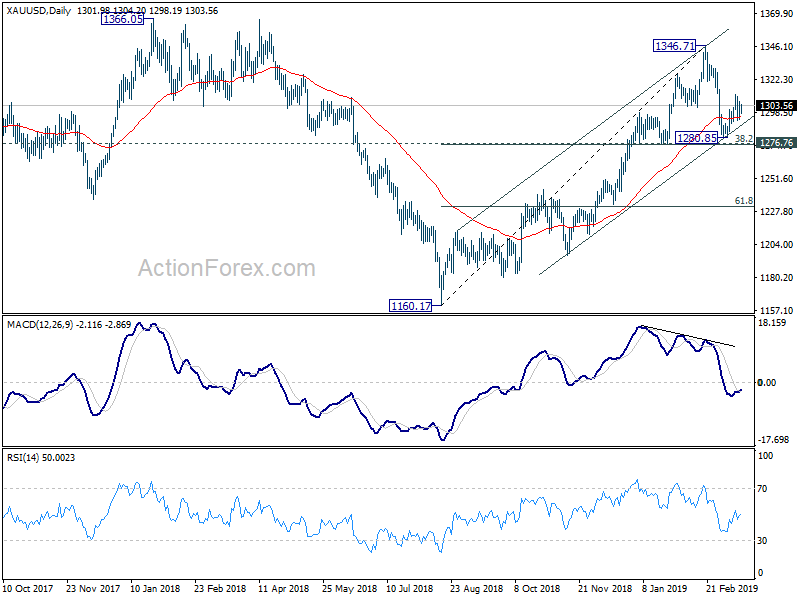

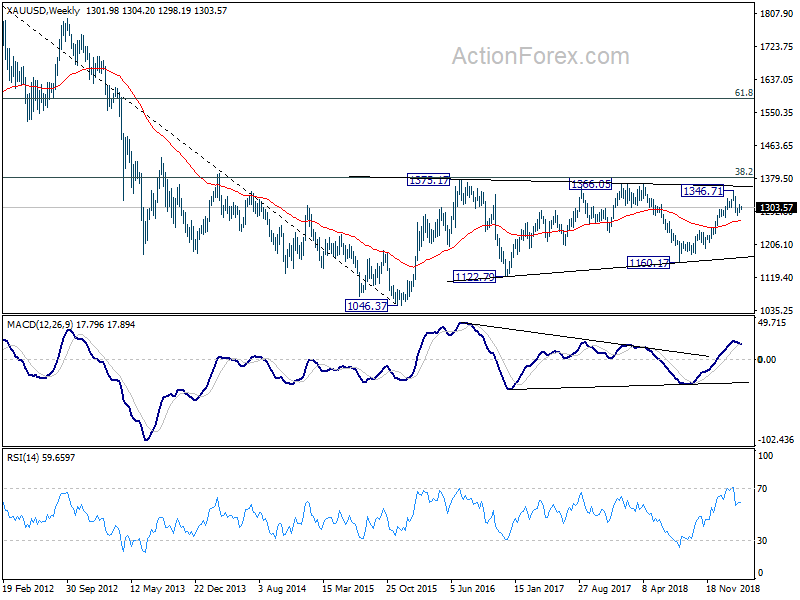

Gold drew support from rising channel line and recovered after hitting 1280.85. So far, it’s held above 1276.76 cluster support (38.1% retracement of 1160.17 to 1346.17 at 1275.45). Thus, there is no indication of trend reversal yet. Rise from 1160.17 could extend further. Break of 1346.71 will target key fibonacci level of 38.2% retracement of 192.070 to 1046.37 at 1380.36. For now, we don’t see enough momentum to break through this 1380.36 key fibonacci level yet.

On the downside, decisive break of 1275.45/1276.76 should confirm completion of whole rise from 1160.17. In that case, gold should have started another falling leg inside the long term range pattern. Deeper fall should then be seen back towards 1160.17 support.

Fed Rosengren: CARES Act a good start but we have to do more

Boston Fed President Eric Rosengren said yesterday that Fed has “acted quickly to address spillovers from the economic disruption” caused by coronavirus pandemic. But “we are probably going to have to do more than what was jut in the CARES Act, but I think it was a very good start in trying to mitigate some of the costs”. He referred to the recently passed USD 2T Coronavirus Aid, Relief and Economic Security (CARES) Act.

Rosengren also added “we’re witnessing the pandemic’s stark effects on public health. Meanwhile, the necessary response – social distancing – has stilled our strong economy, disrupting countless lives and livelihoods.” Social distancing practices are also “distorting the credit and liquidity flows that underpin our economy, threatening the greater pain of a full‐blown financial crisis.”