Eurozone Economic Sentiment Indicator rose to 119.0 in July, up from 11.79, above expectation of 118.8. That’s the highest level on record since 1985. Employment Expectations Indicator was flat at 111.7, well above pre-pandemic level.

Looking at some more details, Eurozone industrial confidence rose from 12.8 to 14.6, eighth straight month of improvement and an all-time high. Services confidence rose from 17.9 to 19.3, highest since 2007. Consumer confidence dropped from -3.3 to -4.4. Retail trade confidence dropped from 4.7 to 4.6. Construction confidence dropped from 5.2 to 4.0.

EU ESI rose 0.9 pts to 118.0. EEI was unchanged at 111.6. Amongst the largest EU economies, the ESI rose sharply in France (+4.0) and, to a lesser extent, in Italy (+1.7) and Spain (+1.7). Sentiment in Germany (+0.3) and the Netherlands (-0.3) stayed virtually unchanged, while it deteriorated mildly in Poland (-0.7).

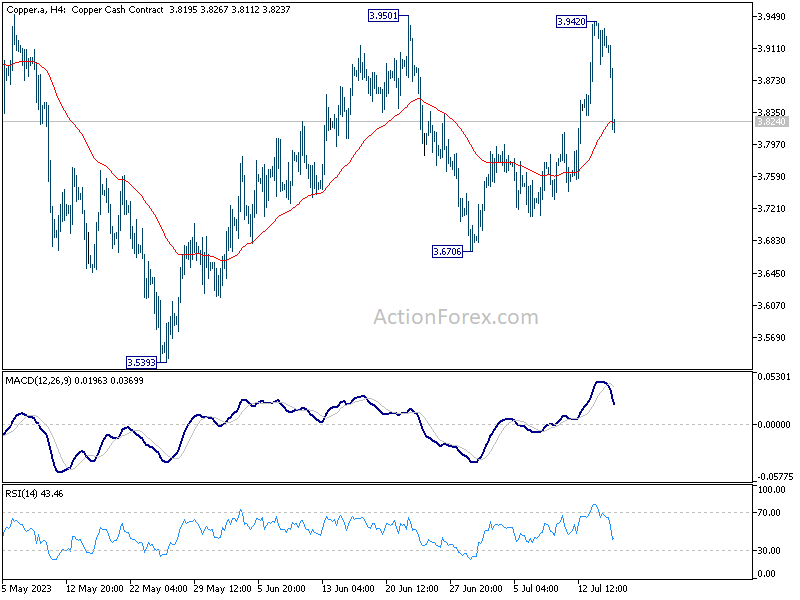

The release of disappointing Chinese economic data earlier today has cast a shadow on global sentiment, instigating downturns in oil and copper prices, as well as European indices and US futures.

WTI crude oil experienced a fleeting rebound following a Reuters news alert suggesting that Saudi Arabia was extending voluntary output cut. However, the news alert was withdrawn shortly after, as it merely echoed an earlier report from June 4. Now, WTI prices are being pressured lower amid concerns over domestic demand in China and the partial restart of Libyan production that had been previously halted.

Technically, near term bias is neutral in WTI after a top was formed at 77.22, ahead of 100% projection of 63.37 to 74.74 from 66.94 at 78.1. While the stay above 55 D EMA is a near term bullish sign, i cannot be ruled out that rebound from 63.37 is merely a corrective bounce. Break of 72.57 support will argue that the rebound have completed and target 63.67 and possibly below. Nevertheless, firm break of 78.01 will add another evidence for trend reversal and target 83.46.

Copper, a commodity particularly sensitive to Chinese data, also felt the pinch. Rejection by 3.9501 resistance keep near term outlook neutral for now. While prior break of 55 D EMA is a bullish sign, upside is capped below falling trend line resistance (from 4.3556). On the upside, break of 3.9501 will resume the rebound from 3.5393 and argues that whole fall form 4.3556 has finished. However, break of 3.6706 would indicate that fall from 4.3556 is ready to resume through 3.5395.

