Credit Suisse’s measures to ease investor concerns over potential contagion and a banking crisis have failed to lift market pressures, with the Asian markets remaining under pressure.

The bank announced it would borrow up to CHF50B from the SNB, calling it a “decisive action to pre-emptively strengthen its liquidity.” The loan and a repurchase of billions of dollars of Credit Suisse debt aim to manage its liabilities and interest payment expenses.

Earlier, in a joint statement with the Swiss financial market regulator FINMA, the SNB assured the markets that the Credit Suisse had met “strict capital and liquidity requirements” and said, “there are no indications of a direct risk of contagion for Swiss institutions due to the current turmoil in the US banking market.”

“If necessary, the SNB will provide CS with liquidity,” FINMA and SNB said.

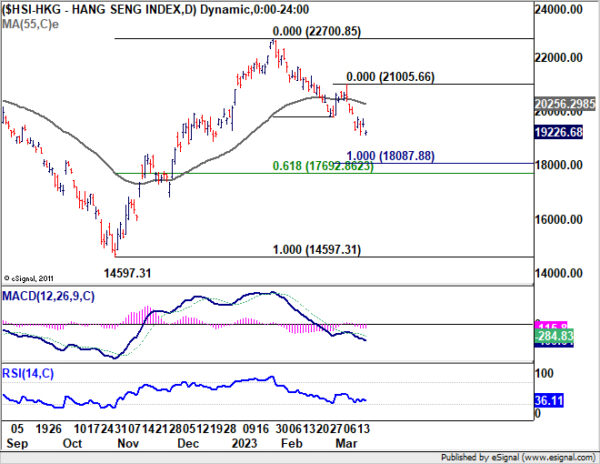

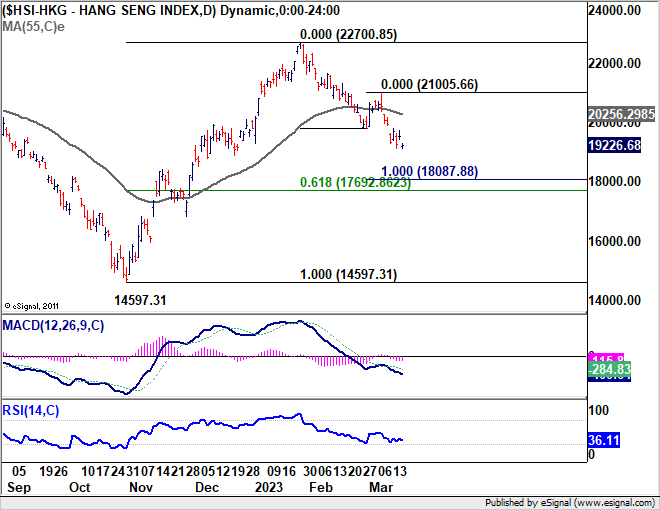

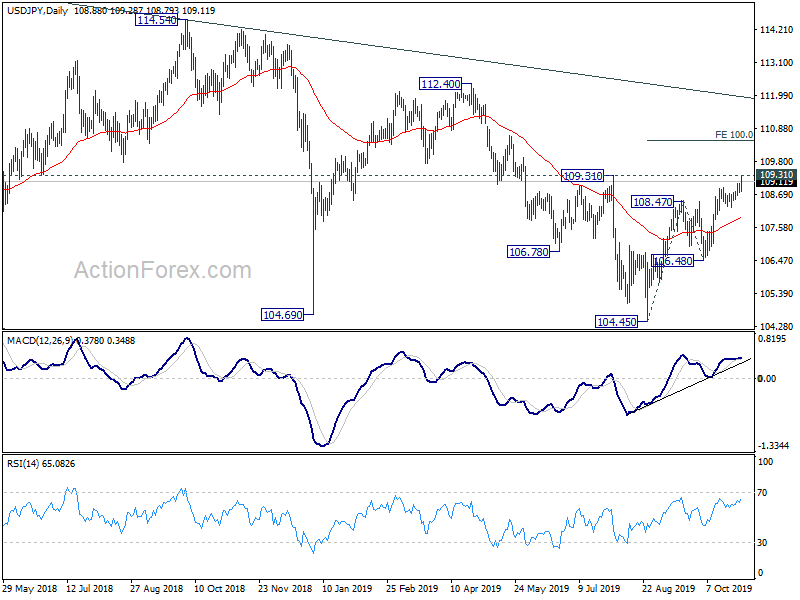

Hong Kong HSI gapped down today and is trading down -1.6% at the time of writing. From a technical perspective, the index’s decline from 22700.85 is still ongoing, and unless the 55-day EMA (now at 20256.19) is breached, a further decrease is anticipated. Even as a corrective move, this drop could aim for the 100% projection of 22700.85 to 19783.07 from 21005.66 at 18087.88.

Trump vows not to back down on tariffs, China warns of countermeasures

At a rally in Florida late Wednesday, Trump accused that China “broke the deal” as the trade negotiations entered the final stage. And he pledged no to back down on tariffs unless China “stops cheating our workers”. He said, “I just announced that we’ll increase tariffs on China and we won’t back down until China stops cheating our workers and stealing our jobs, and that’s what’s going to happen, otherwise we don’t have to do business with them”. And, ‘They broke the deal,” he added. “They can’t do that. So they’ll be paying. If we don’t make the deal, nothing wrong with taking in more than $100 billion a year.”

In response to new tariff threats, China’s Ministry of Commerce said in a statement: “Escalating the trade conflict is not in the interest of the people in both countries and the world. China deeply regrets the move. But if the US tariff measures are implemented, China will have to take necessary countermeasures.” Chinese Vice Premier will be in Washington to try to save the trade deal while new round of tariffs will take effect in less than 24 hours.