US equities ended mixed in Wednesday’s session, following Fed’s expected rate increase by 25 bps to 5.25-5.50%. Despite the major policy decision, market volatility was surprisingly restrained throughout the trading session. Fed Chair Jerome Powell indicated that another rate hike could be on the table for September, while steering clear of predicting when a rate cut might transpire, pointing to the prevailing high economic uncertainty.

Current market expectations for additional rate hikes this year stand at 22% for September, 33% for November, and 30% for December. The likelihood of a rate cut commencing as early as March next year is considered to be 55.8%.

Powell, in the post-meeting press conference, stated, “It is certainly possible we would raise the funds rate at the September meeting if the data warranted, and I would also say it’s possible that we would choose to hold steady at that meeting”. He emphasized that Fed’s monetary policy decisions will continue to be formulated on a meeting-by-meeting basis, largely dependent on economic data and indicators.

When discussing potential rate cuts, Powell asserted, “We’d be comfortable cutting rates when we’re comfortable cutting rates,” suggesting that a cut could take place next year if inflation hovers consistently near the Fed’s target. However, he stressed that this scenario remains a considerable ‘if,’ given the considerable uncertainty surrounding future economic developments and subsequent policy meetings.

More on FOMC

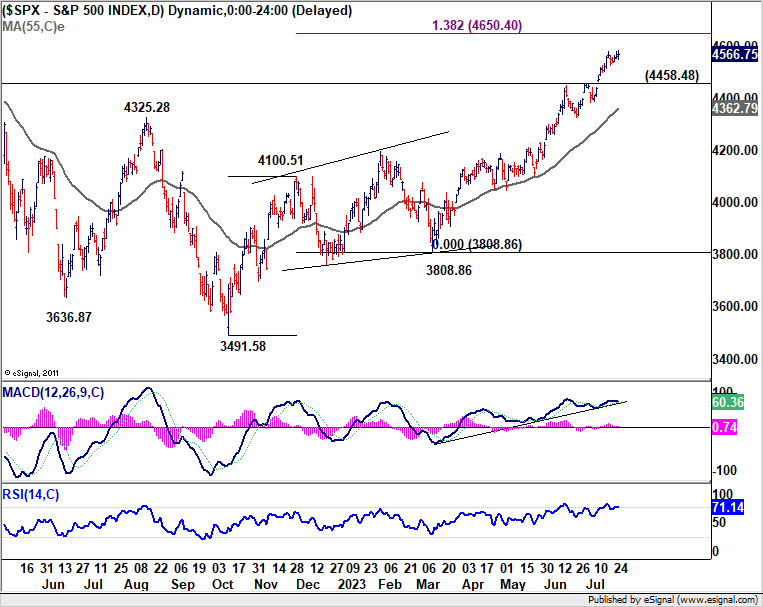

S&P 500 closed down slightly by -0.02% overnight. The index continued to lose upside momentum as seen in D MACD. While further rise cannot be ruled out, upside would likely be limited by 138.2% projection of 3491.58 to 4100.51 from 3808.86 at 4650.40. Meanwhile, break of 4458.48 resistance turned support will confirm that a correction is at least underway, and target 55 D EMA (now at 4362.79) and below.

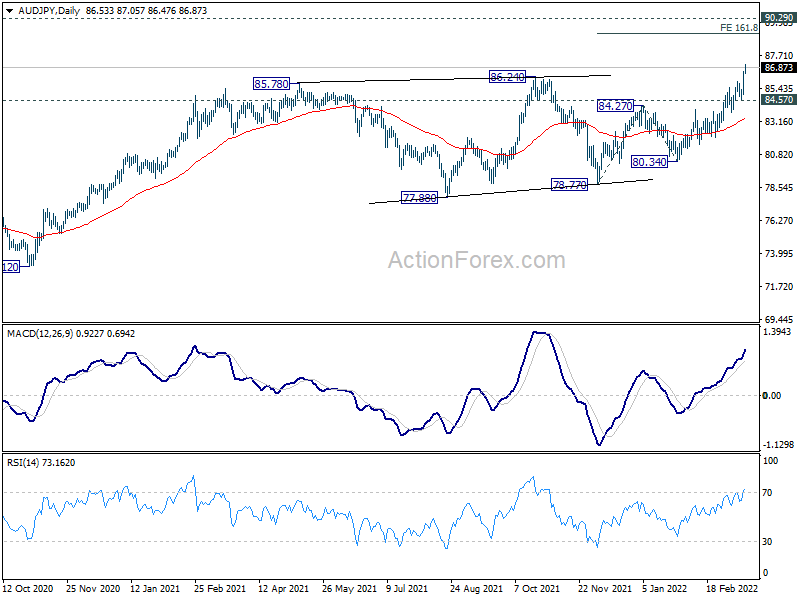

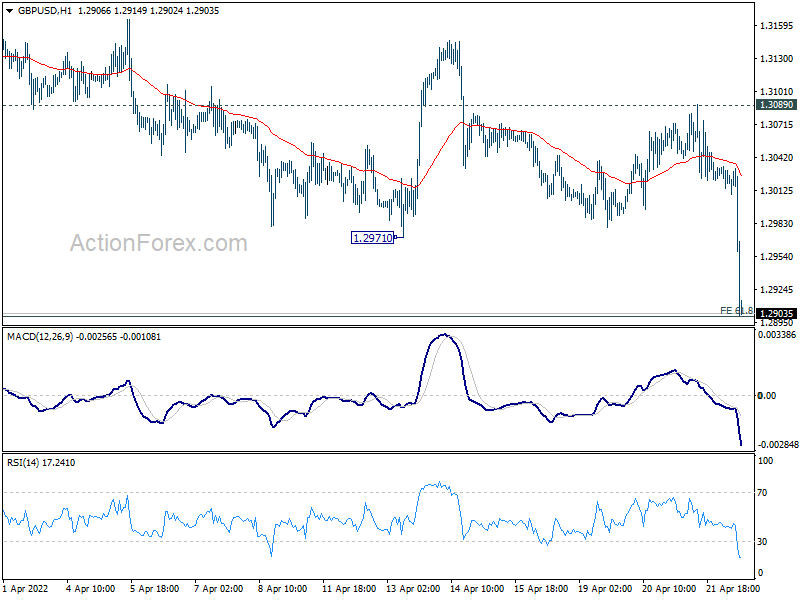

Today’s top mover: AUD/JPY completed post flash crash rebound

AUD/JPY is currently the top mover for today, down over -1.6%. Australian Dollar is knocked down by comments from RBA Governor Philip Lowe. Meanwhile, Yen is lifted by falling global treasury yields. Yen crosses also generally display signs of bearish reversal.

Back to AUD/JPY, current development argues that corrective rebound from 70.27 flash crash low has completed at 79.84 already. This is supported by mild bearish divergence condition in 4 hour MACD, as well as rejection by 55 day EMA. Focus is now on 77.51 support. Break there will confirm this bearish case.

As the 70.27 is an abnormal spike low, it’s hard to judge whether it would be taken out in near term at this point. The momentum through 77.51 should be watched to assess the chance. But in any case, risk will now stay on the downside as long as 79.84 holds, even in case of strong recovery.