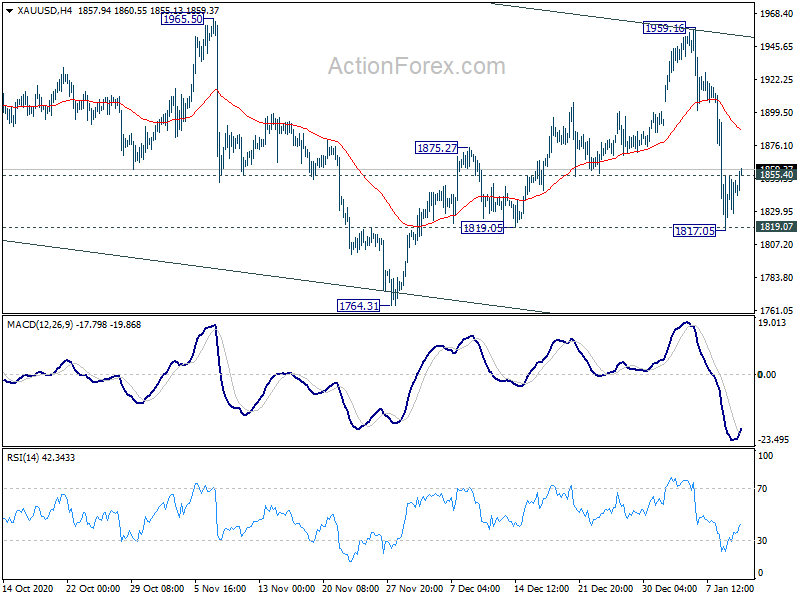

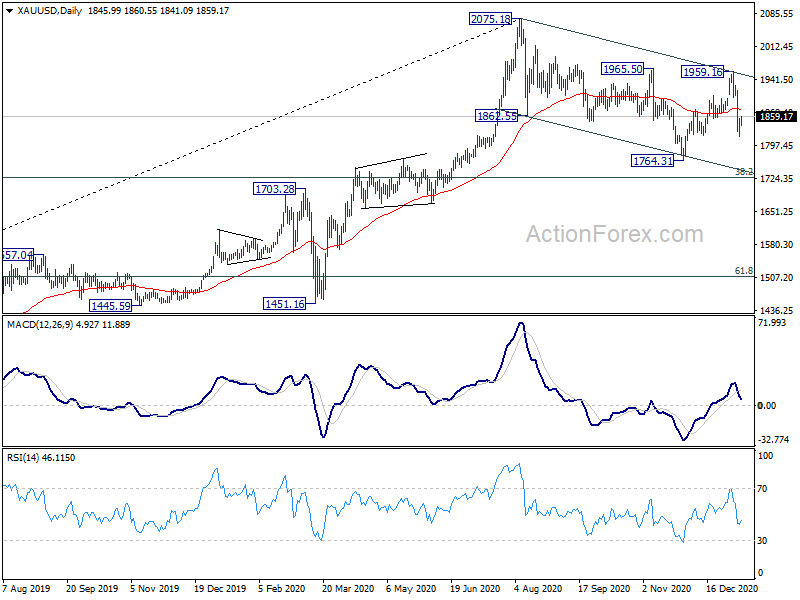

Gold’s break of 1855.40 minor resistance suggests temporary bottoming at 1817.05, after drawing support from 1819.07 support. Some consolidations could be seen, with risk of stronger recovery. But upside should be limited by 4 hour 55 EMA (now at 1888.09) to bring fall resumption.

We’re holding on to the view that fall from 1959.16 is the third leg of the corrective pattern from 2075.18. Break of 1817.05 will target 1764.31 support and below.

The Financial Times reported that EU is floating around a compromised Irish border backstop proposal to solve the ongoing Brexit negotiation impasse. The proposal was briefed to EU ambassadors earlier on Wednesday.

