In recent weeks, the antipodean currencies have encountered turbulent waters, contending for the title of the month’s poorest performers. Reserve Banks of both Australia and New Zealand are widely perceived to have reached the peaks of their ongoing tightening cycles. In contrast, ECB and BoE (and less certaintly Fed) seem poised for further rate hikes. Also, the broader sentiment, underpinned by belief that global interest rates may remain elevated longer than previously anticipated, has notably dampened risk appetites.

However, recent economic concerns stemming from China have played a pivotal role in the accelerated depreciation of these currencies in the last fortnight. China’s less-than-stellar economic recovery post its stringent Covid lockdowns, coupled with looming deflation risks and challenges in its property and finance sectors, have further intensified the pressure on the antipodean currencies. Additionally, PBoC milder than anticipated rate cut today further dampened sentiments towards these currencies.

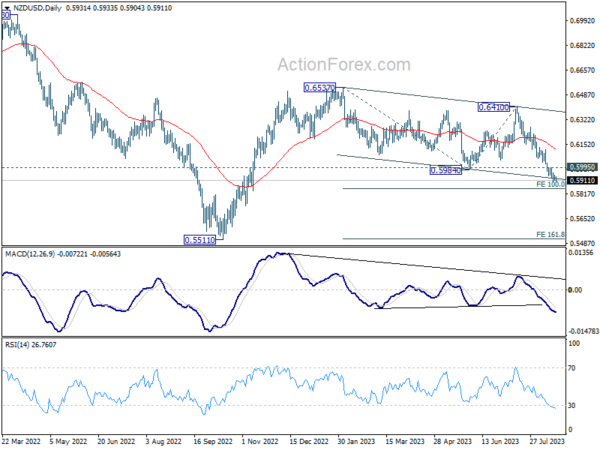

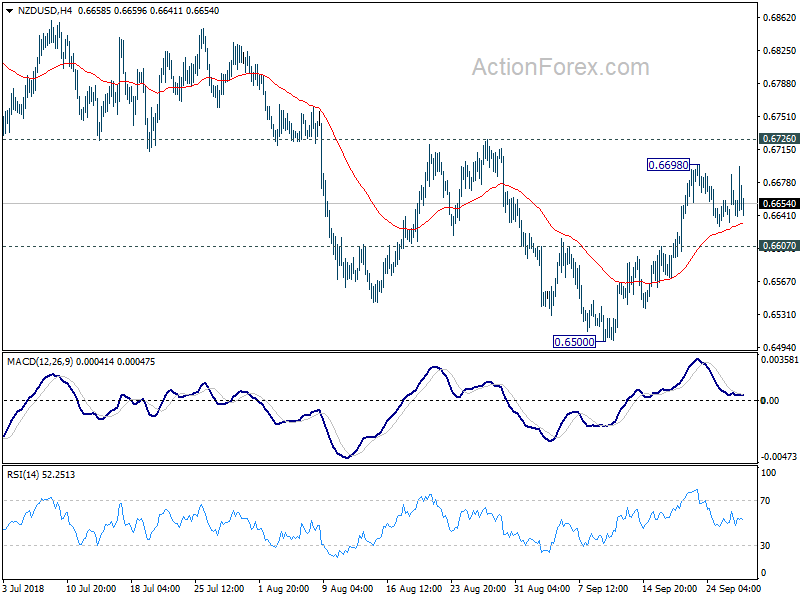

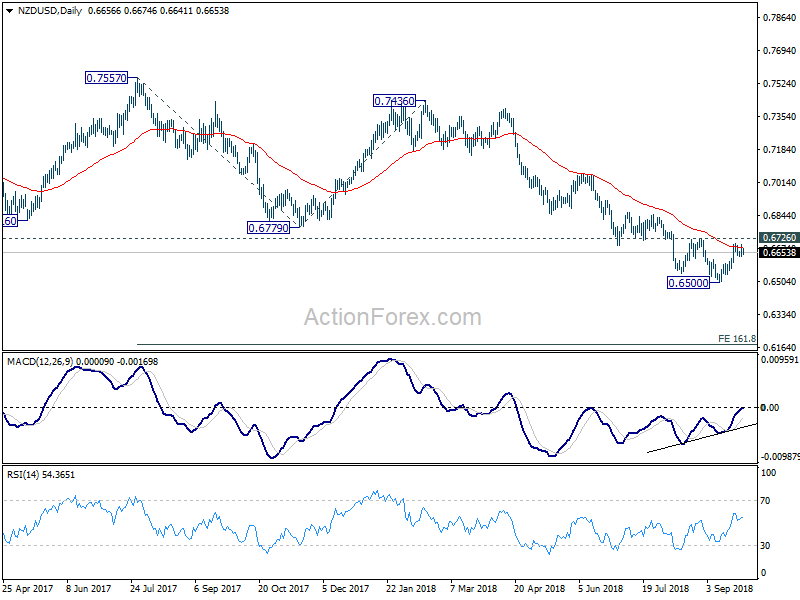

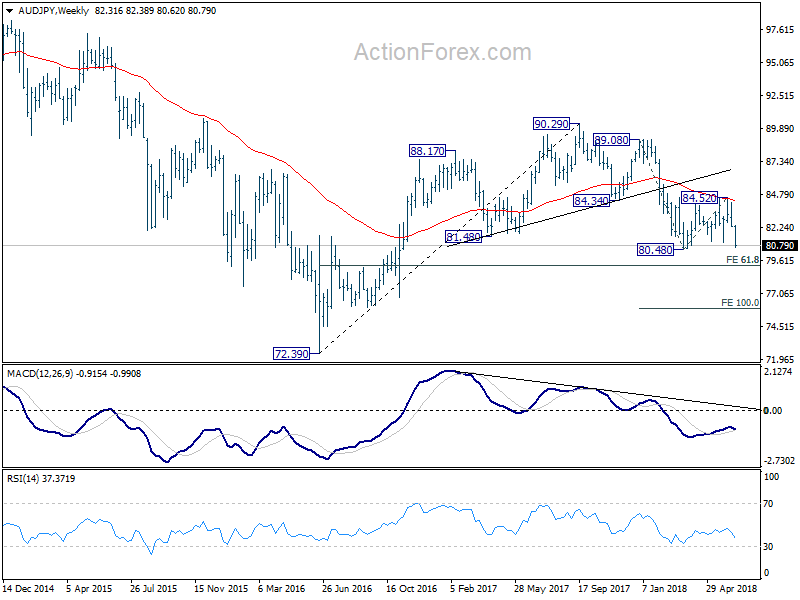

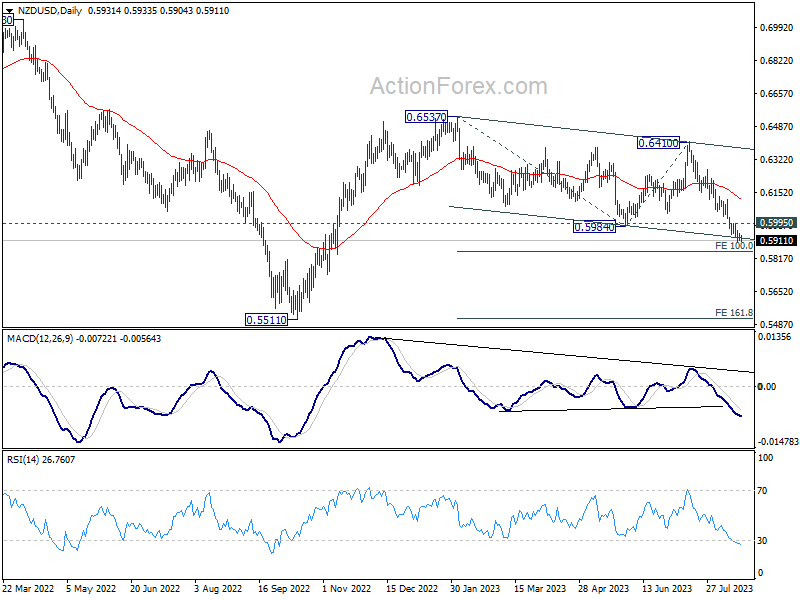

Technically speaking, however, there is prospect of a near term bounce in NZD/USD, given that it’s now pressing a medium term channel support on oversold condition. Break above 0.5995 resistance will trigger a rebound to 55 D EMA (now at 0.6117). However, deeper decline and firm break of 100% projection of 0.6537 to 0.5984 from 0.6410 at 0.5857 could prompt downside acceleration to 161.8% projection at 0.5515, which is close to 0.5511 long term support (2022 low).

