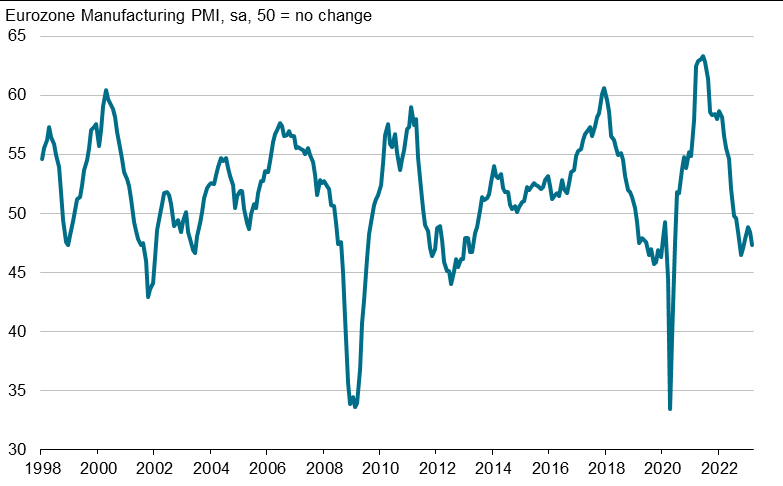

Eurozone PMI Manufacturing was finalized at 47.3 in March, down from February’s 48.5, a 4-month low. Looking at some member states, Greece (52.8, 10-month high) and Spain (51.3, 9-month high) improved. Others deteriorated including Italy (51.1, 2-month low), Ireland (49.7, 3-month low), France (47.3, 5-month low), the Netherlands (46.4, 4-month low), Germany (44.7, 34-month low), and Austria (44.7, 34-month low).

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, highlighted that Eurozone manufacturing “remains in troubled waters” as factories report an eleventh consecutive month of falling demand due to factors such as surging living costs, tighter monetary policy, inventory destocking, and low customer confidence.

He also pointed out that the lack of demand has shifted pricing power from sellers to buyers, and lower energy prices have helped reduce costs. As a result, “prices paid for inputs by factories are now falling sharply on average,” and slower increases in selling prices should eventually lead to lower consumer prices for goods.

US CPI and Fed awaited, NASDAQ surges to new record

Global financial markets are on high alert today as they await two critical announcements from the US, including the release of May’s CPI and FOMC rate decision accompanied by new economic projections. These events are expected to play a crucial role in shaping market sentiment and monetary policy outlooks.

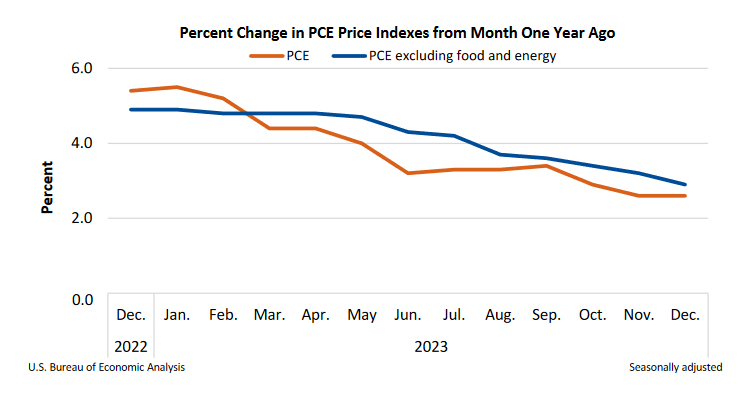

Analysts expect headline CPI to remain steady at 3.4% yoy, while core CPI, which strips out volatile food and energy prices, is anticipated to dip further from 3.6% yoy to 3.5% yoy. On a month-over-month basis, headline CPI is projected to rise by 0.2% mom, and core CPI by 0.3% mom.

Regarding Fed’s upcoming decision, the consensus is that interest rates will be held steady at 5.25-5.50%. However, the focus will be on the updated dot plot, which reflects the rate expectations of Fed policymakers. Key questions include how many policymakers now foresee fewer than two rate cuts this year and whether any still see the need for further hikes.

Current market sentiment suggests that Fed might only cut rates once this year, with an 88.5% probability of a cut by December. The chances of a rate cut in September stand at 52.6%, while the likelihood of a cut in November is slightly higher at 67.1%. These expectations will be closely scrutinized against the backdrop of today’s announcements.

Ahead of theses key events, NASDAQ is looking unstoppable as it surged to fresch all-time highs. S&P 500 also closed at record but its gain was dwarfed by the tech index, while DOW lagged further behind with a loss.

Technically, further rise is expected in NASDAQ as long as 17343.54 support holds. Next target is 61.8% projection of 12543.85 to 16538.86 from 1522.77 at 17691.68. Firm break there could prompt upside acceleration to 100% projection at 19217.78. On the downside, break of 17343.54 will bring consolidations first before staging another rally.