Under the proposal, EU would lay out the full terms of a “bare-bones” whole-UK customs union in the withdrawal agreement. It would apply a common external tariff on imports from outside the EU and rules of original. Meanwhile, under the backstop, Northern Ireland would remain in a deep customs union with the EU, applying all “customs code” and following EU’s regulations for goods and agri-food products. The stop-gap measures would remain in place until concluding the permanent UK-EU trade deal.

UK Prime Minister Theresa May is expected to tell the EU whether UK is open to the compromise next week. And that would be a key factor to determine if a November Brexit summit is to be held.

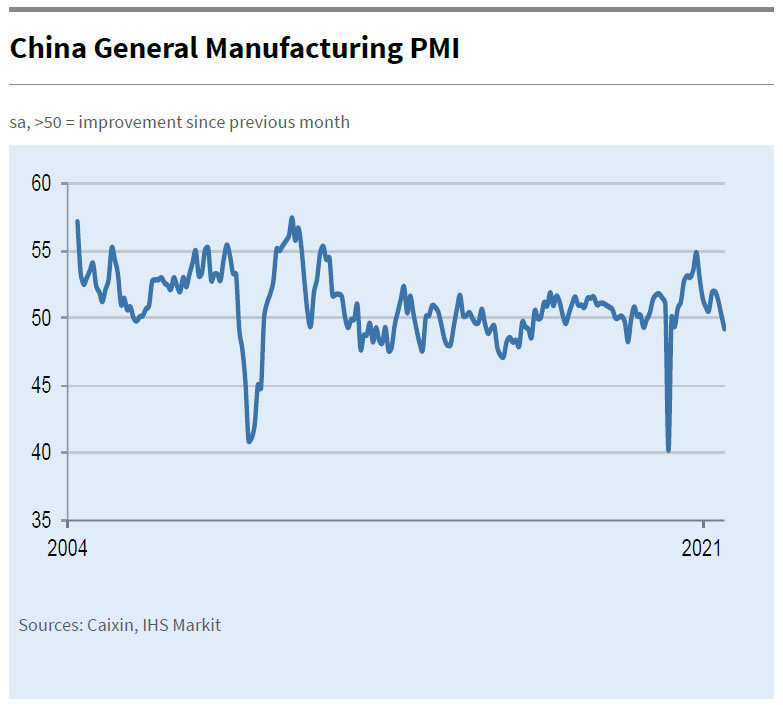

China Caixin PMI Manufacturing dropped to 49.2 in August, down from 50.3, below expectation of 50.2. That’s the first contraction reading since April 2020. Caixin said output and new orders both declined modestly. Supply chain delays worsened amid uptick on COVID-19 cases. Companies trimmed purchasing activity and stagging levels.

Wang Zhe, Senior Economist at Caixin Insight Group said: “The latest Covid-19 resurgence has posed a severe challenge to the economic normalization that began in the second quarter of last year… Official economic indicators for July were worse than the market expected, indicating mounting downward pressure on economic growth. Authorities need to take a holistic view and balance containing Covid-19, stabilizing the job market, and maintaining stability in supply and prices.”

UK reiterated that it “will not extend the transition period”. That still “leaves a limited but sufficient” time to reach an agreement. After an “appropriate number of negotiating rounds” between now and June, UK would hope that “the broad outline of an agreement would be clear and be capable of being rapidly finalised by September”.

However, “if that does not seem to be the case at the June meeting, the Government will need to decide whether the UK’s attention should move away from negotiations and focus solely on continuing domestic preparations to exit the transition period in an orderly fashion.”

Cabinet office minister Michael Gove told parliament that “a the end of the transition period on the 31st of December, the United Kingdom will fully recover its economic and political independence. We want the best possible trading relationship with the EU, but in pursuit of a deal we will not trade away our sovereignty.”

At a Fed conference overnight, Dallas Fed President Lorie Logan said that inflation appears to be “trending toward 3%”, a figure still above the 2% target.

Despite a cooling labor market, Logan highlighted that it remains “too tight,” implying that the job market’s strength could continue to put upward pressure on wages and, consequently, inflation.