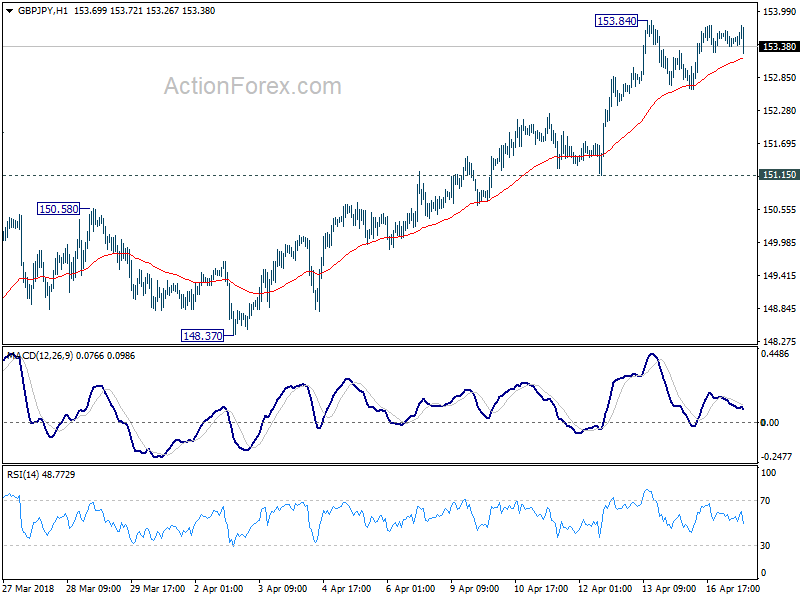

GBPJPY continues to be held below 153.84 temporary top.

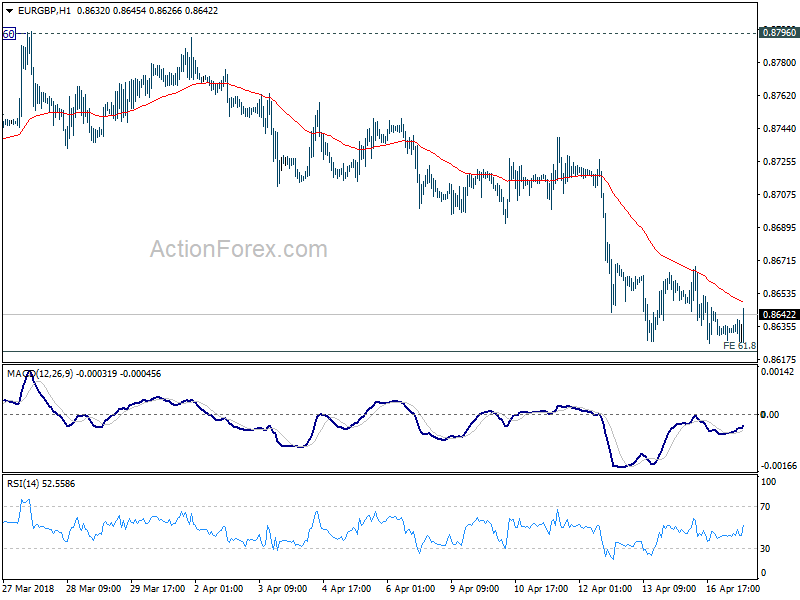

GBPJPY continues to be held below 153.84 temporary top. EURGBP also recovers as bounded in tight range.

EURGBP also recovers as bounded in tight range. GBP bulls will probably need to wait for tomorrow’s CPI before making another strike.

GBP bulls will probably need to wait for tomorrow’s CPI before making another strike.

Australia AiG services rose to 61.2, highest since 2003

Australia AiG Performance of Services Index rose 0.2 pts to 61.2 in May. That’s the highest monthly result since October 2003, indicating a stronger expansion. Four of the five services sectors indicated expansion while the other was broadly stable. Four of the five activity indicators, sales, ne orders, employment and deliveries, showed positive results.

Ai Group Chief Executive, Innes Willox, said: “Australia’s services sector maintained its momentum in May…. With existing capacity well utilised, and with reports of labour shortages becoming more common, conditions were in place for a substantial lift in investment in the sector.”

Full release here.