotiation with the US. Yen got little support from risk aversion and is trading as third weakest. Rebound in German yield is a factor contributing to Yen’s sluggishness.

In other markets, US stocks are rather steady. DOW is up 0.04% at the time of writing, S&P 500 down -0.37% and NASDAQ down -1.06%. That’s nothing comparing to -1.0% fall in FTSE, -1.39% in DAX and -1.54% in CAC.

New Zealand employment grew 0.6% in Q1, above expectation of 0.3% qoq. Unemployment rate dropped to 4.7%, down from 4.9%, better than expectation of 4.9%. Labor force participation rate rose 0.1% to 70.4%. Labor cost index rose 0.4% qoq, above expectation of 0.3% qoq.

“There have been some gains in labour market outcomes, especially for women, over the past two quarters. However, annual changes indicate the labour market still hasn’t returned to pre-COVID-19 levels for men or women,” work, wealth, and wellbeing statistics senior manager Sean Broughton said.

Ahead of a broad review on monetary policy framework, Boston Fed President Eric Rosengren said he’d prefer a range targeting approach on inflation. That is, Fed could be forced to accept inflation below 2% during recessions. On the other hand, Fed should commit to achieve above 2% inflation in good times. For example a range of 1.5-2.5%.

Rosengren echoed other platemakers’ comment that the current 2% target is “symmetric”. But in practice, people saw that figure as a “ceiling”. He added, “even though we’re only missing by a little bit it actually does matter if you miss by a little bit on a regular basis.”

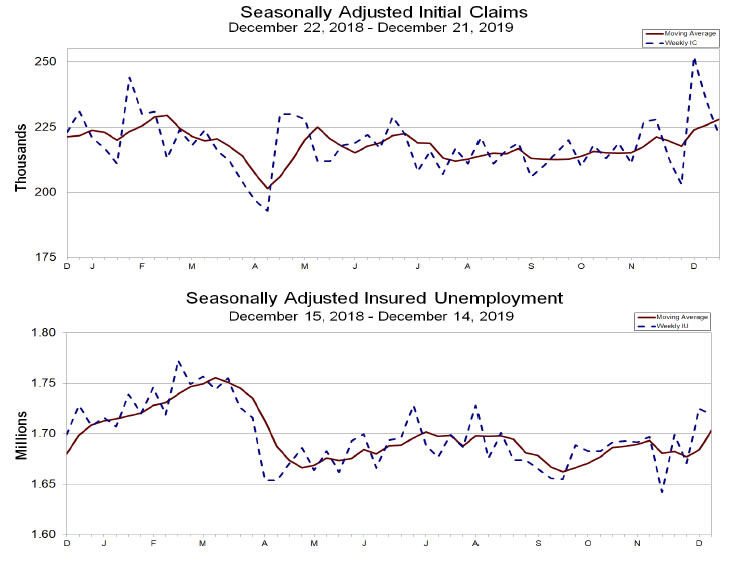

US initial jobless claims dropped -13k to 222k in the week ending December 21, matched expectations. Four-week moving average of initial claims rose 2.25k to 228k.

Continuing claims dropped -6k to 1.719m in the week ending December 14. Four-week moving average of continuing claims rose 19.25k to 1.704m.

Dollar dives sharply as Fed Chair Jerome Powell seems to be backing down from his monetary stance, facing political pressure from Trump.

The key take away is that Powell said “. Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy‑‑that is, neither speeding up nor slowing down growth.”

That is, in Powell’s view, federal funds rate at 2.00-2.25% is “just below” neutral.

However, it should be noted that in September projections, median longer run projected federal funds rate was 3.0%. Central tendency was at 2.8-3.0%. And the range was from 2.5-3.5%.

2.00-2.25% couldn’t be considered being “just below” 3.0%, nor 2.8-3.0%. So, is Powell finally revealing himself as a dove, not that balanced, composed Fed chair that he protraited? Or is he selling Fed’s independence?

Also, back on October 3, Powell said “We may go past neutral, but we’re a long way from neutral at this point, probably” (see this CNBC report). Powell in his own words on October 3. Just in case, start at 8:00.

