BoE is widely expected to continue tightening today, though the extent of interest rate hike remains a point of contention. Markets currently slightly favor a 25 bps increment to 5.25%. However, a more aggressive 50bps hike to 5.50% cannot be entirely dismissed. The Bank’s unexpected 50bps raise in June took markets by surprise, leading some economists to posit a strategic shift in the institution’s response strategy. Conversely, CPI for June, which slowed more-than-expected to 7.9%, was perceived as a positive development by BoE policymakers, and could argue for a return to slowing tightening.

Regardless of today’s decision, it is widely understood that this will not conclude the ongoing tightening cycle. Compared to ECB and Fed, BoE is anticipated to continue tightening for an extended period. Nonetheless, expectation of terminal rate has been fluctuating widely recently though, swinging from as high as 6.5% to 5.75% in a matter of weeks, suggesting a persisting uncertainty about the path ahead.

In addition to the anticipated rate decision, market observers will be closely watching two key aspects. First, today’s voting could provide insight into the approach of MPC’s newest member, Megan Greene, who recently succeeded known dove Silvana Tenreyro. If Greene presents a less dovish stance, Swati Dhingra may stand out as the only dissenter, making the vote an 8-1 majority.

Secondly, BoE is also set to release its new economic forecasts. Governor Andrew Bailey has repeatedly suggested that inflation is expected to decline fairly swiftly in the second half of the year, prompting keen interest in whether this prediction will still be reflected in the forthcoming projections.

Here are some readings on BoE:

