US equities were strong over night while treasury yield also jumped. DOW rose 346.41 pts or 1.40% to 25146.39. S&P 500 rose 023.55 pts or 0.86% to 2772.35. NASDAQ gained 51.38 pts or 0.67% to 7689.24. 10 year yield also closed up 0.056 to 2.975 and is on track to 3.000 handle again. But Dollar lagged behind and continues to trade as the second weakest for the week, just next to slightly better than Yen.

NASDAQ’s performance was impressive as it made new record high. For the near term, further rise is expected for sure. But it’s possible that the consolidation pattern this year, from 7505.77 with five waves to 6026.97, is a triangle pattern in wave four position. If that’s the case, rise from 6026.97 will be a strong but short lived thrust as the fifth wave to complete a larger up move. We’ll see whether the scenario plays out like this. But 8000 handle will be a key to watch.

German 10 yield bund yield breaches 0.5%, takes Euro higher

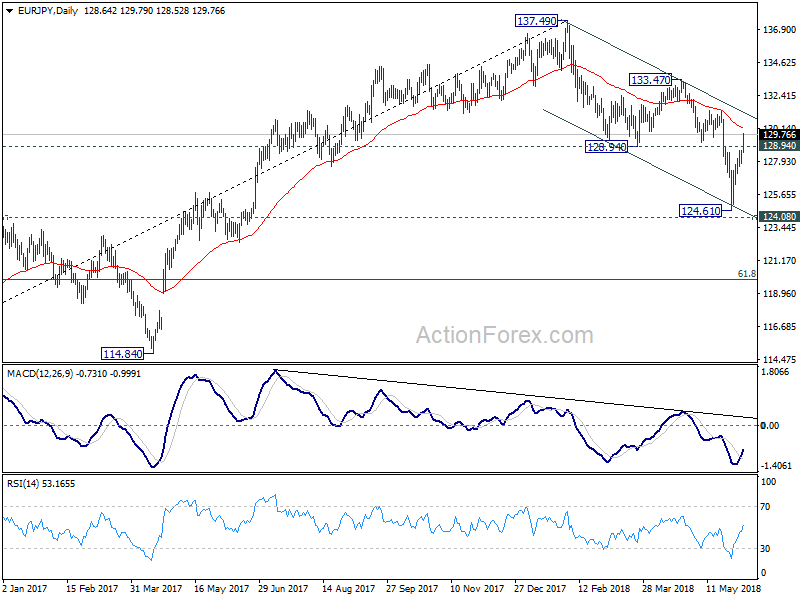

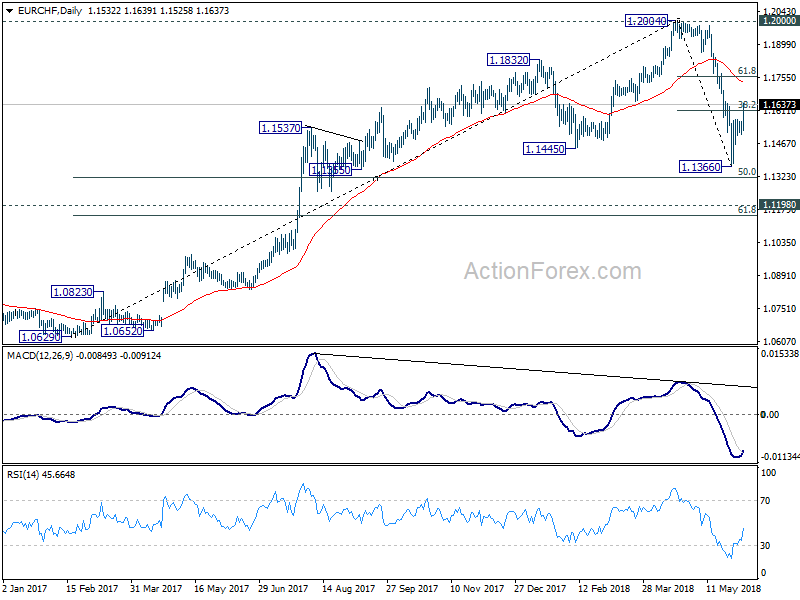

European majors are trading broadly higher today as boosted by surging major benchmark yields.

German 10 year bund yield reaches as high as 0.513 and continues to press 0.5 handle.

UK 10 year gilt yield also surges to as high as 1.421 and is trying to stay firm above 1.4.

Charts from MarketWatch.