By loading the video, you agree to YouTube’s privacy policy. Learn more

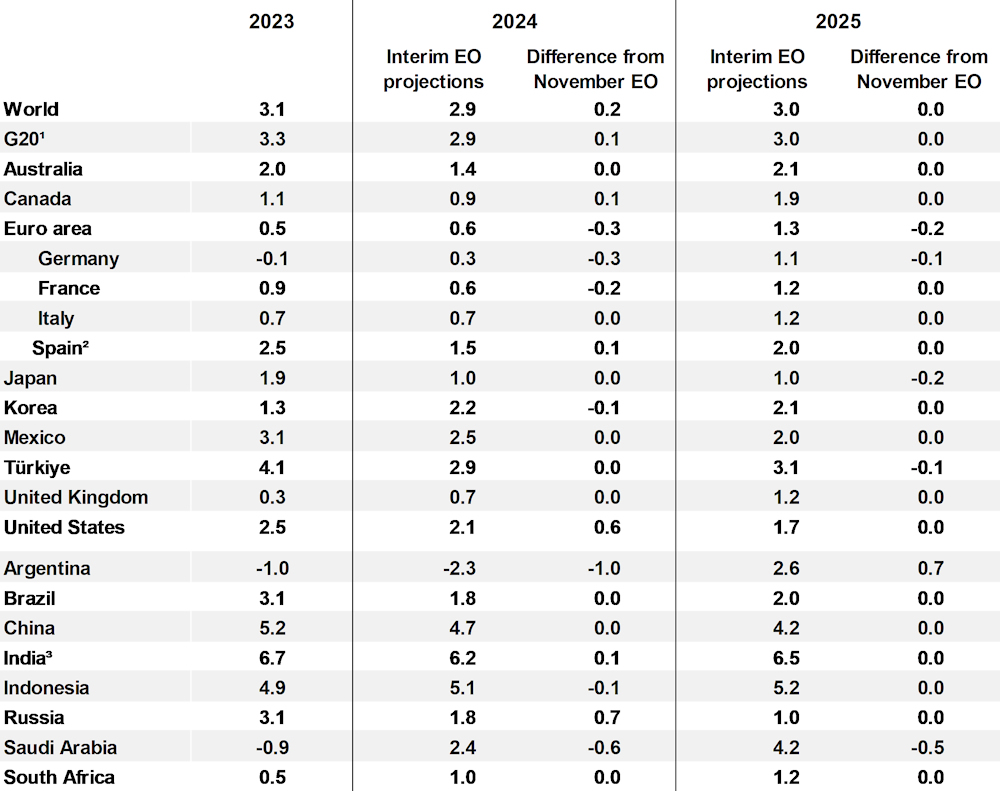

OECD’s latest Interim Economic Outlook report presents a cautiously optimistic upgrade in global growth forecasts for 2024 to 2.9% (up from November’s 2.7% forecast), a notable uplift largely attributed to stronger performance of US economy.

“Some moderation of growth” from 2023 is expected, under the influence of tighter financial conditions affecting credit and housing markets, alongside a subdued global trade dynamics. Recent attacks on ships in the Red Sea have introduced further volatility and exert upward pressure on prices.

Despite some moderation in growth and the ongoing adjustments to tighter financial conditions, OECD cautions that it is “too soon to be sure that underlying price pressures are fully contained.” Labor markets showing signs of equilibrium bring a positive note, yet the persistently high unit labor cost growth looms as a challenge for meeting medium-term inflation targets.

The specter of high geopolitical tension, particularly in the Middle East, poses a “significant near-term risk to activity and inflation”, with potential disruptions in energy markets likely to have far-reaching consequences. Furthermore, persistent service price pressures could lead to inflation surprises, necessitating reevaluation of monetary policy easing expectations. On the other hand, growth could be weaker if effects of past monetary tightening are stronger than expected.

Here are some details.

Global growth forecast for 2024 raised up by 0.2% to 2.9%. 2025 unchanged at 3.0%.

US growth forecast for 2024 raised by 0.6% to 2.1%. 2025 unchanged at 1.7%.

Eurozone growth forecast for 2024 lowered by -0.3% to 0.6%, 2025 down by -0.2% to 1.3%.

Japan’s growth forecast for 2024 unchanged at 1.0%. 2025 lowed by -0.2% to 1.0%.

China’s growth forecast for 2024 unchanged at 4.7%. 2025 unchanged at 4.2%.

