Regarding the US steel tariffs, EU Trade Commissioner Cecilia Malmström will speak with US Commerce Wilbur Ross today. Malmström will try to get last minute consent from the US to exempt the tariffs on EU, which temporary exemption expires tomorrow. However, it’s reported that EU officials are concerned with impossible demands from the US.

European Commission spokes Margaritis Schinas said in a news conference calmly that “we are patient but we are also prepared.” EU’s stance was made clear after German Chancellor spoke with French President Emmanuel Macron and UK Prime Minister Theresa May on Sunday. Merkel said Europe was “resolved to defend its interests within the multilateral trade framework”.

On April 16, EU has already submitted a request to WTO to determine how the US can compensate if trade flows into the EU are affected by the new tariffs. That’s request was under TWO’s Safeguard Agreements. EU also plans to join another separate WTO complaint against the US, arguing that the steel tariffs violate the most-favored nation principle, which forbid discrimination between their trading partners. In addition, it’s reported that EU could retaliate by imposing levies on EUR 2.8b of American goods. And that could start as soon as on June 21, 90 days after the US steel tariffs took effect.

US personal income rose 0.4% mom, spending rose 0.4% mom, core PCE accelerated to 1.9% yoy

US personal income rose 0.4% mom in March, below expectation of 0.4%. Personal spending rose 0.4%, in-line with consensus. Headline PCE accelerated to 2.0% yoy in March, up from 1.7% yoy in February, matched expectations. Core PCE accelerated to 1.9% yoy, up from 1.6% yoy, also met expectations.

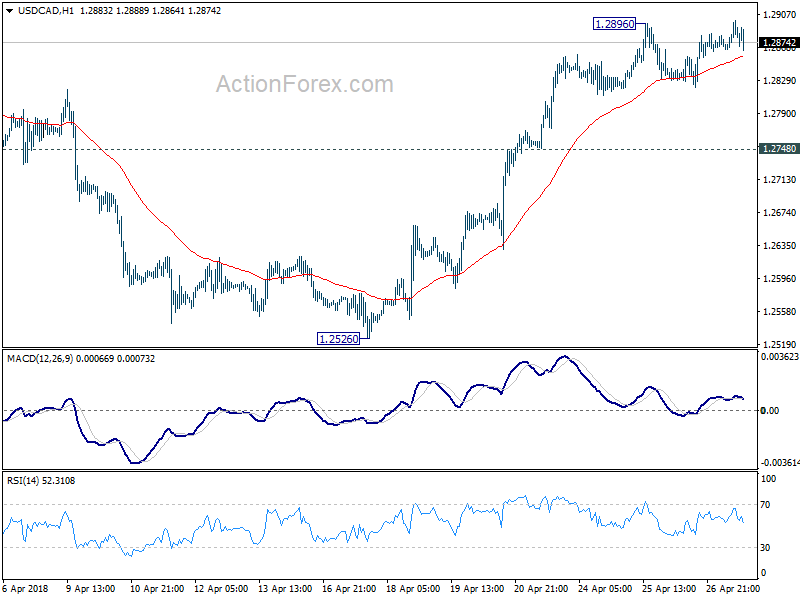

From Canada, IPPI rose 0.8% mom in March, above expectation of 0.2% mom. RMPI rose 2.1% mom, above expectation of 0.6%.

Also German CPI was unchanged at 1.6% yoy in April, above expectation of slowing to 1.5% yoy.

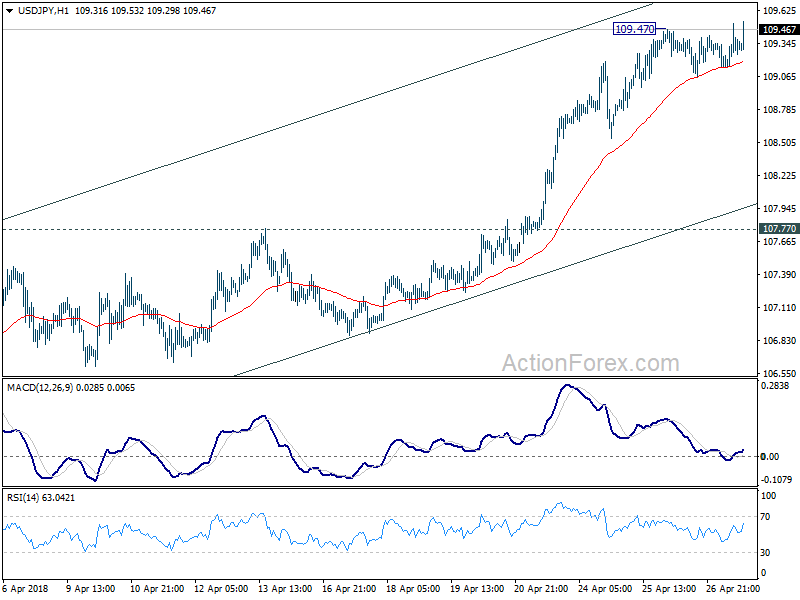

Dollar is steady after the release. Firm, but limited below Friday’s low except versus Sterling.