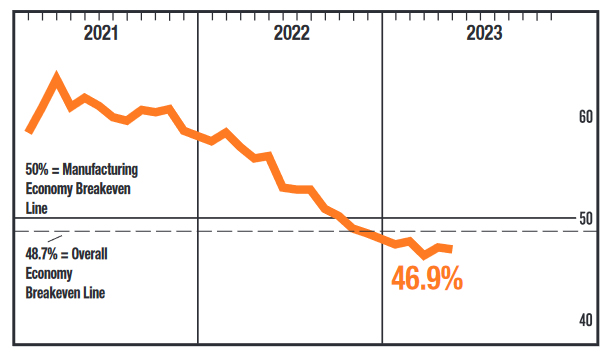

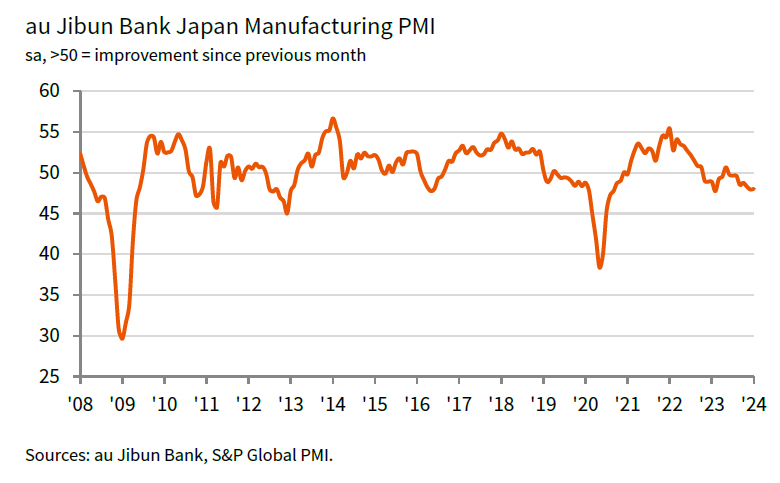

US ISM Manufacturing PMI dropped from 47.1 to 46.9 in May, below expectation of 47.0. Looking at some details, new orders dropped from 45.7 to 42.6. Production rose from 48.9 to 51.1. Employment rose from 50.2 to 51.4. Prices dropped sharply from 53.2 to 44.2.

ISM said: ” “This is the seventh month of contraction and continuation of a downward trend that began in June 2022. That trend is reflected in the Manufacturing PMI’s 12-month average falling to 49.4 percent.”

“The past relationship between the Manufacturing PMI and the overall economy indicates that the May reading (46.9 percent) corresponds to a change of minus-0.6 percent in real gross domestic product (GDP) on an annualized basis.”

Oil price in range ahead of pivotal OPEC meeting

WTI oil price is staying in range between 63.6/66.9 as markets await the pivotal meeting in Austria. Delegations of OPEC and non-OPEC oil producing countries are meeting today in Vienna. The producers are trying to reach a consensus on easing the output cap, that is raising production, to cool oil prices.

Saudi Arabia’s Energy Minister Khalid Al-Falih, the defacto leader of OPEC, said yesterday that he was “optimistic” on a deal as there was a “spirit of cooperation” among the group. And they would discuss how to raise production by around 1 million barrels per day.

The United Arab Emirates’ minister of energy and industry, and OPEC president, Suhail Al- Mazrouei emphasized that OPEC is “not a political organization” but a “commercial organization”. Iraq’s Oil Minister Jabbar Ali al-Luaibi also said he’s “confident that we will reach some sort of agreement”.

However, Iran, Iraq and Venezuela are known to oppose the relaxation of production cut. Iranian Oil Minister Bijan Zanganeh said he doubted OPEC could reach a deal this week and he was feeling “very good” about the current production levels.

Russian Energy Minister Alexander Novak warned that “Oil demand usually grows at the steepest pace in the third quarter … We could face a deficit if we don’t take measures.” And, “this could lead to market overheating.” Russia is pushing up to 1.5 million barrels per day of output raise, OPEC and non-OPEC countries together.

Full program of the meeting.