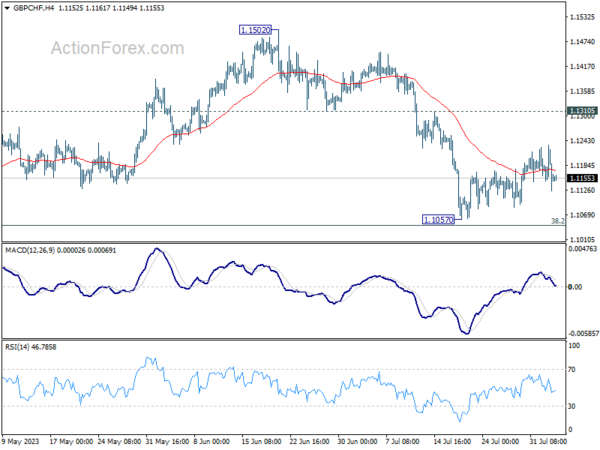

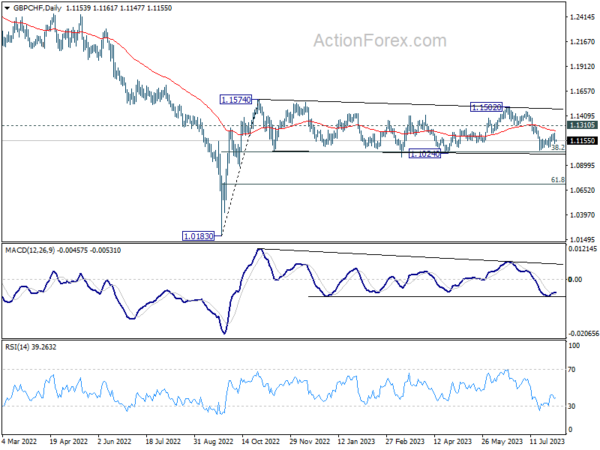

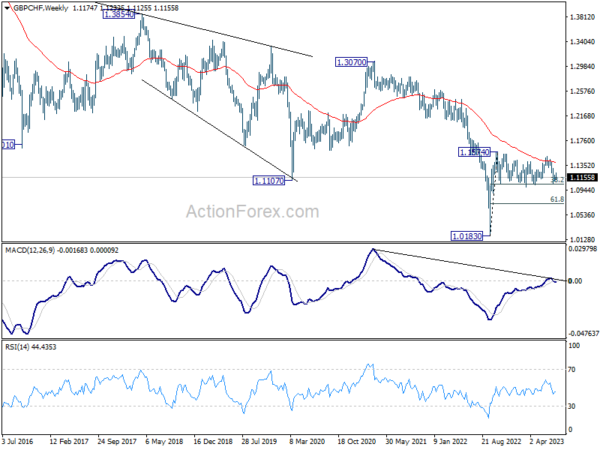

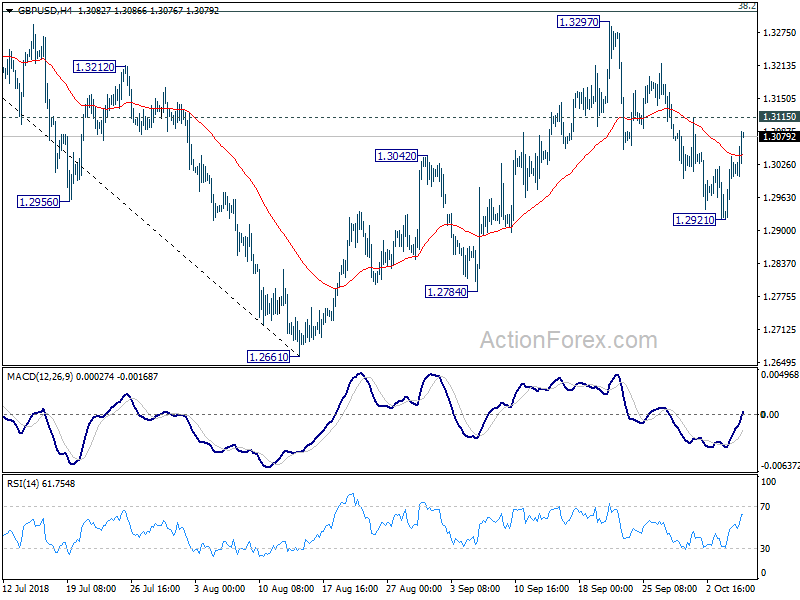

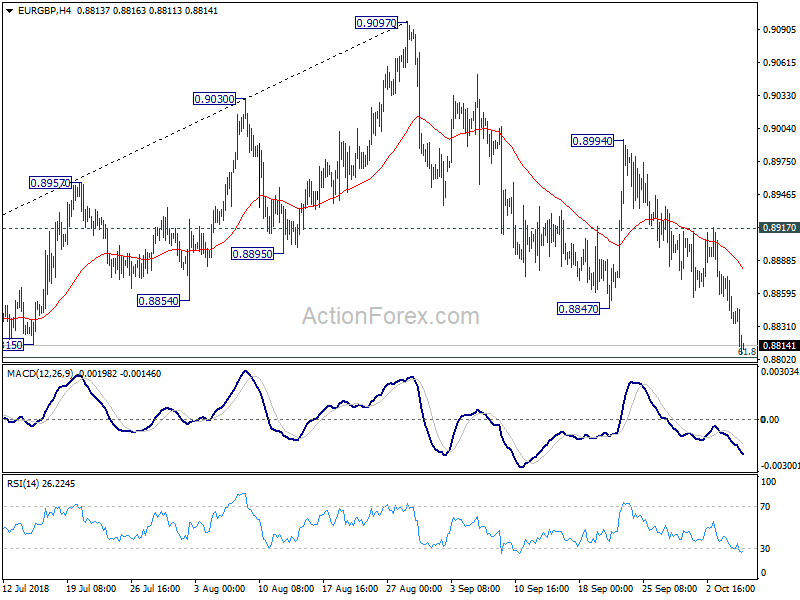

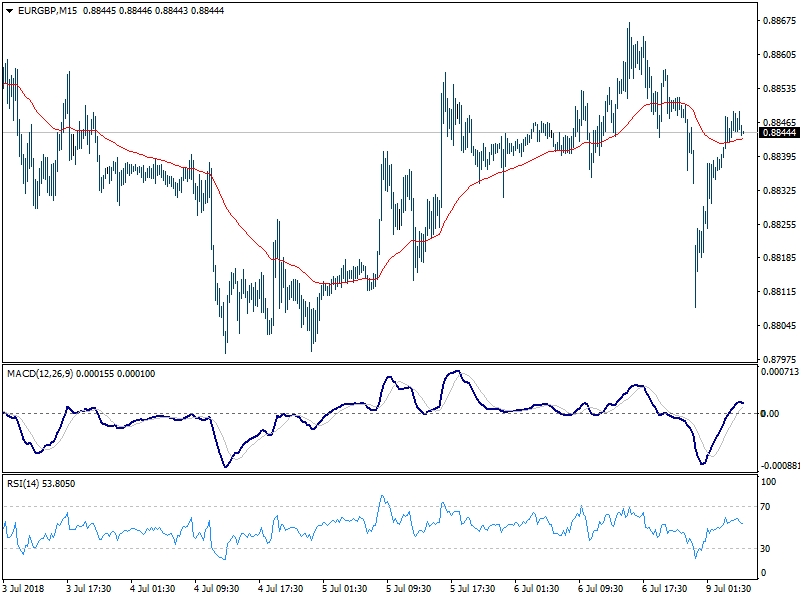

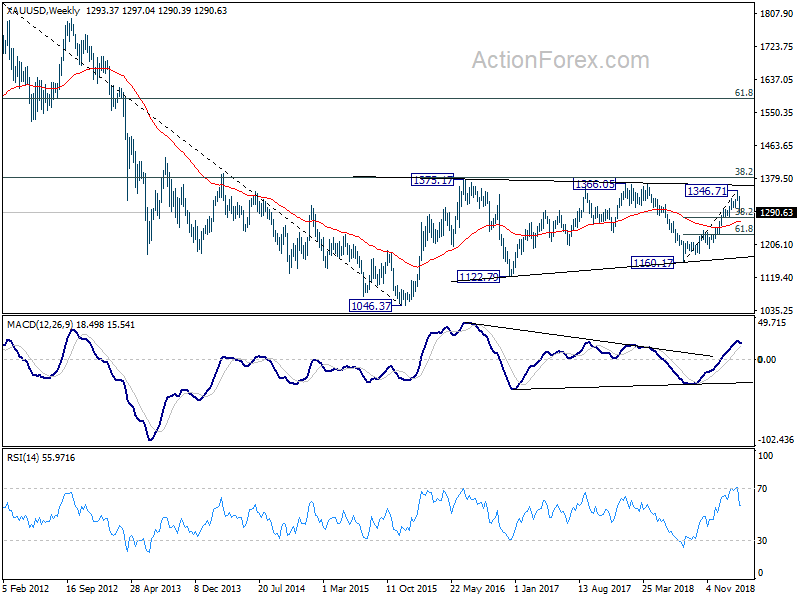

GBP/CHF’s technical picture is mixed for now, with some dovish favor. From the near term angle, recovery from 1.1057 is clearly corrective looking, favoring a downside breakout. But the pair has been trading in medium term range of 1.1024/1574 since last October, keeping it neutral-at-worst. Yet, prior rejection by 55 W EMA is keeping the long term outlook bearish to neutral-at-best.

Still, further fall is more likely than not as long as 1.3105 support turned resistance zone. Decisive break of 1.1024 will bring deeper decline to 38.2% 1.0183 to 1.1574 at 1.0714 in rather quick manner. Let’s see how GBP/CHF would reaction to today’s BoE announcement.

BoE to hike for sure, but by 25bps or 50bps?

BoE is widely expected to continue tightening today, though the extent of interest rate hike remains a point of contention. Markets currently slightly favor a 25 bps increment to 5.25%. However, a more aggressive 50bps hike to 5.50% cannot be entirely dismissed. The Bank’s unexpected 50bps raise in June took markets by surprise, leading some economists to posit a strategic shift in the institution’s response strategy. Conversely, CPI for June, which slowed more-than-expected to 7.9%, was perceived as a positive development by BoE policymakers, and could argue for a return to slowing tightening.

