EUR/USD finally breaks out to the downside after Fed hikes 75bps and projects interest rate to hit 4.4% by year end. For the near term, EUR/USD’s next target is 100% projection of 1.0368 to 0.9863 from 1.0197 at 0.9692, and then 161.8% projection at 0.9380.

For the medium term, next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694.

In any case, break of 1.0049 minor resistance is needed to indicate short term bottoming. Or, outlook will stay bearish even in case of recovery.

San Francisco Fed President Mary Daly noted overnight that the risks of over-tightening versus under-tightening are currently “roughly balanced”.

The tightening of financial conditions, as indicated by surging treasury yields, may influence the extent of Fed’s policy adjustments.

Daly noted, “If that’s tight, maybe the Fed doesn’t need to do as much. That’s why I said, depending on whether it unravels, or whether the momentum in the economy changes, that could be equivalent to another rate hike.”

However, Daly remains watchful, indicating that depending on economic momentum and other variables, “that could be equivalent to another rate hike.”

Beyond domestic considerations, Daly expressed concerns about “geopolitical uncertainty,” noting its potential impact on the US economy.

The repercussions of international events on elements like oil prices and export demand are being closely monitored by the Fed. She encapsulated the Fed’s vigilant stance by stating, “It’s part of a large dashboard of data”

ECB left main refinancing rate unchanged at 0.00% as widely expected. Regarding the asset purchase program, ECB decided to taper it from EUR 30B per month to EUR 15B per month after the end of September. And, the program will end after December 2018.

Press conference to start at 12:30GMT

By loading the video, you agree to YouTube’s privacy policy. Learn more

At today’s meeting, which was held in Riga, the Governing Council of the ECB undertook a careful review of the progress towards a sustained adjustment in the path of inflation, also taking into account the latest Eurosystem staff macroeconomic projections, measures of price and wage pressures, and uncertainties surrounding the inflation outlook.

Based on this review the Governing Council made the following decisions:

First, as regards non-standard monetary policy measures, the Governing Council will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of September 2018. The Governing Council anticipates that, after September 2018, subject to incoming data confirming the Governing Council’s medium-term inflation outlook, the monthly pace of the net asset purchases will be reduced to €15 billion until the end of December 2018 and that net purchases will then end.

Second, the Governing Council intends to maintain its policy of reinvesting the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Third, the Governing Council decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path.

Today’s monetary policy decisions maintain the current ample degree of monetary accommodation that will ensure the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

SNB, BoE and ECB rate decisions are the focuses of the day and all are expected to deliver 50bps rate hikes.

There are some talks that given SNB only meets every quarter, it may surprise the market by maintaining the pace of 75bps. But the balance is more towards a 50bps hike to 1.00%. Tightening bias should be maintained while some focuses will be on the rhetoric on Swiss Franc exchange rate.

BoE is expected to raise policy rate by 50bps to 3.50%. Some attention will be on the voting. Last month, only seven MPC members voted for the 75bps hike. Swati Dhingra voted for 50bps, while Silvana Tenreyro voted for 25bps.

ECB should raise the main refinancing rate by 50bps to 2.50%. Additionally, it would announce some key principles regarding quantitative tightening, but the details main only come later, probably at February’s meeting. The new economic projections would also be watched closely on the central banks view on the path of slowing inflation and recession.

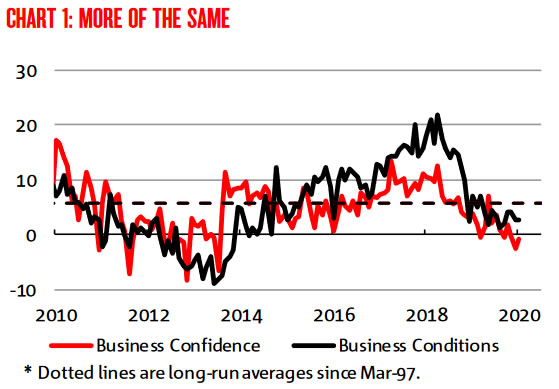

Australia NAB business confidence rose from -2 to -1 in January. Business conditions were unchanged at 3. Looking at some details, Trading conditions dropped from 6 to 5. Profitability conditions rose from 1 to 2. But employment conditions dropped sharply from 4 to 1.

