ECB President Christine Lagarde said in a at the Reuters Next conference that Bitcoin is a “highly speculative asset, which has conducted some funny business and some interesting and totally reprehensible money laundering activity”. As for crytopcurrencies in general, she said, “there has to be regulation. This has to be applied and agreed upon … at a global level because if there is an escape that escape will be used.”

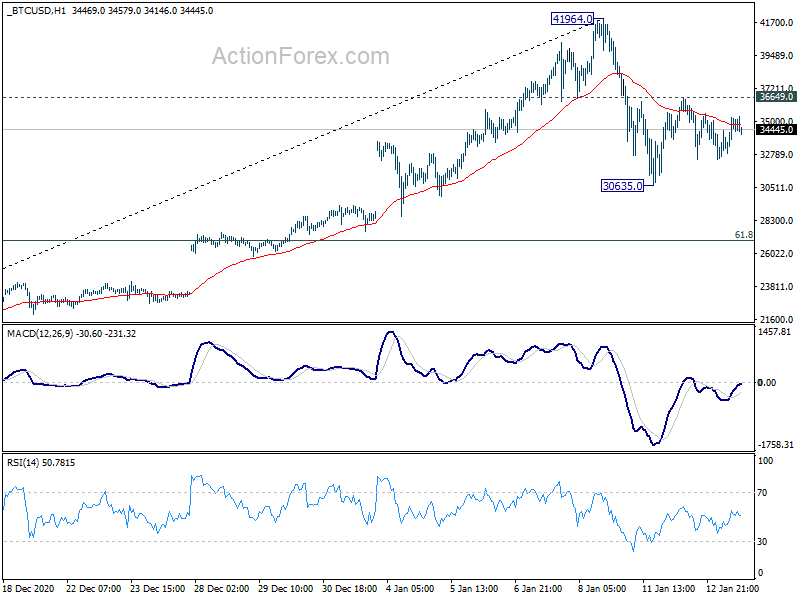

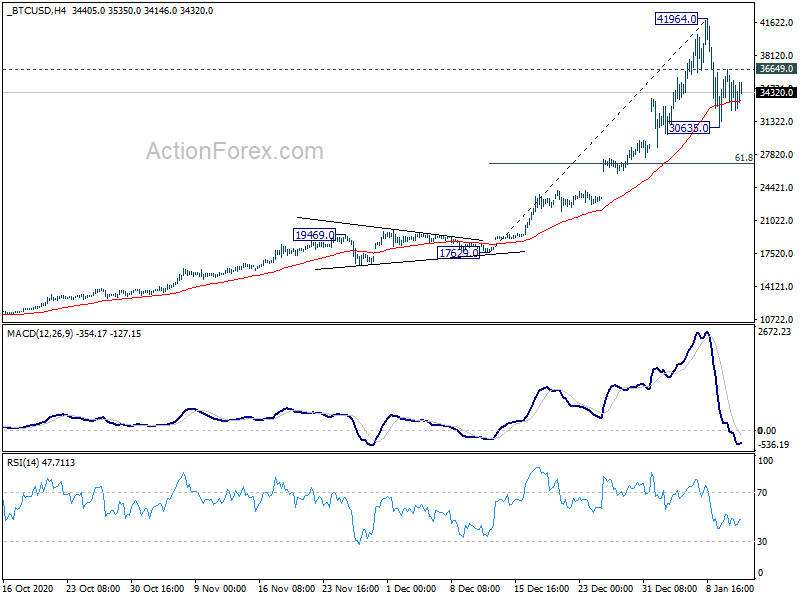

Bitcoin’s pull back from 41964.0 was a bit deeper than expected. But is quickly recovered back above 4 hour 55 EMA and settles in range. Though, as recovery attempt was so far held by 55 H EMA, another fall would be mildly in favor, but 30k handle should provide enough support for now. Meanwhile, a break above 36649.0 resistance will suggest that the correction has completed, and bring retest on the high.

USDCAD broke 1.3065 fib level on good NAFTA progress

Canadian Dollar once again surged overnight on positive NAFTA news. And it’s now trading as the strongest one for the week, maintaining gains for the day.

White House top economic advisor Larry Kudlow also said that there would be “some positive news on NAFTA … and I think the stock market is going to love that.”

It’s also reported that in the latest US proposal regarding car, parts are grouped into five categories. And some of which could have a lower requirement for North American contents or none at all.

It’s been reported repeated that Trump is pushing to have a draft NAFTA agreement by next week. For now, there are so many outstanding issues that it’s impossible to have a full agreement that soon. But there is a chance of a “symbolic agreement” signalling some consensus, as soon as next week.

Technically, the rally in CAD now sent USD/CAD through 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Also, note the head and shoulder top pattern (ls: 1.3000; h: 1.3124; rs: 1.2942) too. It’s now heading to 61.8% retracement at 1.2581 and below.