Logan emphasized the need “see tight financial conditions in order to bring inflation to 2% in a timely and sustainable way”. She will be looking at “data” and “financial conditions” as the next meeting in December approaches.

With a particular focus on recent retracement in 10-year Treasury yield and broader financial conditions, Logan suggests these elements will play a pivotal role in shaping Fed’s forthcoming monetary policy decisions.

RBNZ Governor Adrian Orr said in a Statement of Intent that economic activity in New Zealand is “returning to its pre-COVID-19 levels”, supported by “ongoing favourable domestic health outcomes, and improving global demand and higher prices for New Zealand’s goods and exports”.

“A catch-up in consumer spending and construction activity, supported by substantial monetary and fiscal stimulus is underpinning employment growth,” he added.

“As long as COVID-19 is contained and the global and economic recovery is sustained, eventually economic policy settings can be expected to normalize over the medium term.”

US ISM Services PMI dropped -3.4 pts to 55.3 in February, well below expectation of 58.7. Business activity/production dropped -4.4 to 55.5. New orders dropped -9.9 to 41.9. Employment also dropped -2.5 to 52.7. But prices jumped 7.6 to 71.8.

ISM said, “the past relationship between the Services PMI and the overall economy indicates that the Services PMI for February (55.3 percent) corresponds to a 2.2 -percent increase in real gross domestic product (GDP) on an annualized basis.”

BoC Governor Tiff Macklem delivered three main messages to a House of Commons Committee. First, the Canadian economy is strong… Second, inflation is too high…. Third, we need higher interest rates.”

“The economy needs higher rates and can handle them….,” he said, “We also need higher interest rates to keep Canadians’ expectations of inflation anchored on the target. We can’t control or even influence the prices of most internationally traded goods. But if Canadians’ expectations of inflation stay anchored on the 2% target, inflation in Canada will come back down when global inflationary pressures from higher oil prices and clogged supply chains abate.”

“Canadians should expect interest rates to continue to rise toward more normal settings. By more normal we mean within the range we consider for a neutral rate of interest that neither stimulates nor weighs on the economy. We estimate this rate to be between 2% and 3%,” he added.

Good morning. I’m pleased to be here with you to discuss today’s policy announcement and the Bank of Canada’s Monetary Policy Report (MPR). I am especially pleased to have Senior Deputy Governor Carolyn Rogers here for her first press conference. She has joined the Governing Council at an important time.

Our message today is threefold.

First, the emergency monetary measures needed to support the economy through the pandemic are no longer required and they have ended.

Second, interest rates will need to increase to control inflation. Canadians should expect a rising path for interest rates.

Third, while reopening our economy after repeated waves of the COVID-19 pandemic is complicated, Canadians can be confident that the Bank of Canada will control inflation. We are committed to bringing inflation back to target.

Let me take each of these in turn.

The Bank’s response to the pandemic has been forceful. Throughout, our actions have been guided by our mandate. We have been resolute and deliberate, communicating clearly with Canadians on our extraordinary measures to support the economy and on the conditions for their exit. When we introduced emergency liquidity measures to support core funding markets, we said they would end when market functioning was restored. And they did. When we launched quantitative easing (QE), we said it would continue until the recovery was well underway. As the recovery progressed, we began tapering QE and ended it in October. Today marks the final step in exiting from emergency policies. We said exceptional forward guidance would continue until economic slack was absorbed. With the strength of the recovery through the second half of 2021, the Governing Council now judges this condition has been met. As such, we are removing our commitment to hold our policy rate at its floor of 0.25%.

Second, we want to clearly signal that we expect interest rates will need to increase. A lot of factors are contributing to the uncomfortably high inflation we are experiencing today, and many of them are global and reflect the unique circumstances of the pandemic. As the pandemic fades, conditions will normalize, and inflation will come down. However, with Canadian labour markets tightening and evidence of capacity pressures increasing, the Governing Council expects higher interest rates will be needed to bring inflation back to the 2% target.