Alan Oster, NAB Group Chief Economist warned: “The concern this month is the decline in employment. It is now below average and a worry given the labour market has been a bright spot in the economic data. That said, there is a risk that ongoing weakness in business activity sees a pull-back in hiring intentions”.

High level US-China trade negotiations started in the Diaoyutai state guest house in Beijing today, involving US Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer, and Chinese Vice Premier Liu He. Ahead of that, Mnuchin said he’s “looking forward to discussions today”. There was no elaborate and so far, there is no news leaked regarding the talks.

Trump indicated earlier this week that he’s willing to let the March 1 trade truce deadline slide a little bit. Trump further added that the talks are “going along very well” and the Chinese are “showing us tremendous respect.” Bloomberg reported that Trump is indeed considering to extend the deadline by 60 days, after rejecting the initial request by China of 90 days extension. But the rumor is not confirmed.

Yen trades generally lower on the news while Australian Dollar strengthens. But reactions from the stock markets are rather muted. Currently, Hong Kong HSI is down -0.4% and China SSE is down -0.04%.

Eurozone PMI manufacturing dropped to 56.0 in April, down from 56.6, miss expectation of 56.1. Eurozone PMI services rose to 55.0, up from 54.9 and beat expectation of 54.6. PMI composite unchanged at 55.2.

Comments from Chris Williamson, Chief Business Economist at IHS Markit:

“The Eurozone economy remained stuck in a lower gear in April, with business activity expanding at a rate unchanged on March, which had in turn been the slowest since the start of 2017. Growth has downshifted markedly since the peak at the start of the year, but importantly still remains robust.

“The April data are running at a level broadly consistent with Eurozone GDP growth of approximately 0.6% at the start of the second quarter.

“The decline in the PMI from January’s high is neither surprising nor alarming: such strong growth as that seen at the start of the year rarely persists for long, not least because supply fails to keep up with demand. With recent months seeing record delivery delays for inputs to factories and growing skill shortages, output is clearly being constrained. In France, strikes were also reported to have disrupted growth, and may continue to do so in coming months

“However, it’s also clear that underlying demand has weakened, in part due to exports being hit by the stronger euro. With companies’ future optimism having slipped to the lowest since last year, it looks likely that growth may well slow further in coming months.”

US House Speaker Paul Ryan told the NAFTA negotiation parties that May 17 is the deadline for the new NAFTA deal for eventual passage for the current Congress to vote on within this year. Ryan said “We have to have the paper – not just an agreement, we have to have the paper – from USTR by May 17 for us to vote on it this year, in December, in the lame duck”. But later, his spokesman said he referred to a notification of intent to sign the NAFTA agreement, not the full text. The new elected Congress will take office in January.

Canadian Foreign Minister Chrystia Freeland said after meeting with US legislators that “we are definitely getting closer to the final objective.”

Mexico’s Economy Minister Ildefonso Guajardo said he’ll know by the end of Friday ” if we really have what it takes to be able to land these things in the short run.”

EU Trade Commissioner Cecilia Malmstrom warned in a conference in France that WTO is in “deep crisis” and “we have to recognize this”. In particular, she said “if the appellate body collapses, which probably it will in December – at least temporarily – we will have no enforcement. And if you have no rules everybody can do whatever they want.”

At the same conference, WTO Director General Alan Wolff said “you get into a possible scenario where a country that lost (a case) says we appeal but there is no appeal which means the panel is not final. Then, “you could go to retaliation and counter-retaliation, which is what has happened between the U.S and China, which is certainly not good for the world.”

