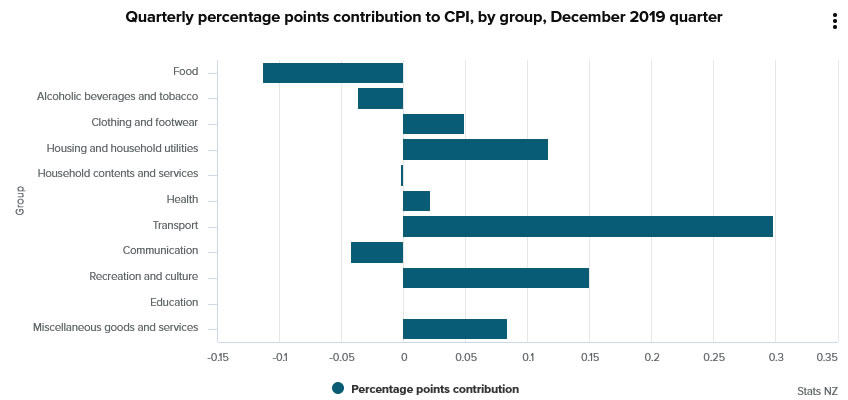

New Zealand ANZ Business Confidence dropped to -53.5 in September, down from -52.3. That’s also the worst reading since April 2008. Agriculture scored weakest confidence at -75.6 while manufacturing was best at -46.2. Activity outlook also dropped to -1.8, down from -0.5. Activity outlook was worst in construction at -7.1, best at services at -0.6.

ANZ noted that RBNZ will be “disappointed that its unexpectedly large 50bp cut in the Official Cash Rate last month does not appear to have had much impact on business’ sentiment or investment and employment intentions.” And, “prolonged lack of confidence is starting to feed its way through the economy and is threatening the tight labour market.” Also, “this gradual but prolonged economic slowdown is at risk of ceasing to be about the data and starting to become about the people.

