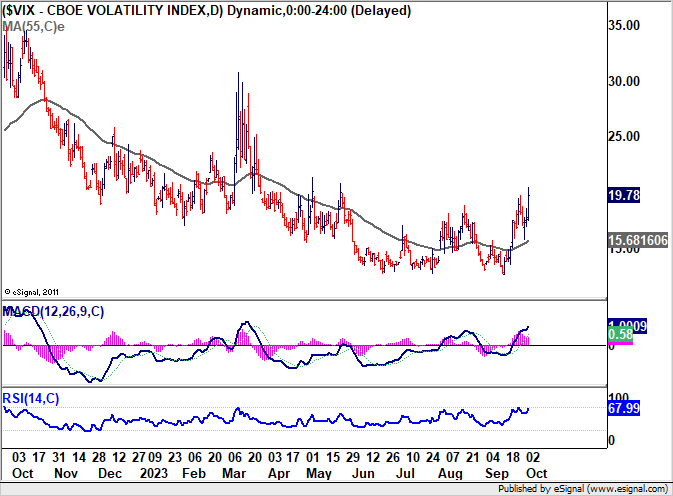

Economic storm clouds appear to be gathering on the horizon. With DOW experiencing its most significant drop since March and key Treasury yields touching multi-year highs, whispers of a potential recession are becoming more audible. This is further exacerbated by the behavior of VIX, often dubbed the “fear index”, which indicates heightened market apprehensions.

DOW plummeted by -430.97 points, or -1.29%, nudging it into negative territory for the year, now lagging by -0.4%. This downturn wasn’t isolated to stocks. The 10-year yield reached a staggering 4.8%, a pinnacle not seen in 16 years. Similarly, 30-year yield hit a peak of 4.925%, levels of which we haven’t seen since 2007.

The narrowing gap between the 2-year and 10-year Treasury yields, contracting to a mere 35 basis points from over 100 basis points a few months earlier, is especially concerning. This normalization, or “de-inverting”, of a vital part of the yield curve is often viewed as a precursor to economic downturns, igniting debates on the imminence of a recession.

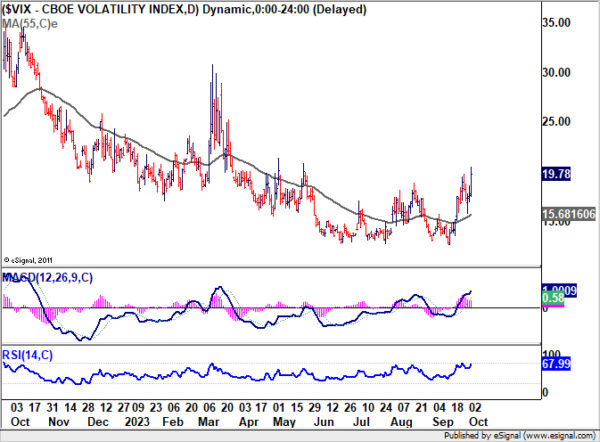

Adding to the market’s jitters, VIX has climbed for three consecutive sessions, momentarily crossing the critical 20 level and finishing at a six-month high. Values below 20 on the VIX generally signify market stability, but as it surpasses this threshold, it denotes an environment fraught with investor unease and skittishness.

Back to DOW, it’s now pressing and important near fibonacci support at 38.2% retracement of 28660.94 to 35679.13 at 32998.17. Sustained break of this level will strengthen the case that fall from 35679.13 is reversing whole rise from 28660.94. This decline could be viewed as the third leg of the long term pattern from 36952.65 high. Deeper fall would be seen to 31.429.82 support, which is close to 61.8% retracement at 31341.88.

In any case, near term outlook will stay bearish as long as 34029.22 support turned resistance holds. The rest of the week, with ISM services today and non-farm payrolls release on Friday, will be crucial.

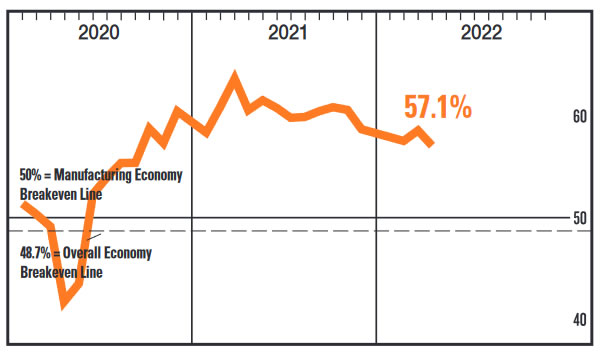

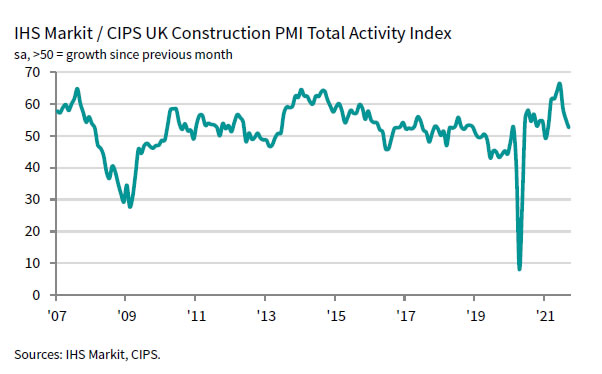

UK PMI construction rose to 53.1, marks three months of sustained recovery

UK PMI construction rose to 53.1 in June, up from 52.5 and beat expectation of 52.0. Markit noted in the release that house building remains best performing area of activity. Also, new orders rise at fastest pace since May 2017 and input cost inflation accelerates in the month.

Tim Moore, Associate Director at IHS Markit and author of the IHS Markit/CIPS Construction PMI® :

“The latest increase in UK construction output marks three months of sustained recovery from the snow-related disruption seen back in March. A solid contribution from house building helped to drive up overall construction activity in June, while a lack of new work to replace completed civil engineering projects continued to hold back growth.

“Of the three main categories of construction work, commercial building was sandwiched in the middle of the performance table during June. Survey respondents suggested that improved opportunities for industrial and distribution work were the main bright spots, which helped to offset some of the slowdown in retail and office development.

“Stretched supply chains and stronger input buying resulted in longer delivery times for construction materials during June. At the same time, higher transportation costs and rising prices for steel-related inputs led to the fastest increase in cost burdens across the construction sector since September 2017.”

Full UK PMI construction release.