Trump finally announce his plan to tariff as much as USD 60b in Chinese imports to safeguard technological development of the US and its future.

Sorry, can you elaborate on what do you mean?

Well, Trump said, “this has been long in the making,” and “we have a tremendous intellectual property theft situation going on” with China affecting hundreds of billions of dollars in trade each year”.

Sorry, but… are you talking about USD 60b tariffs annually?

No. And apparently no. The tariff is only on USD 60b of Chines imports!

So how much is the tariff?

We here don’t know yet. What we only know is that Trump complained that “We’ve lost, over a fairly short period of time 60,000 factories.” And, he complained that China has been steal our jobs, stealing our technology. Yet, Trump said today that he view these thieves “as a friend”?!!

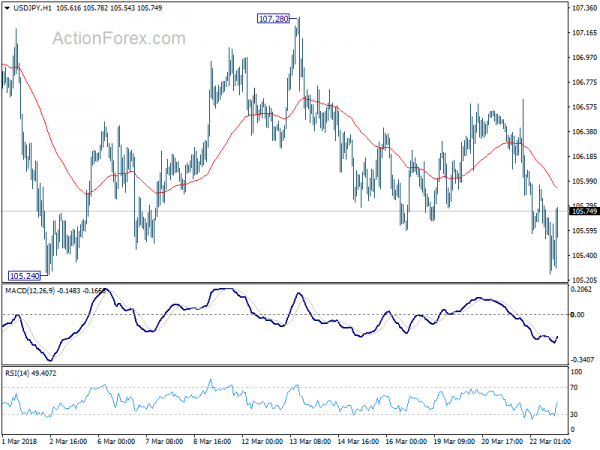

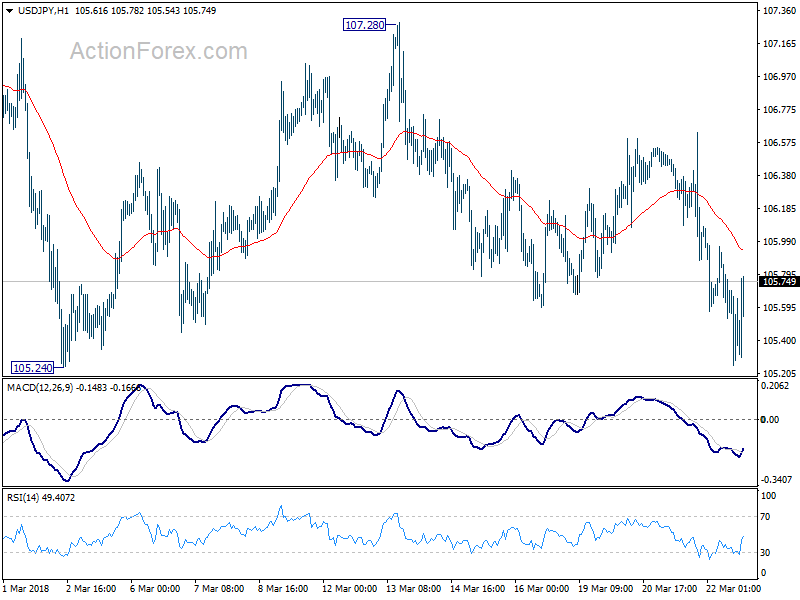

Anyway, reactions from the financial market is clear. USD/JPY recovers ahead of 105.24 near term support, without breaking.

DOW also recovers after after dipping to as low as 24175.49.

The markets’ message is clear. Don’t bother me until you’re doing something significant!

BoC stands pat, expects Q3 to recover 40% of H1 economic collapse

BoC kept monetary policy unchanged as widely expected. Overnight Rate is held at the effective lower bound of 0.25%. Bank Rate is kept at 0.25% correspondingly, deposit rate at 0.25%. BoC will also continue the QE program with large-scale asset purchases of at least CAD 5B per week of government bonds. BoC also pledge to “provide further monetary stimulus as needed.”

In the accompanying statement, BoC said global and Canadian outlook is “extremely uncertain, given the unpredictability of the course of the COVID-19 pandemic”. It expects global economy to contract by -5% in 2020, then grow by 5% on average in 2021 and 2022. But the timing and pace of recovery varies among regions.

Canadian economic activity in Q2 is estimated to be 15% lower than the level at the end of 2019. But there are “early signs” that reopening and pent-up demand are leading to an “initial bounce-back” in employment and out put. In BoC’s central scenario, roughly 40% of H1’s contraction is made up in Q3. Real GDP would still decline -7.8% in 2020, with 5.1% growth in 2021 and 3.7% in 2022.