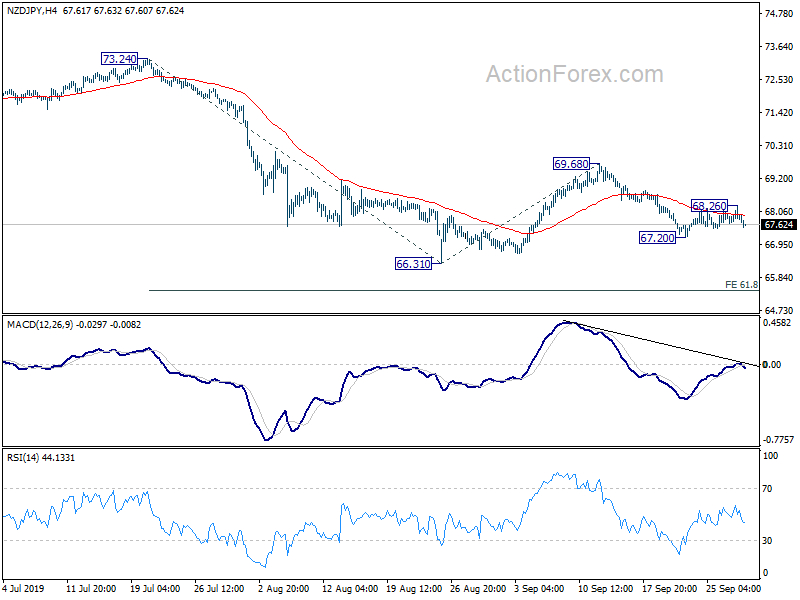

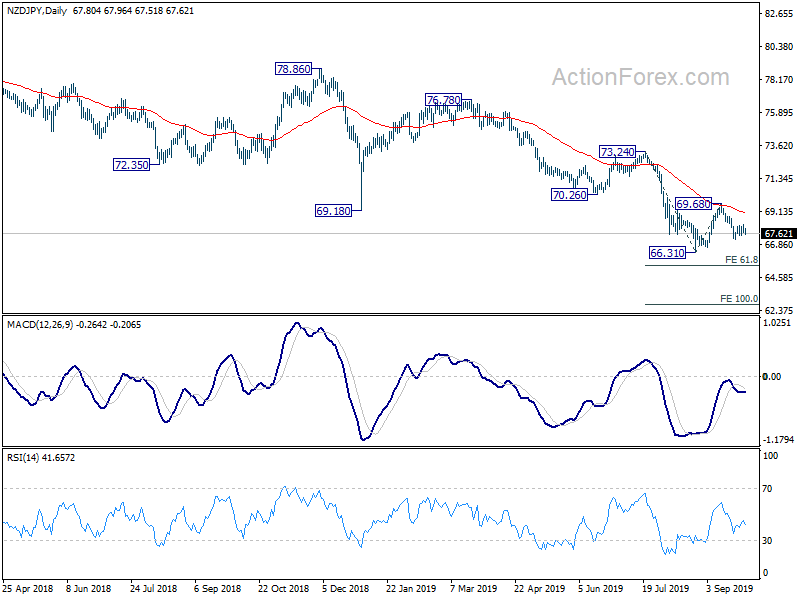

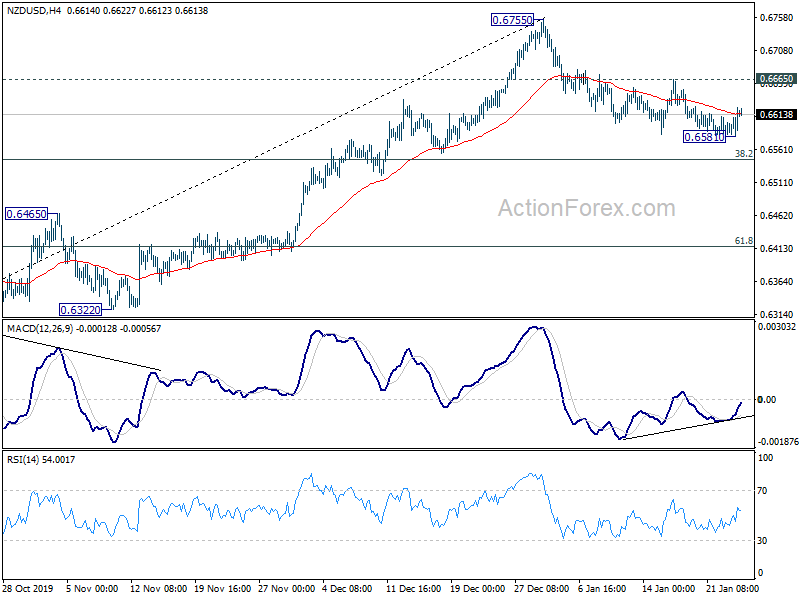

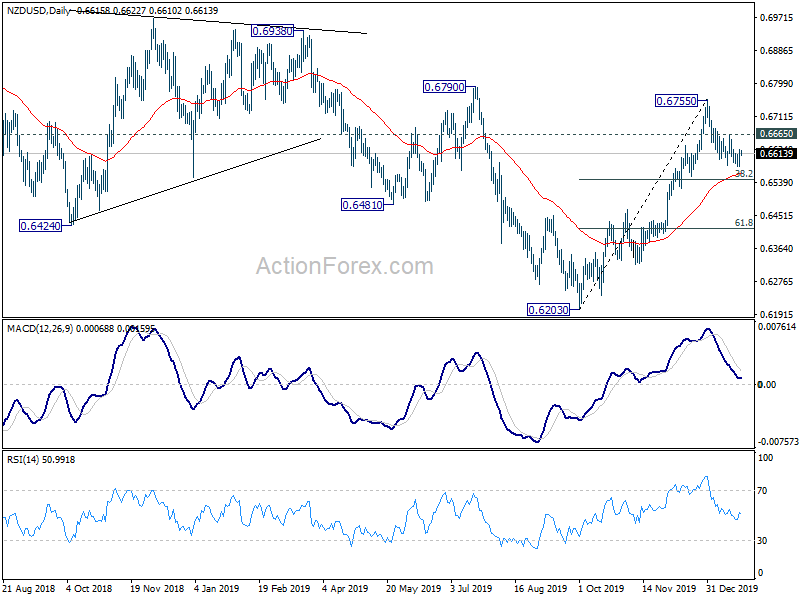

Today’s decline in NZD/JPY the release suggests the corrective recovery from 67.20 has completed at 68.26, after failing to sustain above 4 hour 55 EMA. Focus is immediately back on 67.20 and break will target a test on 66.31 low. Overall, NZD/JPY is clearly staying in near term down trend, held well by falling 55 day EMA. Next target is 61.8% projection of 73.24 to 66.31 from 69.68 at 65.39, and then 100% projection at 62.75.

European Update: Sterling recovers, bears refuses to commit

Sterling rebounds broadly today, except versus Kiwi, as bears refuse to commit further selling. Stronger than expected UK wage growth in September does provide some support. But more importantly, there are rumors flying around about an imminent Brexit deal with the EU. It’s reported that the “texts” are ready and they’re just waiting for the nod from UK Prime Minister Theresa May. We’ll see if both sides can really agree on something that paves the way to a November EU summit.

Australian and New Zealand Dollar are also strong on improved sentiment over optimism on US-China trade spat. China Vice Premier Liu He might travel to the US to meet with Treasury Secretary Steven Mnuchin shortly, to prepare for the meeting between Trump and Xi on November 30 at the G20 summit. Yen and Dollar are trading as the weakest ones, paring some of this week’s gain. Canadian Dollar is back under pressure as WTI crude oil resumes recent free fall and hit as low as 58.33.

In other markets, major European indices are trading higher at the time of writing:

Earlier in Asia