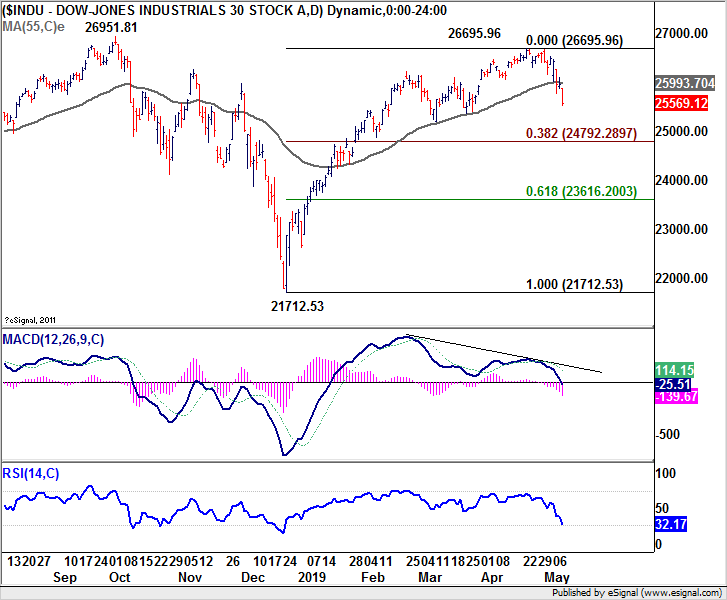

US stock markets are in deep selloff today on trade war concerns. At the time of writing, DOW is down -365 pts or -1.41%. S&P 500 is down -1.39%. NASDAQ is down -1.59%. 10-year yield is down -0.047 at 2.435. Technically, the near term outlook in the indices are rather bearish too.

Regarding DOW, firstly, rise from 21712.53 is seen as the second leg of medium to long term consolidation pattern from 26951.81. (S&P 500 and NASDAQ broke respective historical highs but couldn’t sustain above. So, that doesn’t violate the view that equivalent rebounds were the second legs of corrective patterns too). Secondly, 26695.96 was reasonably close to 26951.81 high. Thirdly, bearish divergence is seen in daily MACD. Fourthly, 55 day EMA is now firmly taken out today.

The developments suggest that rise from 21712.53 has completed at 26695.96 already. And fall from there should be the third leg of the above mentioned corrective pattern from 26951.81. Further decline should now be seen back to 38.2% retracement of 21712.53 to 26695.96 at 24792.28. Sustained break there should confirm our view and target 61.8% retracement at 23616.20 and below.

Meanwhile, a turn around in US-China trade negotiation could reverse the decline in stocks. But could Chines Vice Premier achieve that? Theoretically yes but unlikely.

ECB Lagarde: Eurozone contraction likely in between medium and severe scenarios

ECB President Christine Lagarde said the “mild” coronavirus economic scenario is now “out of date”. She added, “we’ll have a better sense in a few days as we publish our numbers in early June, but it’s likely we will be in between the medium and severe scenarios.” Eurozone economy is expected to contract between -8% to -12%.

The central bank is expected to expand the Pandemic Emergence Purchase Program next week. Lagarde said with respect to the PEPP, “this concerns the size but also the composition and the duration of the program.” She also talked down the risk of a new debt crisis as debt-servicing costs are “extremely low”. “All countries around the world had to respond, and as a result of that had to increase their debt,” she said. In the current coronavirus crisis, “use of debt is not only recommended, it’s the way to go.”