Finally, Canadians can be assured that the Bank of Canada will control inflation. Prices for many goods and services are rising quickly, and this is making it harder for Canadians to make ends meet—particularly those with low incomes. Prices for food, gasoline and housing have all risen faster than usual. We expect inflation will remain close to 5% through the first half of 2022 and then move lower. There is some uncertainty about how quickly inflation will come down because we’ve never experienced a pandemic like this before. But Canadians can be assured that we will use our monetary policy tools to control inflation.

Let me turn to the economic outlook that we’ve outlined in our MPR.

Globally, the pandemic recovery is strong but uneven and continues to be marked by supply chain disruptions. Robust demand for goods combined with these supply problems and higher energy prices have pushed up global inflation. With this rise in inflation, expectations that monetary stimulus will be reduced have been pulled forward and financial conditions have tightened from very accommodative levels.

In Canada, growth in the second half of 2021 was even stronger than we had projected, and a wide range of measures now suggest economic slack is absorbed. With the rapid spread of the Omicron variant, first-quarter growth is likely to be modest, but we expect the impact on our economy to be less severe than previous waves. We forecast annual growth in economic activity will be 4% this year and about 3½% in 2023 as consumer spending on services rebounds and business investment and exports show solid growth.

CPI inflation is currently well above our target range and core measures have edged up. Global supply chain disruptions, weather-related increases in agricultural prices and high energy prices have put upward pressure on inflation in Canada, and that is expected to continue in the months ahead. These pressures should ease in the second half of 2022, and inflation should decline relatively quickly to around 3% by year end. Further out, we expect demand will moderate and supply will increase as productivity improves. This will ease price pressures and bring inflation gradually back close to the 2% target over 2023 and 2024.

Let me now say a few words about the Governing Council’s deliberations.

Of course, we discussed the impact of Omicron. Renewed restrictions and household caution about this highly infectious variant have temporarily slowed economic activity. Once again, high-contact services sectors have been hardest hit. But with many more Canadians getting infected in this wave, worker absences have been more widespread. Our high rates of vaccination and adaptability to restrictions should limit the downside economic risks of this wave.

The Governing Council also spent considerable time assessing the overall balance of demand and supply in the economy. In October, we projected the output gap would close sometime in the middle quarters of this year. While measuring the output gap is always uncertain and pandemic-related distortions make assessing supply more complicated, a broad range of indicators clearly suggest economic slack has been absorbed more quickly than expected. Employment is above pre-pandemic levels, businesses are having a hard time filling job openings, and wage increases are picking up. Unevenness across sectors remains, but taking all the evidence together, the Governing Council judges the economy is now operating close to its capacity.

We debated the most likely path for inflation. The resolution of global supply bottlenecks has important implications for inflation in Canada. There is some evidence that supply disruptions may have peaked, but the spread of Omicron is a new wildcard that could further disrupt global supply chains. We also considered the potential for some reversal of the large price increases for goods. This would pull inflation down more quickly than we forecast. Overall, we judged the risks around our inflation projection are reasonably balanced.

We also assessed more domestic sources of inflationary pressures. While global goods price inflation is expected to ease, the tightness in Canadian labour markets, rising house prices and evident capacity pressures suggest that if demand continues to grow faster than supply this will put upward pressure on inflation.

We noted that measures of inflation expectations are broadly in line with our own forecast, with longer-term expectations remaining well anchored on the 2% target. We agreed it is paramount to ensure that higher near-term inflation expectations don’t migrate into higher long-term expectations and become embedded in ongoing inflation.

Putting all this together, we concluded that, consistent with our forecast, a rising path for interest rates will be required to moderate spending growth and bring inflation back to target.

Of course, we discussed when to begin increasing our policy interest rate. Our approach to monetary policy throughout the pandemic has been deliberate, and we were mindful that the rapid spread of Omicron will dampen spending in the first quarter. So we decided to keep our policy rate unchanged today, remove our commitment to hold it at its floor, and signal that rates can be expected to increase going forward. As we indicated in our press release this morning, the timing and pace of those increases will be guided by the Bank’s commitment to achieving the 2% inflation target.

