RBNZ rate decision is a major focus in the upcoming Asian session. It’s widely expected to keep OCR unchanged at 1.75%. There is little to practically no chance of a surprise. The question is on how RBNZ view the sharp slow down in CPI to 1.1% in Q1. The reaction of NZD would very much depend on how dovish the new governor Adrian Orr is.

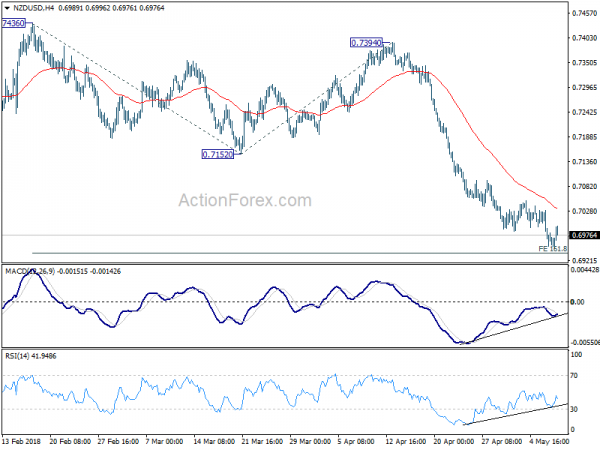

Take a look at NZDUSD Action Bias table, D row shows it’s clearly in a down trend. However, 6H Action bias suggests that downside momentum is unconvincing. Adding to that, there is a few bard of upside blue H row, arguing that it’s in a rebound.

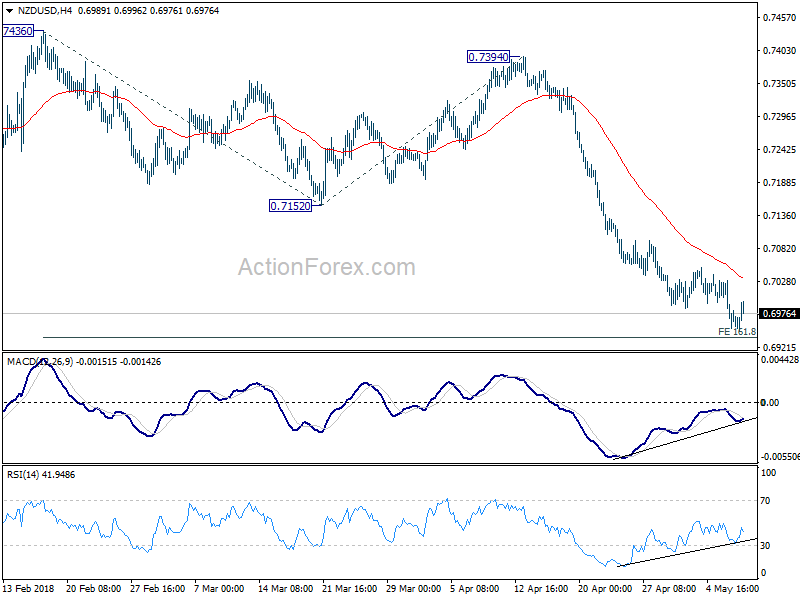

Take a look at the 6H Action Bias chart, it’s apparent, even with eyeballing, that the decline since mid April is losing momentum. The so many neutral bars since late April is consistent with this view. So, is it ready for a rebound?

Take a look at the regular bar chart, we see that NZD/USD reached as low as 0.6947 earlier today. It’s now close to 161.8% projection of 0.7436 to 0.7152 from 0.7394 at 0.6934. Bullish convergence is seen in 4 hour RSI. There is possibility of bullish convergence in 4 hour MACD too. So, this is a good candidate for counter trend, or reversal trading.

We’d like to emphasize that the exact strategy is very personal. It has to suit one’s temperament. Some traders like to catch tops and bottoms. Some traders like to grab quick profits on swing trades. Some like scalping. Some like to hold a position for a few weeks or more. While the strategies vary, the analytic process, to us, is pretty much the same. It’s about deciding what to trade first, then see if it fits our style. To us, it has to be the “style” first, then “what”, before “how” the actual system.

That is, for those who like counter trend trading (style), NZDUSD (what) is a candidate. And how? We’ll buy on next dip, with a tight stop below 0.6934 projection level at 0.6900, target 0.7152 support turned resistance, and get out earlier if momentum of the rebound is weak. Other traders could have their own way based on their temperament.

Fed Daly: One month does not a victory make

San Francisco Fed President Mary Daly said yesterday that the slowdown in inflation was “goods news”. Yet, “one month does not a victory make.”

“We have to be resolute to bring inflation down; we’re united in that commitment,” she said. “It’s raising the rate and then holding it for a length of time that is sufficient to bring inflation reliably back to 2%.”

“I would rather move a little bit higher and have to come back then to move a little bit less high and to then tell people we’re going to go higher, because at some point it does seep into inflation expectations,” Daly said.

At the same time, she said, “I don’t want to be over tightening to the point where we throw the economy into a sharp recession, but if we are talking about a rate hike on either side, I want to fully get inflation sustainably down to 2% on average.”