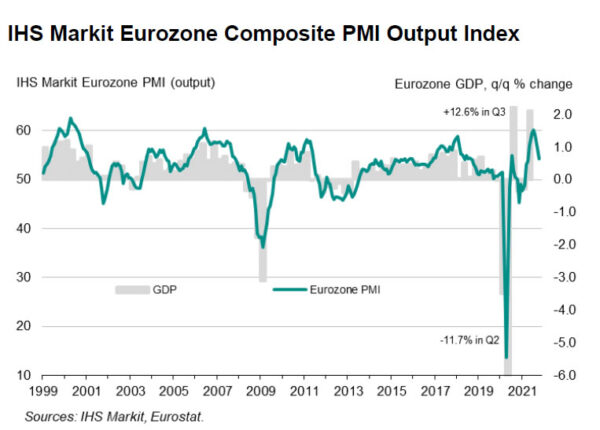

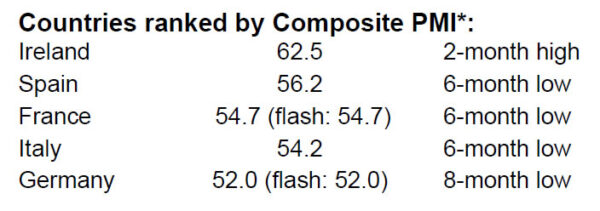

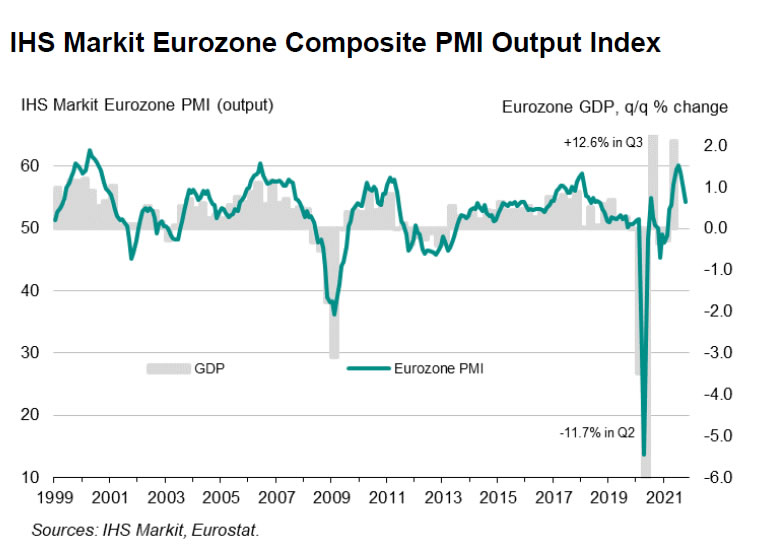

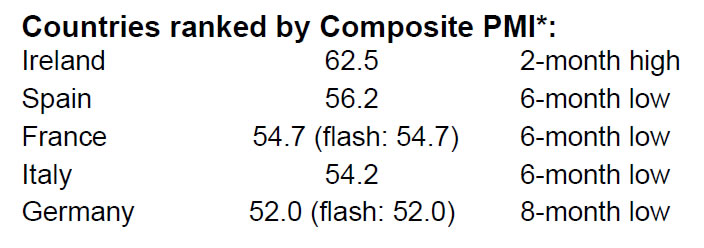

Eurozone PMI Services was finalized at 54.6 in October, down from September’s 56.4. PMI Composite was finalized at 54.2, down from September’s 56.2. Looking at some member states, Ireland PMI composite rose to 2-month high at 62.5. Spain dropped to 6-month low at 56.2. France dropped to 6-month low at 54.7. Italy dropped to 6-month low at 54.2. Germany dropped to 8-month low at 52.0.

Chris Williamson, Chief Business Economist at IHS Markit said:

“Eurozone growth has slowed sharply at the start of the fourth quarter, with manufacturing hamstrung by supply constraints and services losing momentum as the rebound from lockdowns fades.

“Despite the slowdown, the rate of expansion remains consistent with quarterly GDP growth of 0.5%, but there’s a worrying lack of clarity on the direction of travel in coming months.

“With supply shortages getting worse rather than better in October, manufacturing growth is likely to remain subdued for some time to come. That would leave the economy reliant on the service sector to drive growth, and there are already signs that rising virus case numbers are dampening activity in many service sector businesses, notably – but by no means exclusively – in Germany.

“Ongoing supply shortages meanwhile suggest that high price pressures will persist into next year, but as yet there are no signs of persistent strong wage growth, which would be the bigger concern for the longer-term inflation outlook.”

Full release here.

GBP/CHF continues consolidation pattern, targeting 1.104

GBP/CHF is so far one of the top movers for the week, even though over movements in the markets are rather indecisive. The decline from 1.1543 is seen as the third leg of the consolidation pattern from 1.1574. Deeper fall is expected as long as 1.1265 resistance holds.

Strong support could be seen around 1.1045 cluster (38.2% retracement of 1.1043) to complete the three-wave pattern. Break of 1.1265 resistance will bring stronger rise back to retest 1.1574. Nevertheless, sustained break of 1.1043/5 will be a sign of trend reversal, and target 61.8% retracement at 1.0714.