We take our communication with Canadians very seriously. For almost two years now we have told Canadians we would keep our policy rate pinned at its floor until economic slack is absorbed. With slack absorbed more quickly than expected, it is time to remove our extraordinary forward guidance. This ends our emergency policy setting and signals that interest rates will now be on a rising path. This is a significant shift in monetary policy, and we judged that it is appropriate to move forward in a deliberate series of steps.

Let me say a final word about another important monetary policy tool—our balance sheet. The Bank will keep the holdings of Government of Canada bonds on our balance sheet roughly constant at least until we begin to raise the policy interest rate. At that time, we will consider exiting the reinvestment phase and reducing the size of our balance sheet by allowing maturing Government of Canada bonds to roll off. As we have done in the past, before implementing changes to our balance sheet management, we will provide more information on our plans.

With that, Senior Deputy Governor Rogers and I will be happy to take your questions.

BoC Governor Tiff Macklem, during a parliamentary committee hearing, spoke on the progress made in curbing inflation. He stated, “Inflation is coming down quickly—data this morning show it fell to 4.3% in March. And we forecast it to be around 3% this summer.”

He emphasized the need for inflation expectations, services price inflation, wage growth, and corporate pricing behavior to normalize before inflation can reach the 2% target. He warned, “if monetary policy is not restrictive enough to get us all the way back to the 2% target, we are prepared to raise the policy rate further to get there.”

Macklem, expects inflation to return to 2% by the end of 2024 and noted that Canadian GDP growth would be weak for the rest of this year, gradually picking up in 2024 and through 2025.

He identified the biggest upside risk as the stickiness of services price inflation and the key downside risk as a global recession. While acknowledging that the risks around the inflation forecast are roughly balanced, he noted, “with inflation still well above our target, we continue to be more concerned about the upside risks.”

No surprise from Fed. Below is the full statement.

Federal Reserve issues FOMC statement

Information received since the Federal Open Market Committee met in June indicates that the labor market has continued to strengthen and that economic activity has been rising at a strong rate. Job gains have been strong, on average, in recent months, and the unemployment rate has stayed low. Household spending and business fixed investment have grown strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1-3/4 to 2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the FOMC monetary policy action were: Jerome H. Powell, Chairman; John C. Williams, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Esther L. George; Loretta J. Mester; and Randal K. Quarles.

US durable goods orders rose 0.5% mom to USD 256.3B in March, well below expectation of 2.5% mom. Ex transport orders,however, rose 1.6% mom , matched expectations. Ex-defense orders rose 0.5% mom. Fabricated metal products, up six of the last seven months, led the increase, 3.6% mom to USD 35.4B.

BoE Chief Economist Huw Pill told BloombergTV that in yesterday policy decision statement, ” the word ‘forcefully’ – which clearly is the word the market is focused on, you focused on, and has a meaning – it’s also important to see that that was put in the context of ‘if necessary we will act forcefully’, and so there’s a conditionality there.”

“If we do see greater evidence that the current high level of inflation is becoming embedded in pricing behavior by firms, in wage setting behavior by firms and workers, then that will be the trigger for this more aggressive action,” he added.

But he also indicated that the statement had “a certain level of flexibility because it had to encompass those different views… we were trying to emphasise is that that flexibility also applies to what the decisions are. I don’t think it’s all about August. We talked about the pace, timing and scale of future decisions.”

