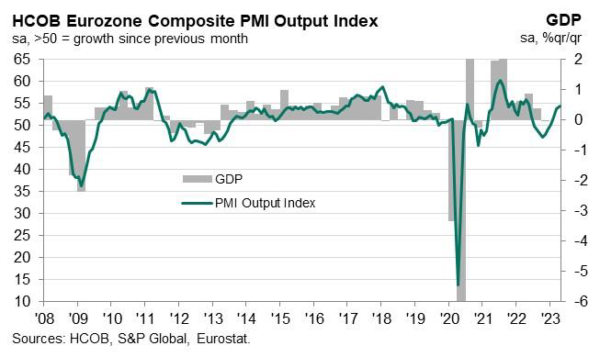

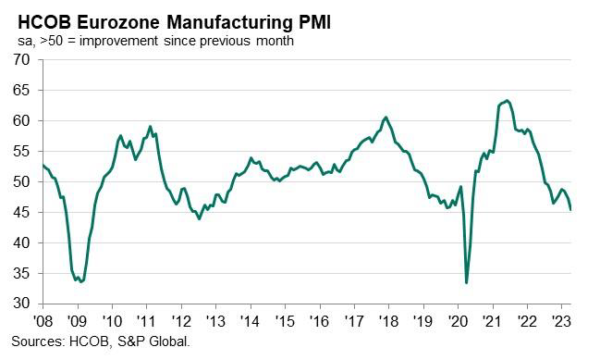

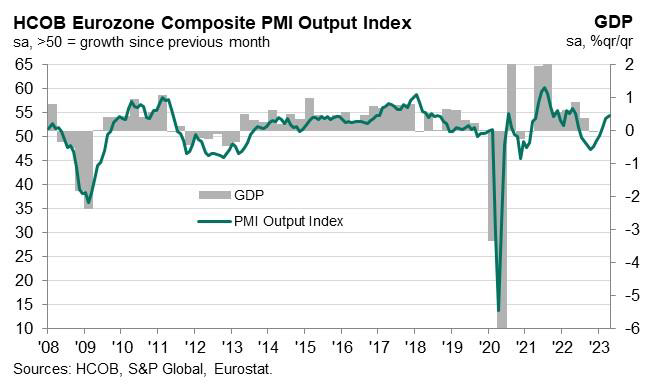

Eurozone PMI Manufacturing declined from 47.3 to 45.5 in April, hitting a 35-month low. On the other hand, PMI Services rose from 55.0 to 56.6, a 12-month high. PMI Composite rose from 53.7 to 54.4, an 11-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said: “The HCOB Purchasing Managers’ Indices for the euro zone show a very friendly overall picture of an economy that continues to recover. However, a closer look reveals that growth is very unevenly distributed…”

“For the further, companies are rather positive not only in the services sector but also for the manufacturing sector. According to the companies surveyed, the reasons for this optimism include a diminishing fear of a resurgence of the energy crisis, supply chains that are functioning better again, and the expectation that inflation has passed its zenith. The latter is coupled with the hope that the ECB will pause its interest rate hikes soon.”

Full Eurozone PMI release here.

Also released, Germany PMI Manufacturing fell from 44.7 to 44.0, a 35-month low. PMI Services rose from 53.7 to 55.7, a 12-month high. PMI Composite rose from 52.6 to 53.9, a 12-month high.

France PMI Manufacturing dropped from 47.3 to 45.5, a 35-month low. PMI Services rose from 53.9 to 56.3, an 11-month high. PMI Composite rose from 52.7 to 53.8, also an 11-month high.

Eurogroup urged Italy to comply to EU budget rules

In a statement released today, the Eurogroup said Italy’s 2019 Draft Budget Plan (DBP) was breaking EU rules and urged Italy to rectify it.

It said “The Eurogroup recalls that in its opinion issued on 23 October 2018 the Commission identified a particularly serious non-compliance with the recommendation addressed to Italy by the Council on 13 July 2018 and requested a revised DBP. Italy submitted a revised DBP on 13 November, on which the Commission issued another opinion on 21 November, confirming the existence of a particularly serious non-compliance with the Council recommendation.”

And, “we support the Commission assessment and recommend Italy to take the necessary measures to be compliant with the SGP. We also support the ongoing dialogue between the Commission and the Italian authorities.”

Also, the Eurogroup noted that five member states’ DBP are “deemed to be at risk of non-compliance with the SGP”, including Belgium, France, Portugal, Slovenia and Spain.

Eurogroup’s statement here.