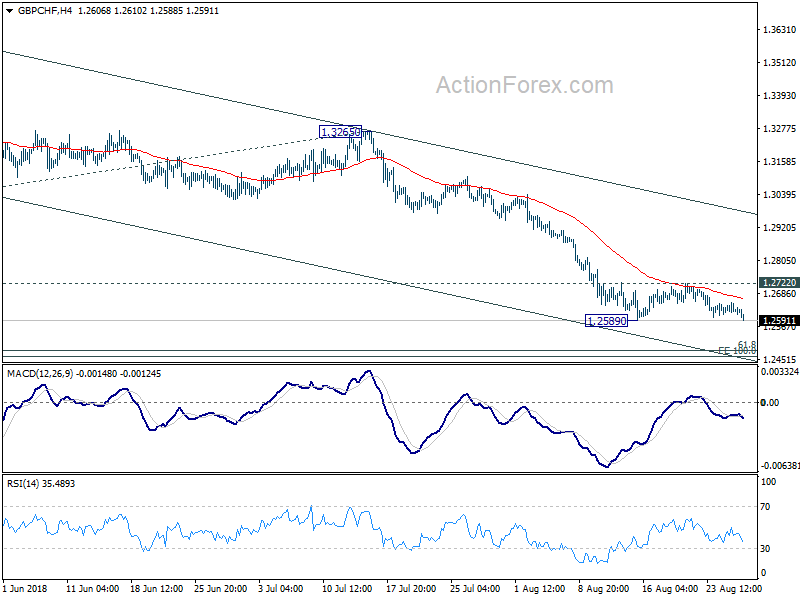

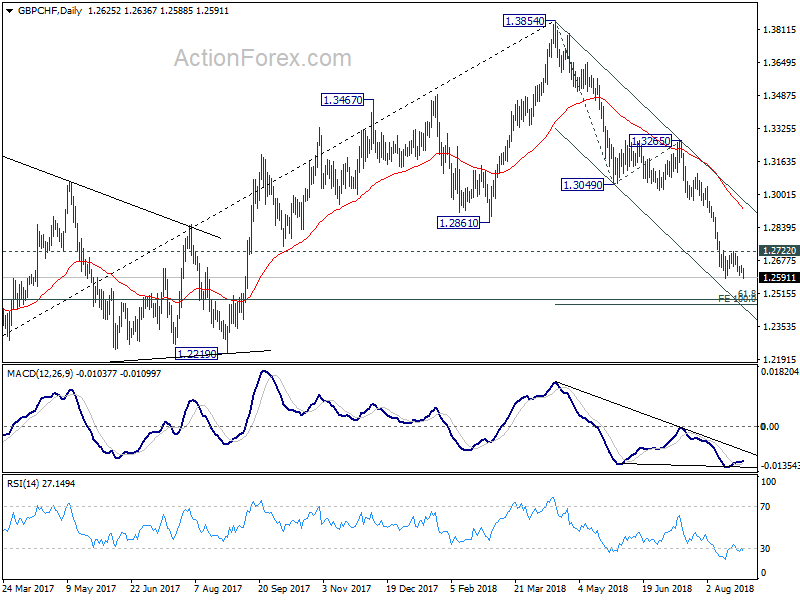

Swiss Franc overtakes Euro as the strongest currency for today and the week so far as buyers jump in during early part of European session. On the other hand, Sterling was left behind by others in the broad based selloff in Dollar. As a result, GBP/CHF dips notably to as low as 1.2588 so far today and is set to recent down trend. As planned in the last weekly report, we’ll now lower the stop of our GBP/CHF short (sold at 1.2971) to 1.2725, which is slightly above 1.2722 minor resistance.

Overall view is unchanged that fall from 1.3854 is in progress and should target cluster level at 100% projection of 1.3854 to 1.3049 from 1.3265 at 1.2460 and 61.8% retracement of 1.1638 to 1.3854 at 1.2485. We plan to exit our short position at 1.2500, which is slightly above this 1.2460/85 support zone. Consider that there is loss of downside momentum, as seen it daily MACD’s stay above signal line. There is no compelling reason to change this plan.

S&P raised New Zealand’s foreign and local currency government debt rating by a notch to AA+ and AAA, up from AA and AA+ respectively. The ratings are back to a level last seen in 2009. A “stable” outlook was attached to the new ratings.

