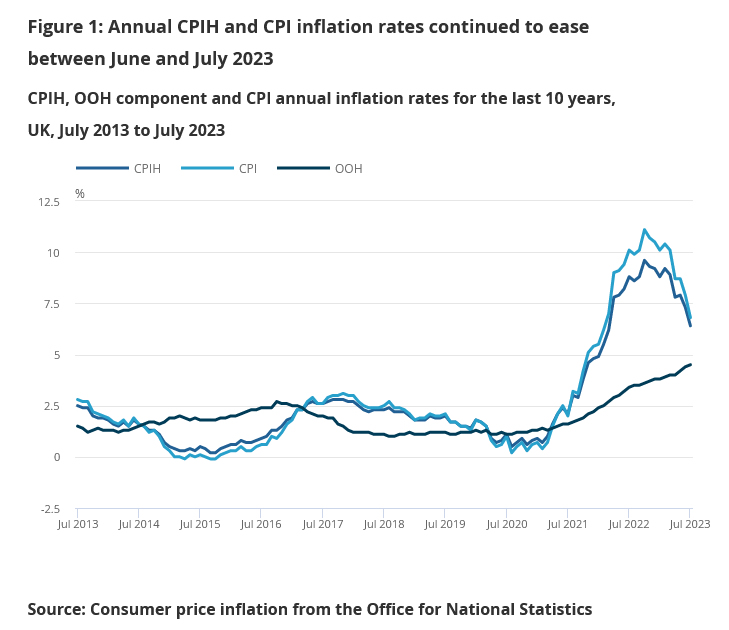

July saw a marked deceleration in UK’s CPI, falling from 7.9% yoy to 6.8% yoy , precisely in line with market expectations. Core CPI, which strips out variables like energy, food, alcohol, and tobacco, stood unchanged at 6.9% yoy, above the expected 6.8%.

CPI figures pertaining to goods showed a noticeable slowdown, dropping from 8.5% yoy to 6.1% yoy. On the flip side, CPI services ramped up from 7.2% yoy to 7.4% yoy , registering its peak since the staggering 9.5% yoy rate observed in March 1992.

On a month-to-month analysis for July, CPI receded by -0.4%, a figure slightly above than forecasted decline of -0.5%. Core CPI saw a monthly rise of 0.3% mom. While the CPI for goods plunged by -1.7% mom. , services CPI exhibited an increase, registering growth of 1.0% mom. .

Office for National Statistics remarked, “The slowdown in the annual CPI rate into July 2023 was driven by downward contributions to change from 8 of the 12 divisions.”

Notably, housing and household services emerged as the primary sectors applying downward pressure. Expanding on this, ONS stated, “Within this division, the downward effect came mainly from gas and electricity.”

US consumer confidence rose to 109.7, highest since Jan 2022

US Conference Board Consumer Confidence rose from 102.5 to 109.7 in June, well above expectation of 103.6. Present Situation Index rose from 148.9 to 155.3. Expectations Index jumped from 71.5 to 79.3, but remained below 80 which was associated with a recession within the next year.

“Consumer confidence improved in June to its highest level since January 2022, reflecting improved current conditions and a pop in expectations,” said Dana Peterson, Chief Economist at The Conference Board.

“Assessments of the present situation rose in June on sunnier views of both business and employment conditions.”

“Although the Expectations Index remained a hair below the threshold signaling recession ahead, a new measure found considerably fewer consumers now expect a recession in the next 12 months compared to May.”

Full US consumer confidence release here.