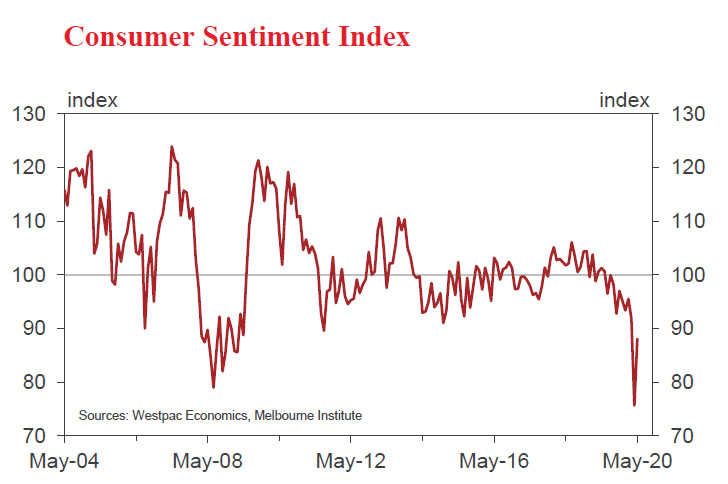

Australia Westpac consumer sentiment rebounded notably by 16.4% to 88.1 in May, up from 75.6. That’s also the biggest gain since record began nearly fifty years ago, reversing much of April’s -17.7% decline. However, the index is still “relatively weak by historical standard”, being the second lowest reading since global financial crisis and “firmly in pessimistic territory”.

Looking at some big movers, the “economy, next 12 months” sub-index jumped 32.6% to 71.2, up from 53.7. The prospect of earlier than expected reopening has “soothed some of the worst fears”, even though consumers still do not expect a return to growth any time soon. The “time to buy a major item” sub-index surged 26.7% to 96.6, up from 76.2. Retailers can expect more “foot traffic” as restrictions ease.

Westpac also noted that today’s results “provide genuine reason for optimism that the Australian economy can surprise forecasters on the upside in these highly uncertain times.”.

Also from Australia, wage price index rose 0.5% qoq in Q1, matched expectations.

RBA Governor Philip Lowe said in a speech that the key to a return to more normal interest rates globally is to improve the “investment climate”. There are two central elements to do so. First is “reduction in some of the geopolitical and other concerns”. Second is “structural measures” that boost people’s “confidence about future economic growth”.

Domestically, Lowe said this year’s three interest rate cuts as “helping” the Australian economy and supporting the “gentle turning point” in growth. RBA is “prepared to ease” further if needed. But he emphasized it is “extraordinarily unlikely that we will see negative interest rates in Australia”. Though, it’s likely that “an extended period of low interest rates” is required.

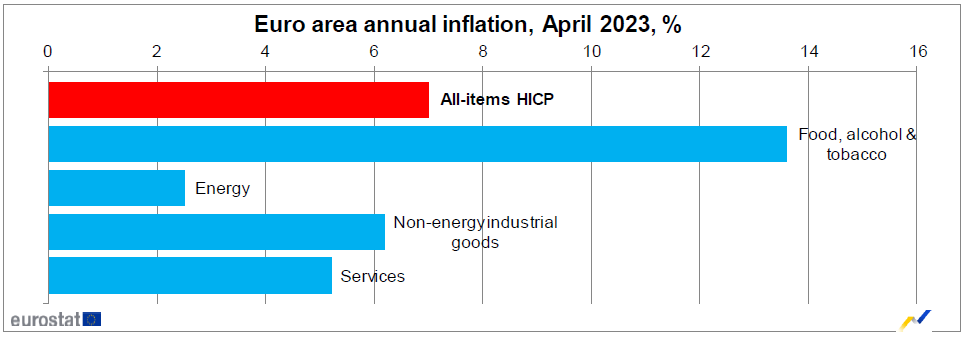

Eurozone CPI accelerated from 6.9% yoy to 7.0% yoy in April, above expectation of 6.9% yoy. CPI core (all item excluding energy, food, alcohol & tobacco) slowed from 5.7% yoy to 5.6% yoy, below expectation of 5.7% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in April (13.6%, compared with 15.5% in March), followed by non-energy industrial goods (6.2%, compared with 6.6% in March), services (5.2%, compared with 5.1% in March) and energy (2.5%, compared with -0.9% in March).