“New Zealand is recovering quicker than most advanced economies after the Covid-19 pandemic and subsequent government lockdown delivered a severe economic and fiscal shock to the country,” S&P said. “While downside risks persist, such as another outbreak, we expect New Zealand’s fiscal indicators to recover during the next few years.”

“This provides us with better clarity over the extent of the pandemic’s damage to the government’s balance sheet,” it said in a statement,” it said, “We now believe that the government’s credit metrics can withstand potential damage from negative shocks to the economy, including a possible weakening of the real estate market”.

UK construction PMI dropped notably to 52.9 in August, down from 55.8 and missed expectation of 54.9.

Tim Moore, Associate Director at IHS Markit and author of the IHS Markit/CIPS Construction PMI®:

“The construction sector slipped back into a slower growth phase in August, with this summer’s catch-up effect starting to unwind after projects were delayed by adverse weather at the start of 2018.

“Civil engineering was the worst performing area of the construction sector, with output in this category falling for the first time since March amid reports citing a lack of new work on infrastructure projects. House building saw a particularly sharp slowdown since July, meaning that commercial construction was the fastest growing sub-sector in August.

“There are some encouraging takeaways from the latest survey, especially the resilient degree of new business growth in August and a strong upturn in staff recruitment. Survey respondents noted that they are confident about achieving organic growth at their businesses in the coming 12 months. The degree of optimism reported in August remained constrained by external factors, including domestic political uncertainty, stretched supply chains and shortages of suitably skilled labour.”

At last week’s policy meeting, which marked the conclusion of Japan’s extensive easing program and its first interest rate hike since 2007, BoJ board members underscored the importance of a cautious approach. The Summary of Opinions from this pivotal gathering highlighted board members’ perspectives on the delicate balance required in this new phase of monetary policy.

One member stressed the necessity of maintaining a “cautious stance”, especially in light of ending the negative interest rate policy, pointing out that “Japan’s economy is not in a state where rapid policy interest rate hikes are necessary.”

Furthermore, clarity and communication were emphasized as crucial elements in this transitional period. “It is important to clearly communicate through the use of various methods that the changes in the monetary policy framework proposed at this monetary policy meeting will not be a regime shift toward monetary tightening,” another member articulated.

The summary also conveyed concerns about the potential impact of premature expectations on Japan’s economic stability. A member warned of the risks associated with policy changes sparking speculative expectations misaligned with economic fundamentals, which could inadvertently destabilize financial conditions. Such volatility could “dampen the momentum of the virtuous cycle operating in Japan’s economy and delay the achievement of the inflation target.”

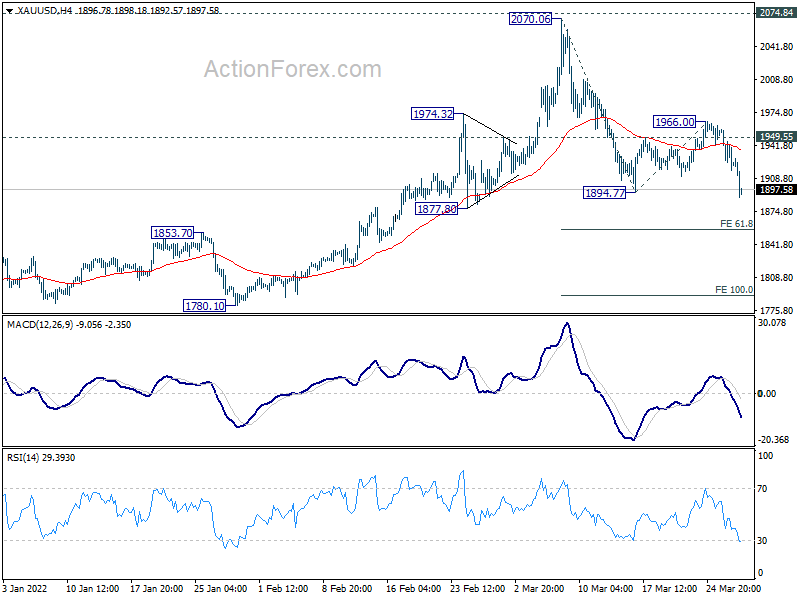

Gold dives sharply on some progress in the negotiation between Russia and Ukraine. It’s report that Ukrainian negotiators proposed a status under which it would not join alliances or host bases of foreign troops. Russia also promised to drastically scale down its military operations around Kyiv and the northern Ukrainian city of Chernihiv.

