Eurozone PMI Manufacturing rose to 62.4 in March, up from 57.9, well above expectation of 57.9. That’s a record high since June 1997. PMI Services improved to 48.8, up from 45.7, beat expectation of 46.1, a 7-month high. PMI Composite rose to 52.5, up from 48.8, an8-month high.

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone economy beat expectations in March, showing a much better than anticipated expansion thanks mainly to a record surge in manufacturing output… The outlook has deteriorated, however, amid rising COVID-19 infection rates and new lockdown measures. This two-speed nature of the economy will therefore likely persist for some time to come, as manufacturers benefit from a recovery in global demand but consumer-facing service companies remain constrained by social distancing restrictions.

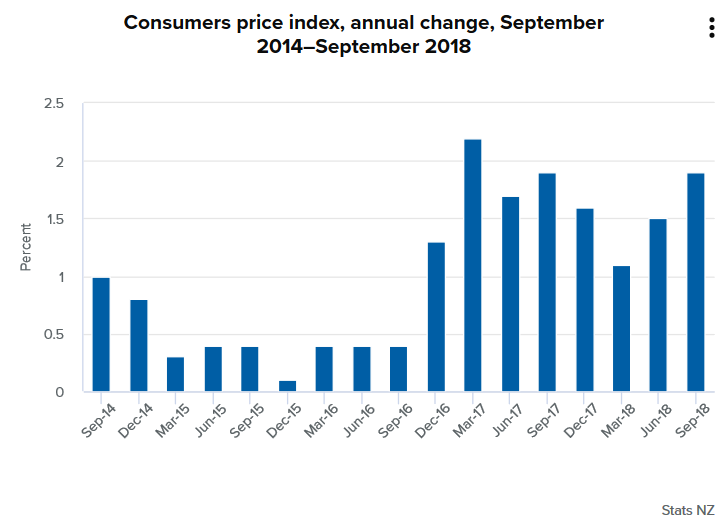

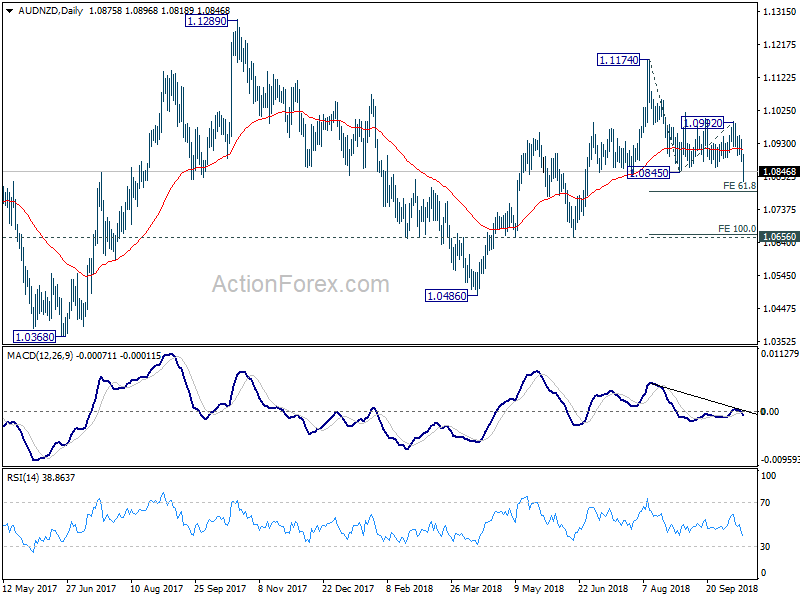

New Zealand trade surplus at NZD 217m in Feb, import hits Feb record high, NZD broadly higher

NZD trades generally higher in Asian session after trade balance data.

Accord to Stats NZ Tatauranga Aotearoa, for February 2018 compared with February 2017:

NZD is trading higher together with commodity currencies in general, as seen in daily heatmap.