Eurozone Sentix Economic Index dropped to -5.8 in June, down from -3.3 and missed expectation of 0.2. It’s also the lowest level since November 2014. Current Situation Index dropped from 6.0 to 1.8, lowest since February 2015. Expectations Index also dropped from -12.3 to -13.0, lowest since February 2019.

Sentix noted that after the supposed de-escalation signals in US-China trade war at G20, there was “great hope that the downward trend in the economy could be stopped”. But, investors are “not blinded by the rising share prices” as expectations show no upward reaction to the news. It warned, “without resilient negotiation results, it will be difficult for investors worldwide to develop a different perspective.”

For Germany, Overall Economic Index dropped from -0.7 to -4.8, lowest since November 2009. Current Situation Index dropped from 13.5 to 7.0, lowest since April 2010. Expectations Index dropped from -14.0 to -16.0, lowest since February 2019.

Sentix said “things are even worse for the German economy”. “The high dependence on exports and the Chinese sales market is increasingly becoming a burden and the customs dispute hovers like a sword of Damocles over the former model boy of the Euro region.” Also, the automotive industry is “simply not emerging from the crisis”.

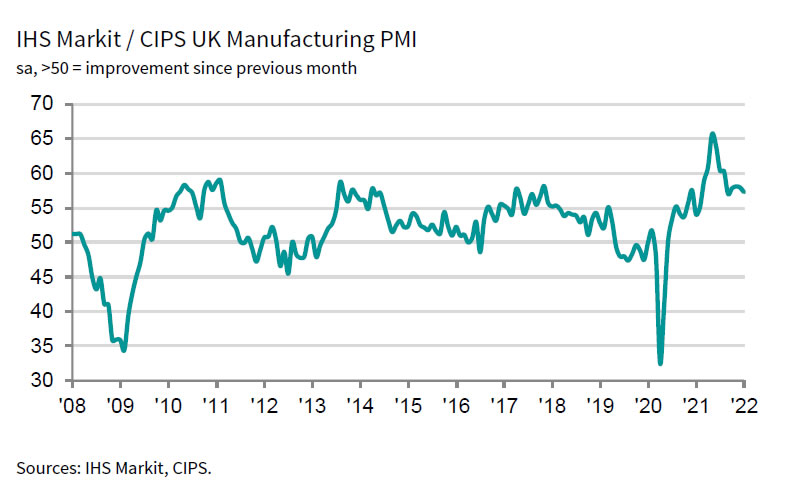

UK PMI Manufacturing was finalized at 57.3 in January, slightly down from December’s 57.9. Markit said production rose at fastest rate in six months. new order growth slowed despite mild uptick in new export businesses. Input cost and output price inflation eased.

Rob Dobson, Director at IHS Markit, said: “UK manufacturing made a solid start to 2022, showing encouraging resilience on the face of the Omicron wave, with growth of output accelerating as companies reported fewer supply delays. Causes for concern remain, however, as new orders growth slowed, exports barely rose, staff absenteeism remained high and manufacturers’ ongoing caution regarding supply chain disruptions led to the beefing up of safety stocks

“There was some positive news on the supply chains front. Although pressure on vendors remains severe, and still sufficient to stymie output growth and cause difficulty in obtaining required inputs, supplier lead times lengthened to the lowest degree since November 2020 to suggest that the current period of abnormal stress has hopefully passed its peak, despite the surge in cases linked to Omicron. This also lessened the upward pressure on prices, with input costs and output charges both rising at less elevated rates in January.”

ECB Lagarde: Price-pressures still spreading through the economy

In a today address to the European Parliament, ECB President Christine Lagarde noted that economic activity indicators have shown steady improvement in recent months, coinciding with diminished concerns over energy shortages and price hikes. However, she cautioned that accumulated price pressures are still spreading throughout the economy, albeit with some delay.

Lagarde observed, “Wage pressures have strengthened on the back of robust labor markets and employees aiming to recoup some of the purchasing power they have lost to high inflation.” She added that due to inflation remaining “too high for too long,” the ECB Governing Council decided to increase the three key interest rates by 50 basis points last week, demonstrating their commitment to returning inflation to the 2% medium-term target.

In light of the heightened uncertainty, Lagarde emphasized the importance of a “data-dependent” approach to policy rate decisions, stating, “Our policy rate decisions will be determined by our assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission.”

Full speech of ECB Lagarde here.