Gold’s break of 1894.77 support indicate resumption of the fall from 2070.06. Deeper decline should be seen to 61.8% projection of 2070.06 to 1894.77 from 1966.00 at 1857.67, and then 100% projection of 1790.71. Also, such fall is seen as the third leg of the correction pattern from 2074.84, and could head to 1682.60 support before completion.

BoE Deputy Governor Sarah Breeden indicated in a speech growing confidence that further tightening of rates might not be necessary. She noted a pivotal shift in focus towards “how long rates need to remain at their current level.”

Breeden underscored the importance of upcoming pay settlements and corporate responses to rising costs as key determinants of her stance on rate cuts. With pay growth currently running “several percentage points higher than what is consistent with the inflation target were they to persist,” the pathway to aligning underlying inflation with the target hinges on “some combination of a further moderation in labor cost growth and firms’ margins will be needed.”

She noted some encouragement from other economies’ advanced progress in managing inflationary pressures but emphasized the need for “further evidence” before applying similar optimism to the UK’s situation.

The upcoming months are set to play a crucial role in shaping Breeden’s evaluation of wage and price persistence, with a significant portion of the year’s wage negotiations expected to “conclude by April”. This period will be “incredibly important for my assessment,” she remarked, indicating the critical nature of this timeframe in determining the future direction of BoE’s monetary policy.

WHO spokesman Christian Lindmeier said in Geneva that Director-General Tedros Adhanom Ghebreyesus met Chinese President Xi Jinping in Beijing. Both have discussed ways to protect people in areas affected by the coronavirus. Also, they talked about “possible alternatives” to evacuations by other countries.

Lindmeier added that the Emergency Committee is being “kept in the loop” on the coronavirus outbreak. At this point, WHO hasn’t seen onward human-to-human spread of the virus outside China. He said it’s “good news but of course this could change”.

China’s Xi was quoted by state media, saying: “The virus is a devil and we cannot let the devil hide,” state television quoted Xi as saying. China will strengthen international cooperation and welcomes the WHO participation in virus prevention … We believe that the WHO and international community will give a calm, objective and rational assessment of the virus and China is confident of winning the battle against the virus.”

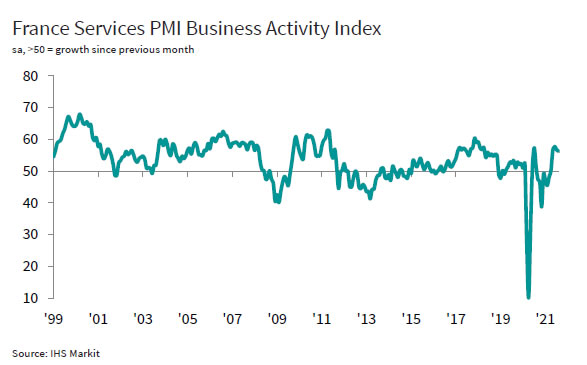

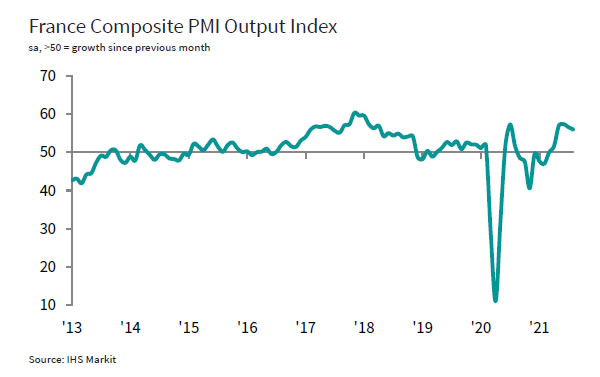

France PMI Services was finalized at 56.3 in August, just slightly down from July’s 56.8. PMI Composite was finalized at 55.9, slightly down from June’s 56.6 Markit said business activity increased at slowest rate in four months. Employment growth, on the other hand, was at strongest since October 2018. Also, cost inflation was at sharpest rate for over a decade.