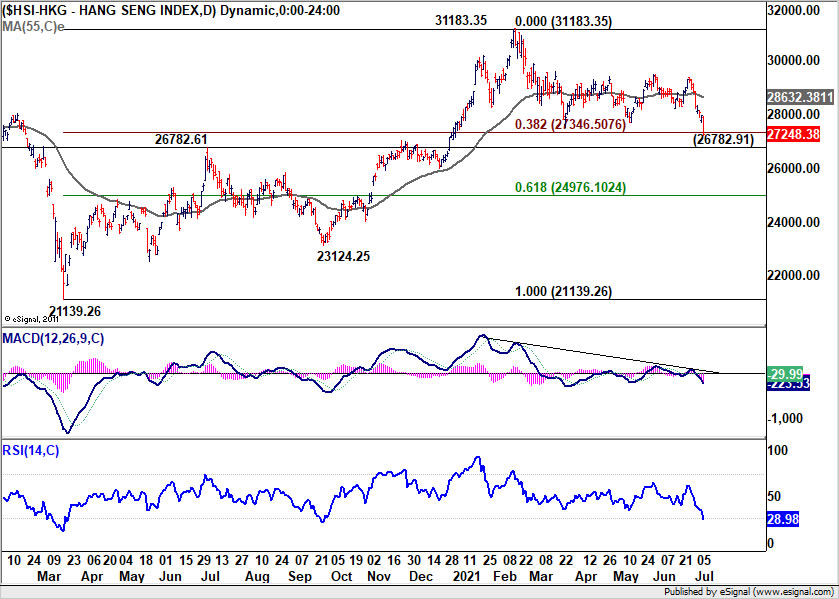

While US stocks were strong, Asian markets are trading notably lower today, as led by the free fall in Hong Kong. Selloff in Chinese tech stocks intensified after the Chinese government announced a step up in oversight on Chinese stocks listing in the US. The announcement came just after the surprised crackdown on ride-hailing giant Didi, days after it’s mega IPO last week.

At the time of writing, HSI is down -2.5%. Considering the downside momentum, the break of 38.2.% retracement of 21139.26 to 31183.35 at 27346.50 is starting to make outlook bearish. Focus is now on 26782.61 resistance turned support. Sustained break there will suggest that whole rise from 21139.26 has completed at 31183.35 in a corrective three-wave structure. That would at least open up a bearish case for 61.8% retracement at 24976.10 and below.

EU leaders agreed overnight to close the external borders for 30 days to slow the spread of coronavirus pandemic. All non-EU citizens are not allowed to enter EU. But movements within EU are allowed. Also, the restrictions do not apply to medical staff nor goods. The restrictions will take effect as soon as individual governments take the necessary internal measure.

“The enemy is the virus and now we have to do our utmost to protect our people and to protect our economies,” European Commission President Ursula von der Leyen said. “We are ready to do everything that is required. We will not hesitate to take additional measures as the situation evolves.”

European Council President Charles Michel pledge that “the union and its member states will do whatever it takes”, and EU will arrange for the repatriation of citizens of member countries.

Eurozone economic sentiment rose to record 119.0, strong industrial and services confidence

Eurozone Economic Sentiment Indicator rose to 119.0 in July, up from 11.79, above expectation of 118.8. That’s the highest level on record since 1985. Employment Expectations Indicator was flat at 111.7, well above pre-pandemic level.

Looking at some more details, Eurozone industrial confidence rose from 12.8 to 14.6, eighth straight month of improvement and an all-time high. Services confidence rose from 17.9 to 19.3, highest since 2007. Consumer confidence dropped from -3.3 to -4.4. Retail trade confidence dropped from 4.7 to 4.6. Construction confidence dropped from 5.2 to 4.0.

EU ESI rose 0.9 pts to 118.0. EEI was unchanged at 111.6. Amongst the largest EU economies, the ESI rose sharply in France (+4.0) and, to a lesser extent, in Italy (+1.7) and Spain (+1.7). Sentiment in Germany (+0.3) and the Netherlands (-0.3) stayed virtually unchanged, while it deteriorated mildly in Poland (-0.7).

Full release here.