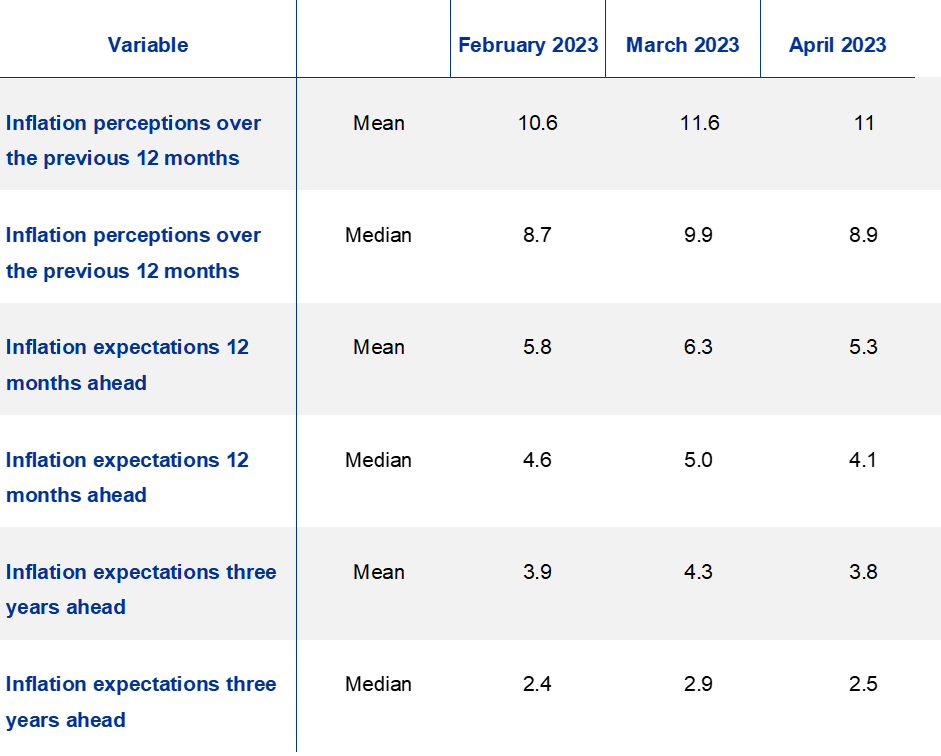

According to the latest Consumer Expectations Survey conducted by ECB in April, consumer inflation expectations have taken a significant downturn, reversing most of the gains made in the previous month.

The survey revealed that mean inflation expectations for the coming 12 months dropped from 6.3% to 5.3%. Median inflation expectations for the same period also saw a decline, dropping from 5.0% to 4.1%. These results mark a decrease even below February readings, which were at 5.8% and 4.6% respectively.

Looking further ahead, mean inflation expectations for three years in the future also slid down from 4.3% to 3.8%. Similarly, median expectations for this timeline dropped from 2.9% to 2.5%.

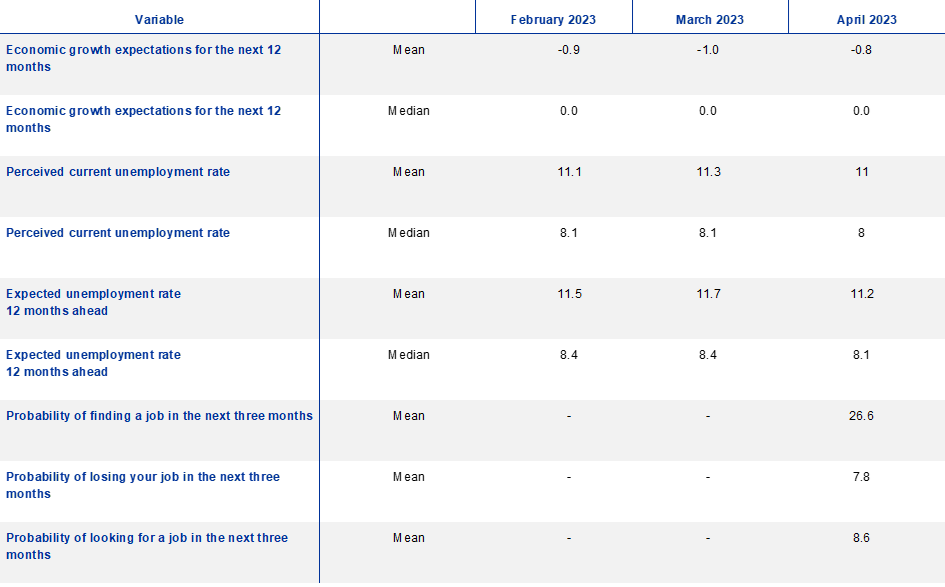

However, consumer sentiment regarding economic growth over the next 12 months displayed less negativity. The mean expectations for economic growth in the next year edged up from -1.0% to -0.8%. Meanwhile, median growth expectations remained static at 0.0% for the next 12 months.

Canada employment grew 104k in Dec, unemployment rate down to 5%

Canada employment grew strongly by 104k in December, well above expectation of 5.5k. Total employment also surpassed prior peak in May.

Unemployment rate dropped from 5.1% to 5.0%, below expectation of 5.2%, just above record low of 4.9% reached in June and July. Participation rate rose 0.2% to 65.0%.

Full release here.