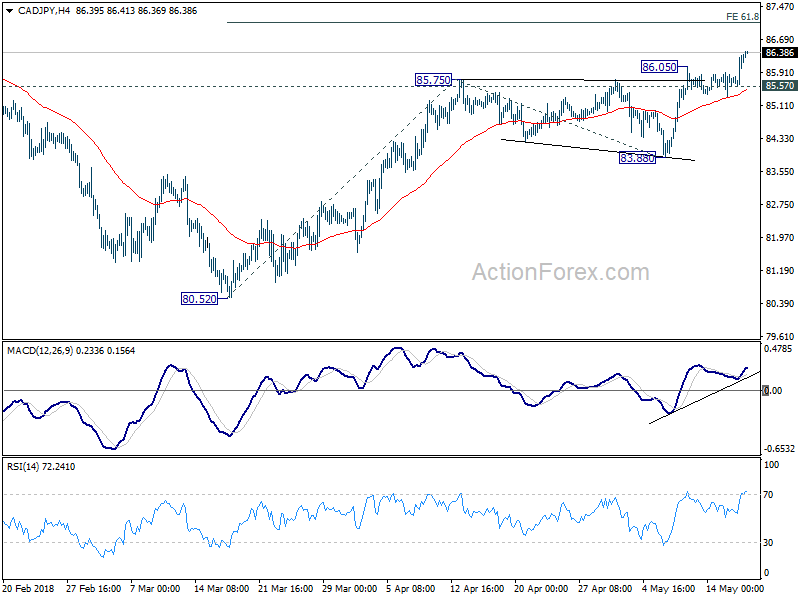

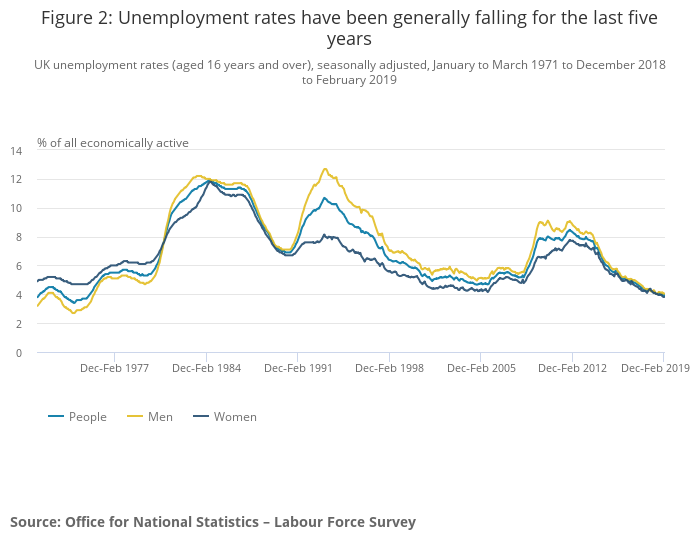

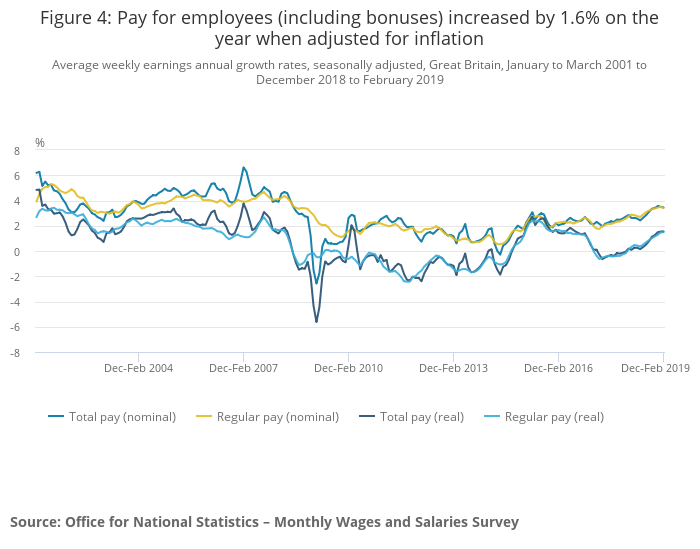

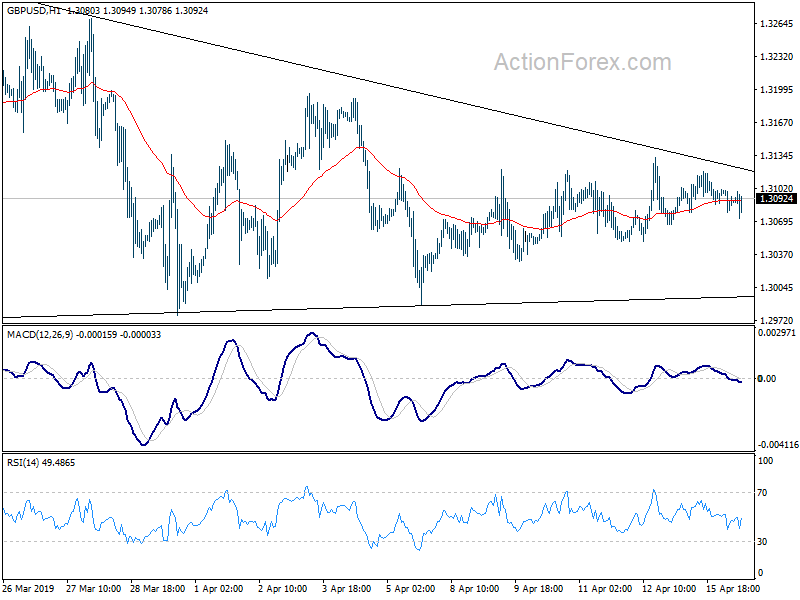

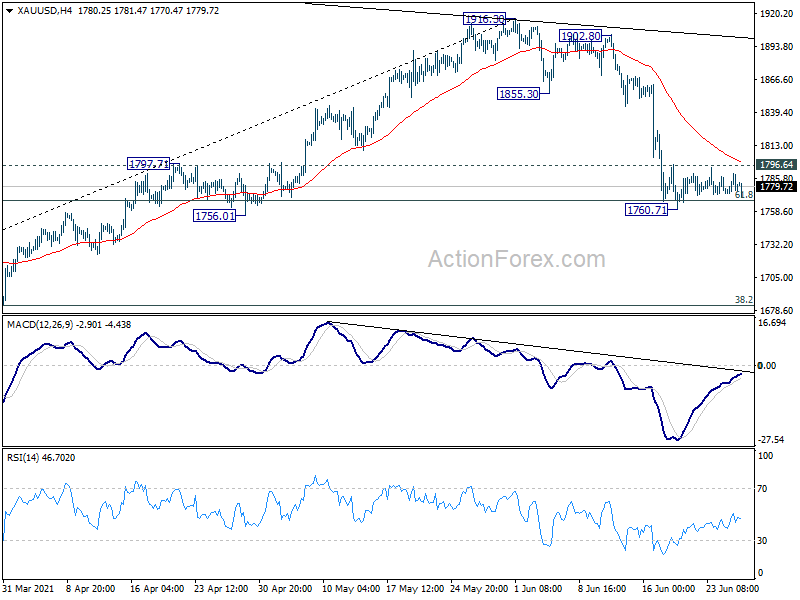

While GBP is the star performer today, the weekly top movers table shows CAD is the real strong one. CADJPY’s break of 86.05 resistance last week confirmed up trend resumption. That’s consistent with our view here on Monday that CAD/JPY was a better choice for trend trading than EUR/JPY.

The framework of using just the top movers table, heat map and action bias could be used to identify, or rule out, trend trading candidates. For counter trend trading, the results of the frame work are less accurate, just as our views on GBPCHF and NZDUSD reversals were wrong. But reversals are harder to call anyway.

CADJPY Action Bias table and D Action Bias chart are both consistent with the view that rise from 80.52 is extending, and with solid momentum.

Back to the regular bar chart, CADJPY is now reading to target 61.8% projection of 80.52 to 85.75 from 83.88 at 87.11. Near term bullishness will remain as long as 85.57 support holds, in case of retreat.

Yen mildly higher as Trump-Kim summit cut short, no agreement reached

Yen is given a mild lift on news that Trump-Kim summit in Vietnam is cut short, for unknown reason. Trump will pull ahead his scheduled media conference to 0700 GMT. And, for now, it’s unknown whether the scheduled “join agreement signing ceremony” would still be held.

White House spokeswoman Sarah Sanders confirmed that “the two leaders discussed various ways to advance denuclearization and economic driven concepts,” but “no agreement was reached at this time, but their respective teams look forward to meeting in the future.”

Earlier, both sides indicated progresses in denuclearization of the Korean Peninsula. Kim told reports that “If I’m not willing to do that, I won’t be here right now”. Trump responded by saying “that might be the best answer you’ve ever heard.”