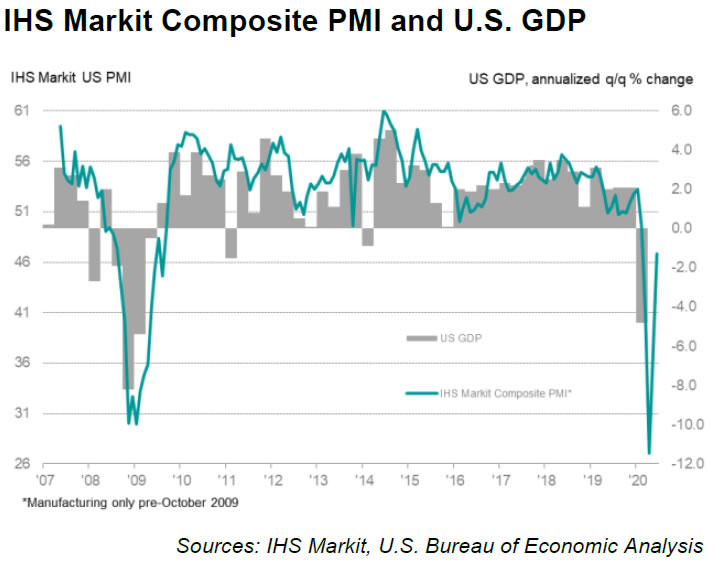

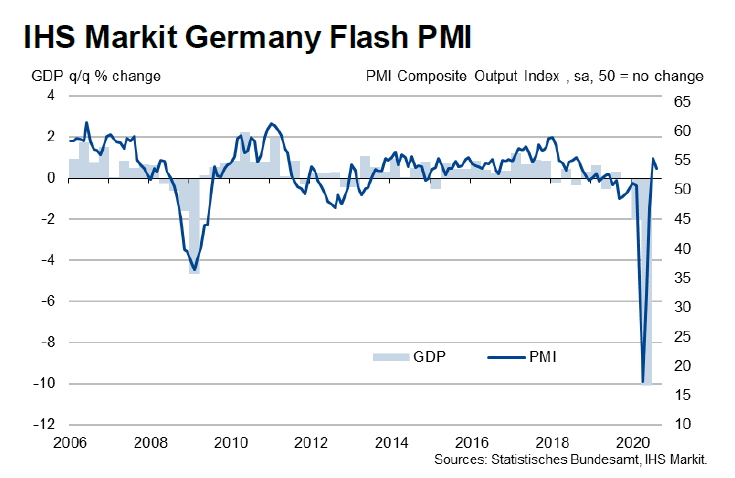

US PMI Manufacturing rose to 49.6 in June, up from 39.8, missed expectation of 50.0. PMI Services rose to 46.7, up from 37.5, missed expectation of 46.9. PMI Composite rose to 46.8, up form 37.0. All three indices are at their 4-month high.

Chris Williamson, Chief Business Economist at IHS Markit, said:

“The flash PMI data showed the US economic downturn abating markedly in June. The second quarter started with an alarming rate of collapse but output and jobs are now falling at far more modest rates in both the manufacturing and service sectors. The improvement will fuel hopes that the economy can return to growth in the third quarter.

“However, although brief, the downturn has been fiercer than anything seen previously, leaving a deep scar which will take a long time to heal. We anticipate that the US economy will contract by just over 8% in 2020. The coming months will therefore see the focus turn to just how much recovery momentum the economy can muster to recoup this lost output.

“Any return to growth will be prone to losing momentum due to persistent weak demand for many goods and services, linked in turn to ongoing social distancing, high unemployment and uncertainty about the outlook, curbing spending by businesses and households. The recovery could also be derailed by new waves of virus infections. Continual vigilance by the Fed, US Treasury and health authorities will therefore be required to keep any recovery on track.”

Germany manufacturers’ export expectations improved on Brexit and US clarity

Germany’s Ifo Export Expectations in manufacturing rose 1.9 pts to 6.0 in January, hitting the highest level since October. “Clarity on Brexit and the US presidency, a robust industrial economy, and the start of vaccination campaigns worldwide led to cautious optimism in the German export sector,” said Clemens Fuest, President of the ifo Institute.

“Manufacturers of computers and electrical equipment expect to see major increases in exports. Companies in mechanical engineering and the chemical industry are also confident about their future exports. Expectations among food and beverage manufacturers also saw a marked recovery. They currently assume their export business will hold steady. The international market is still difficult for Germany’s clothing industry. Furniture manufacturers also expect their international sales to decline.”

Full release here.