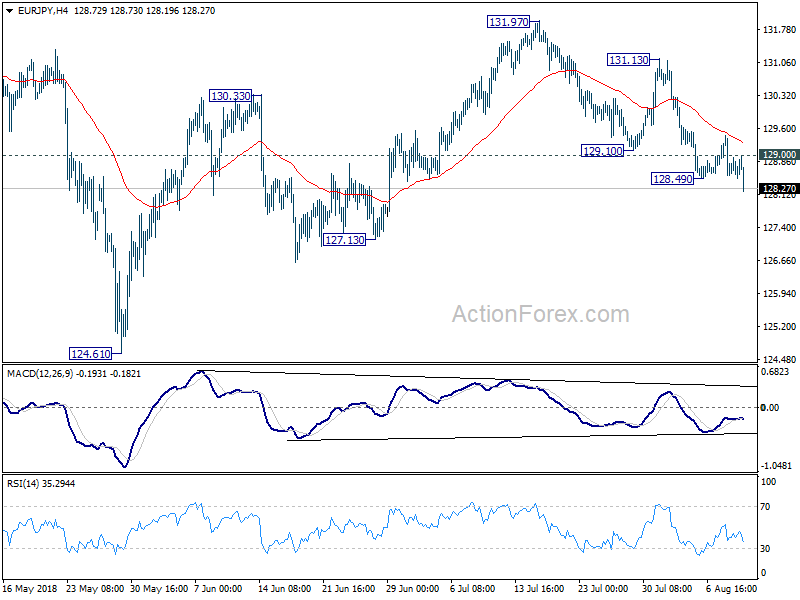

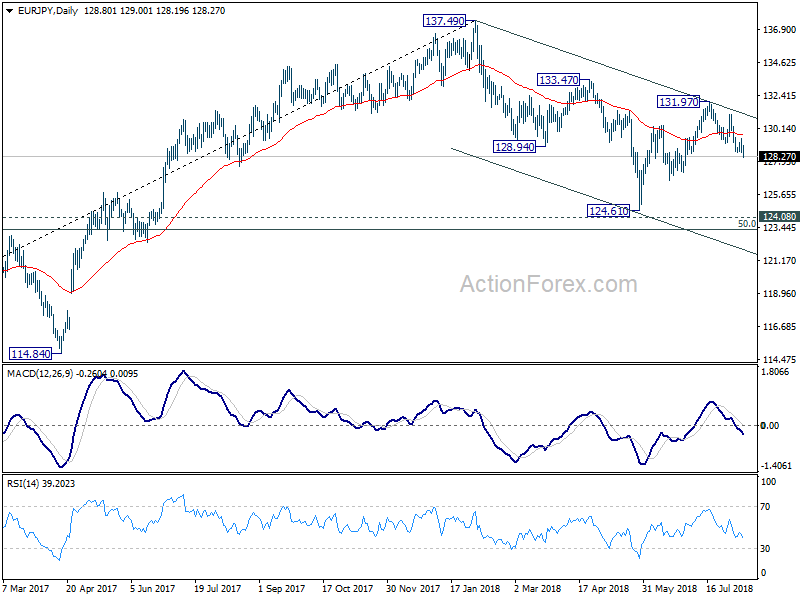

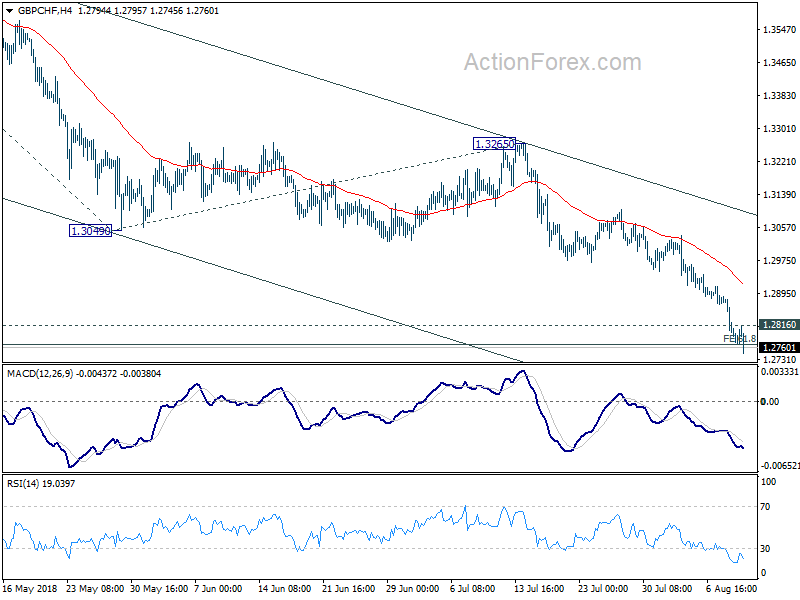

Statement by Reserve Bank Governor Adrian Orr:

Tena koutou katoa, welcome all.

The Official Cash Rate (OCR) remains at 1.75 percent. We expect to keep the OCR at this level through 2019 and into 2020, longer than we projected in our May Statement. The direction of our next OCR move could be up or down.

While recent economic growth has moderated, we expect it to pick up pace over the rest of this year and be maintained through 2019.

Robust global growth and a lower New Zealand dollar exchange rate will support export earnings. At home, capacity and labour constraints promote business investment, supported by low interest rates. Government spending and investment is also set to rise, while residential construction and household spending remain solid.

The labour market has tightened over the past year and employment is roughly around its maximum sustainable level. We expect the unemployment rate to decline modestly from its current level.

There are welcome early signs of core inflation rising. Inflation will increase towards 2 percent over the projection period as capacity pressures bite. This path may be bumpy however, with one-off price changes from global oil prices, a lower exchange rate, and announced petrol excise tax rises expected. We will look through this volatility as appropriate, and only respond to any persistent movements in inflation.

Risks remain to our central forecast. The recent moderation in growth could last longer. Low business confidence can affect employment and investment decisions. Conversely, there is a chance that inflation could increase faster if cost pressures can pass through into higher prices and impact inflation expectations.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

Meitaki, thanks.

Known dove Chicago Fed Evans turns hawkish, suggesting interest rates could become restrictive

The known dove Chicago Fed President Charles Evans started to turn hawkish in his comments to reports yesterday. Evans said the the economy is “extremely strong” and it’s “really a very good period of time” for both the economy and monetary policy setting. And Fed funds rate might eventually enter into “somewhat restrictive” area as economy strengthens while inflation stays above target.

He also noted that “inflation has moved up to 2 percent essentially”. There is “good reason to expect we will stay in that area.” Also, if inflation continues to be “on the order of 2, 2.2”, that “suggests only a modest amount of restrictiveness above our neutral rate might be called for in 2020.” And, “it would not surprise me at all if we make a judgment to move to a somewhat restrictive setting.” He cited it could be roughly 0.5% above his neutral rate of 2.75%.

Evans also downplayed the impact of Trump’s trade policy. He said “you size up the tariffs, the increases in input costs … and you find that while it sounds like a big number … the actual effect on industry output and GDP is still measured in a few tenths”of a percentage point. And, “the magnitude still seems to be relatively small, uncertain, against a context where the economy is very strong and we have just added quite a lot of fiscal stimulus.”