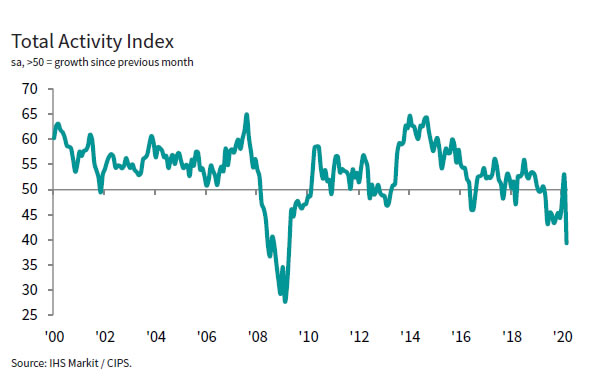

UK PMI manufacturing rose to 53.8 in September, up from 53.0 and matched expectations. Keying findings showed “output and new order growth both accelerate”, “input cost and output charge inflation strengthen”.

Rob Dobson, Director at IHS Markit, which compiles the survey:

“September saw a mild improvement in the performance of the UK manufacturing sector. Domestic market demand strengthened, while increased orders from North America and Europe helped new export business stage a modest recovery from August’s contraction. Business confidence also rose to a three month high.

“Despite these causes for short-term optimism, conditions in manufacturing are still relatively lacklustre overall. Based on its historical relationship with official ONS data, the latest survey is consistent with output expanding at only a moderate pace. Although total exports rose, exports of goods used as inputs by other manufacturers fell for the third straight month, ending the worst quarter for over three years for such exporters, suggesting that foreign companies may be sourcing less from UK-based component suppliers.

“Many UK manufacturers also noted that the backdrop of Brexit and a volatile exchange rate were making any forecasting activity increasingly difficult, with uncertainty adding to reluctance to hire. Headcounts fell at larger companies for a second successive month.

“On the price front, both output charges and input costs rose at faster rates in September, which may exert further upward pressure on consumer prices in future.”

Full release here.

Also from UK, mortgage approvals rose to 66k in August. M4 money supply rose 0.2% mom in August.

Bundesbank: German economy to remain subdued at least in H1

In its monthly report, Bundesbank warned that German economy will continue to struggle in the first half of 2019. The economy is unlikely to regain momentum with Weak orders in manufacturing, gloomy sentiment indicators and sluggish investments. It said that “all these suggest that the underlying pace of the economy should remain subdued at least in the first half of the year.”

Though, it also noted that “there are no signs that the slowdown is becoming an outright downturn.” In particular, the drag from auto exports is starting to normalize. Meanwhile, labor market remains healthy with private consumption picking up.

Full report here.