Joe Hayes, Senior Economist at IHS Markit said: “The economic recovery in France continued to move along at a solid clip during August. The narrative is essentially unchanged – we’re still seeing strong demand, and firms are adjusting their workforces to accommodate growing order books. The rate of jobs growth was at its best in almost three years in August. There’s still ample work-in-hand however, so there’s clearly scope for further expansions in employment and business activity.

“Business confidence is also proving to be resilient, despite the emergence of the delta variant and steep cost pressures across the economy. Whether the recovery in business activity can push on unchecked amid these risks remains to be seen.

“Nevertheless, based on July and August survey data, France looks set for another solid GDP growth number in the third quarter.”

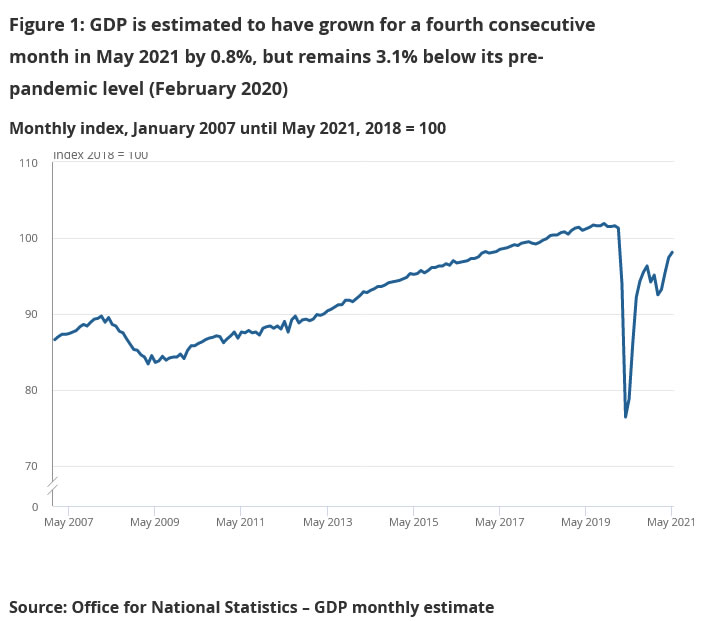

UK GDP grew 0.8% mom in May, well below expectation of 1.9% mom. That’s still the fourth consecutive month of growth. Service sector grew 0.9% mom. Production grew 0.8% mom, returned to growth. Manufacturing contracted -0.1% mom. Construction contracted for a second consecutive month, by -0.8% mom.

Overall GDP was still -3.1% below pre-pandemic level seen in February 2020. Services was -3.4% low, production -2.6% lower, while manufacturing was -3.0% lower. But construction was 0.3% above the pre-pandemic level.

Japan headline CPI (all items) rose from 1.2% yoy to 2.5% yoy in April. CPI core (ex-fresh food) rose from 0.8% yoy to 2.1% yoy. CPI core-core (ex-fresh food, energy) rose from -0.7% yoy to 0.8% yoy.

The 2.1% CPI core reading was slightly above expectation of 2.0% yoy. It topped BoJ’s 2% target for the firs time since March 2015. Also, it should be noted that CPI core-core was positive for the first time since July 2020.

EUR/USD downside breakout after Fed rate hike

EUR/USD finally breaks out to the downside after Fed hikes 75bps and projects interest rate to hit 4.4% by year end. For the near term, EUR/USD’s next target is 100% projection of 1.0368 to 0.9863 from 1.0197 at 0.9692, and then 161.8% projection at 0.9380.

For the medium term, next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694.

In any case, break of 1.0049 minor resistance is needed to indicate short term bottoming. Or, outlook will stay bearish even in case of recovery.