UK PMI Construction recovered to 45.3 in July, up from 43.1 (10 year low) but missed expectation of 46.0. And, it’s still the fifth straight month of sub-50 contraction reading. Markit noted that construction activity fell for the third month in a row. There was sharp drop in new work and purchasing activity during July. Business optimism also slid to its lowest since November 2012.

Tim Moore, Economics Associate Director at IHS Markit, which compiles the survey:

“UK construction output remains on a downward trajectory and another sharp drop in new orders has reduced the likelihood of a turnaround in the coming months.

“Total business activity declined at a softer pace than the ten-year record seen in June, but this should not detract attention from the challenges ahead for the construction sector. Customer demand has been squeezed on all sides in recent months, which has pushed down business expectations to the lowest since the second half of 2012.

“July data revealed declines in house building, commercial work and civil engineering, with all three areas suffering to some degree from domestic political uncertainty and delayed decision-making.

“Construction companies have started to respond to lower workloads by cutting back on input buying, staffing numbers and sub-contractor usage. If the current speed of construction sector retrenchment is sustained, it will soon ripple through the supply chain and spillovers to other parts of the UK economy will quickly become apparent.”

Full release here.

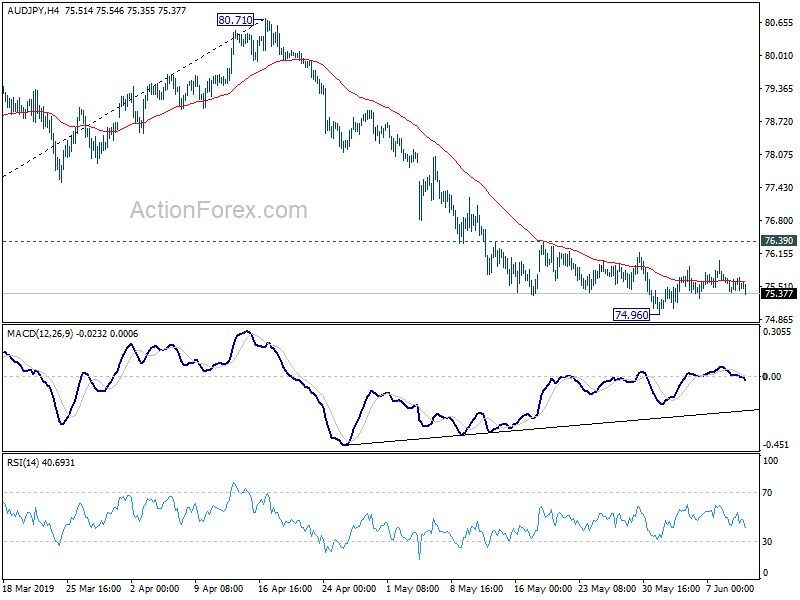

USDCAD head and shoulder top threatening bearish reversal

USD/CAD’s selloff accelerates as the US session goes on, as supported by NAFTA news. The break of 1.2814 support now raise the chance of a head and shoulder top reversal pattern. (ls: 1.3000; h: 1.3124; rs: 1.2942). But for now, we’d prefer to see sustained break of 38.2% retracement of 1.2246 to 1.3124 at 1.2789 to confirm.

Also bare in mind that such near term reversal would also indicate rejection by 38.2% retracement of 1.4689 to 1.2061 at 1.3065. And in that case, the rebound from 1.2061 could have completed as a corrective three waves pattern to 1.3124 too. And in that case, 1.2061/2246 support zone will be back in sight.

For now, we’ll wait and see if 1.2789 would be firmly taken out.