Regardless of today’s decision, it is widely understood that this will not conclude the ongoing tightening cycle. Compared to ECB and Fed, BoE is anticipated to continue tightening for an extended period. Nonetheless, expectation of terminal rate has been fluctuating widely recently though, swinging from as high as 6.5% to 5.75% in a matter of weeks, suggesting a persisting uncertainty about the path ahead.

In addition to the anticipated rate decision, market observers will be closely watching two key aspects. First, today’s voting could provide insight into the approach of MPC’s newest member, Megan Greene, who recently succeeded known dove Silvana Tenreyro. If Greene presents a less dovish stance, Swati Dhingra may stand out as the only dissenter, making the vote an 8-1 majority.

Secondly, BoE is also set to release its new economic forecasts. Governor Andrew Bailey has repeatedly suggested that inflation is expected to decline fairly swiftly in the second half of the year, prompting keen interest in whether this prediction will still be reflected in the forthcoming projections.

Here are some readings on BoE:

GBP/CHF’s technical picture is mixed for now, with some dovish favor. From the near term angle, recovery from 1.1057 is clearly corrective looking, favoring a downside breakout. But the pair has been trading in medium term range of 1.1024/1574 since last October, keeping it neutral-at-worst. Yet, prior rejection by 55 W EMA is keeping the long term outlook bearish to neutral-at-best.

Still, further fall is more likely than not as long as 1.3105 support turned resistance zone. Decisive break of 1.1024 will bring deeper decline to 38.2% 1.0183 to 1.1574 at 1.0714 in rather quick manner. Let’s see how GBP/CHF would reaction to today’s BoE announcement.