Japan’s industrial production expanded for the second consecutive month, recording a 0.8% mom growth in March, surpassing the expected 0.4% mom increase. The growth was driven by output in eight sectors, led by motor vehicles, while declines were observed in seven sectors, including electronic components and devices.

The Ministry of Economy, Trade and Industry upgraded its basic assessment for the month, stating that industrial production was “showing signs of moderately picking up” as parts supply shortages continued to ease. This is a marked improvement from the previous month’s assessment of “weakening.” The ministry also projects a further 4.1% growth in industrial production for April and a -2.0% decline in May.

Other economic indicators released include 7.2% yoy increase in retail sales for March, surpassing expectations of 6.5% yoy. However, unemployment rate rose for the second month in a row, reaching 2.8%, above expectation of 2.5%.

April, Tokyo core CPI, which excludes fresh food, accelerated from 3.2% to 3.5% yoy, exceeding expectations of 3.2% yoy. Core-core CPI, which excludes fresh food and fuel costs, accelerated from 3.4% to 3.8% year-on-year, marking the highest rate since April 1982.

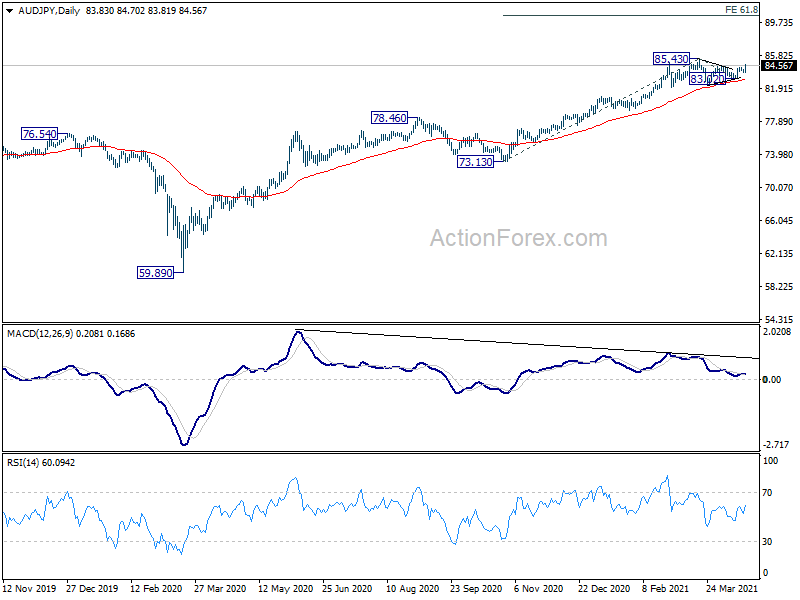

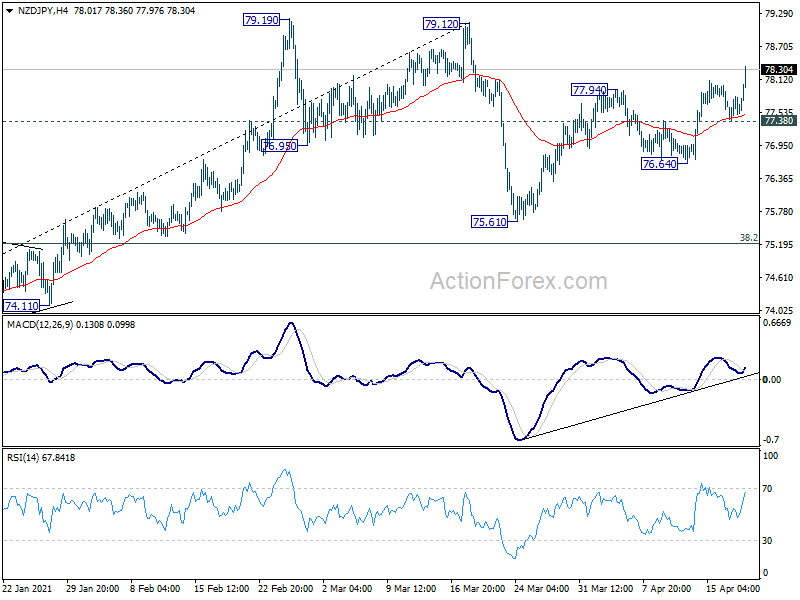

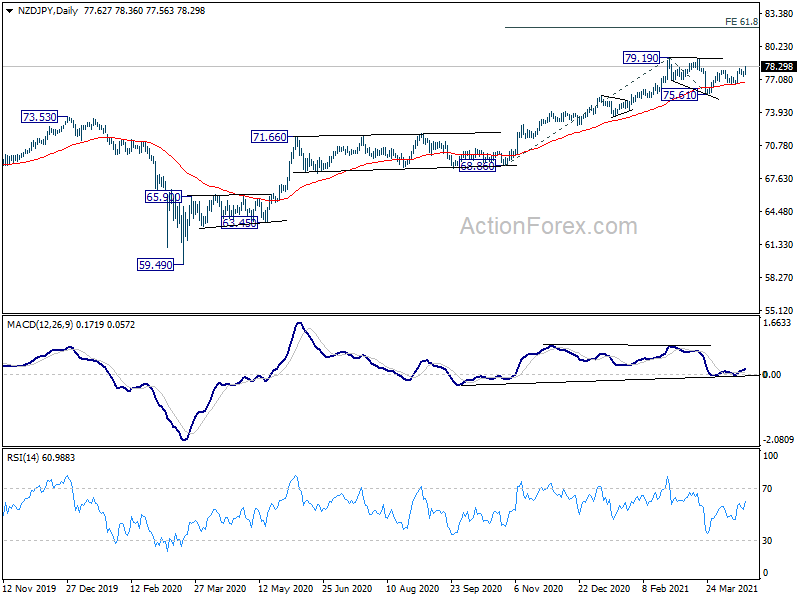

In to US session: A look at AUDUSD and EURCHF

Heading into US session, CHF and JPY are notably higher against others. Commodity currencies are the weakest, together with EUR.

The surge in USD/CAD earlier in European session first caught out attention. As mentioned earlier, it’s on course for 1.3124 resistance.

Selling of AUD and EUR came in later. AUD/USD traders should have finally made up them mind to push the pair through 0.7500 key support level. Such development should confirm medium term reversal in the pair and should pave the way to 0.7328 support next.

Also, the steep fall in EUR/CHF suggests that it’s finally being rejected by 1.2 key handle. Break of 1.1888 support will confirm near term reversal. And deeper pull back should be seen to 38.2% retracement of 1.1445 to 1.2004 at 1.1790 next.