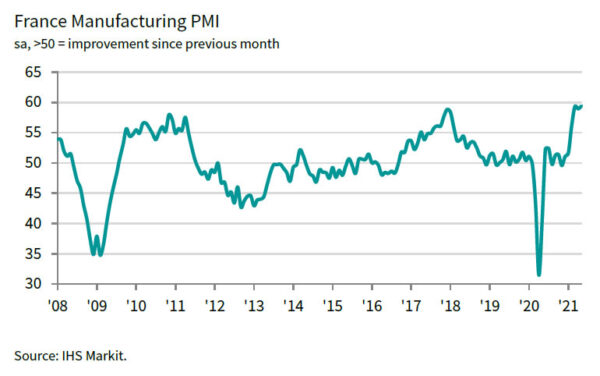

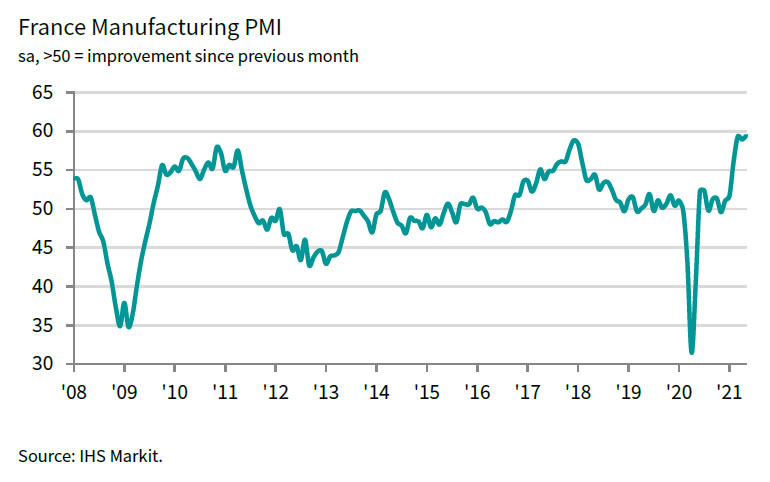

France PMI Manufacturing was finalized at 59.4 in May, up from April’s 58.0. That’s was also the highest level since September 2000. Both output and new orders rose at sharpest rates since January 2018. Accumulation of backlogs was steepest since November 2006. Rise in selling prices was near-record amid further acceleration of cost inflation.

Andrew Harker, Economics Director at IHS Markit, said: “Demand and production volumes continued to ramp up in the French manufacturing sector during May, with the loosening of lockdown restrictions playing a key part in this last month.

“The key challenge now for firms is being able to keep up with workloads. This is proving to be a struggle amid severe supply-chain delays and a lack of material availability. As a result, levels of backlogged work are rising sharply. We are therefore likely to see further expansions to production in the months ahead should some of these constraints start to ease, with hopefully more jobs created to help deal with backlogs.

“Inflationary pressures showed little sign of abating. On the contrary, input costs increased at the fastest pace for a decade, with output price inflation the second-fastest on record.”Commenting on the latest survey results, Andrew Harker, Economics Director at IHS Markit, said: “Demand and production volumes continued to ramp up in the French manufacturing sector during May, with the loosening of lockdown restrictions playing a key part in this last month.

“The key challenge now for firms is being able to keep up with workloads. This is proving to be a struggle amid severe supply-chain delays and a lack of material availability. As a result, levels of backlogged work are rising sharply. We are therefore likely to see further expansions to production in the months ahead should some of these constraints start to ease, with hopefully more jobs created to help deal with backlogs. “Inflationary pressures showed little sign of abating. On the contrary, input costs increased at the fastest pace for a decade, with output price inflation the second-fastest on record.”

Full release here.

RBA cuts rate to 0.25%, starts government bond purchases

RBA announces a package of coronavirus response today. Firstly, cash rate is cut by 25bps to 0.25%. Additionally, the central bank will start purchases of government bonds to keep 3 year yield at around 0.25%, starting tomorrow. A three-year funding facility will also be set up to provide credit support to small and medium-sized businesses. Lastly, exchange settlement balances will be remunerated at 10 basis points, instead of zero.

The central said, “the various elements of this package reinforce one another and will help to lower funding costs across the economy and support the provision of credit, especially to small and medium-sized businesses.” “Today’s policy package from the Reserve Bank complements the welcome fiscal response from governments in Australia. Together, these measures will support jobs, incomes and businesses through this difficult period and they will also assist the Australian economy in the recovery.”

Full statement here.