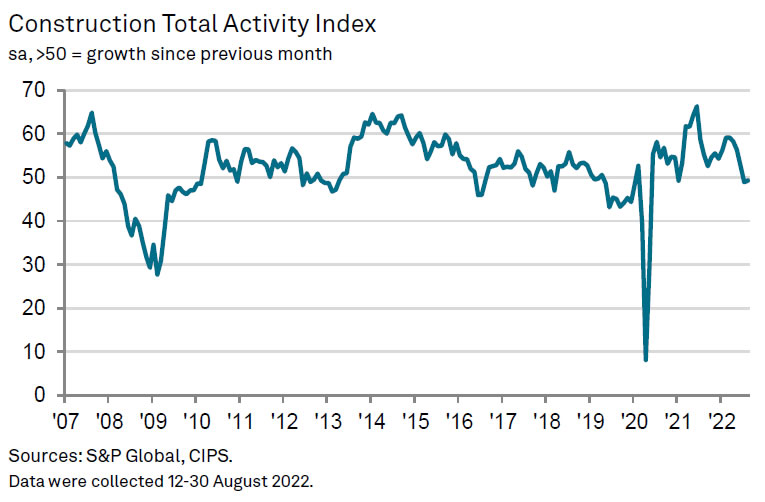

German PMI manufacturing was finalized at 58.1, unchanged from first estimate. Markit noted that After reaching a record-high last December, the PMI has fallen in every month in 2018 so far. Slower rises in new orders and employment weigh on overall performance in April. And growth remains strong by historical standards, with output up markedly on the month

Comments from Phil Smith, Principal Economist at IHS Markit:

“The manufacturing PMI slipped to a nine-month low in April, but alarm bells aren’t ringing yet. The sector boomed in the second half of 2017 and probably overheated; record input delivery delays show that supply has struggled to keep up with demand. The sector looks to have come off the boil in terms of its rate of growth, though it is still running relatively hot.

“By historical standards, April’s increase in output was robust, and it coincided with another strong round of job creation as manufacturers continued in their efforts to expand capacity. But what’s important in terms of staying in growth territory is the strength of new orders, which in April showed the smallest gain for 17 months. A further slowdown in order books in May would mean some downside risks to the outlook.

“The survey’s forward-looking business confidence gauge has stabilised after falling throughout the opening quarter, to suggest that firms themselves see growth levelling off at a lower rate than those seen in recent months.”

UK retail sales dropped -0.5% in May, ex-auto fuel dropped -0.3%

UK retail sales data for May came in mixed. No sector reported growth during the month. But the contraction was not as bad as expected.

Full release here.

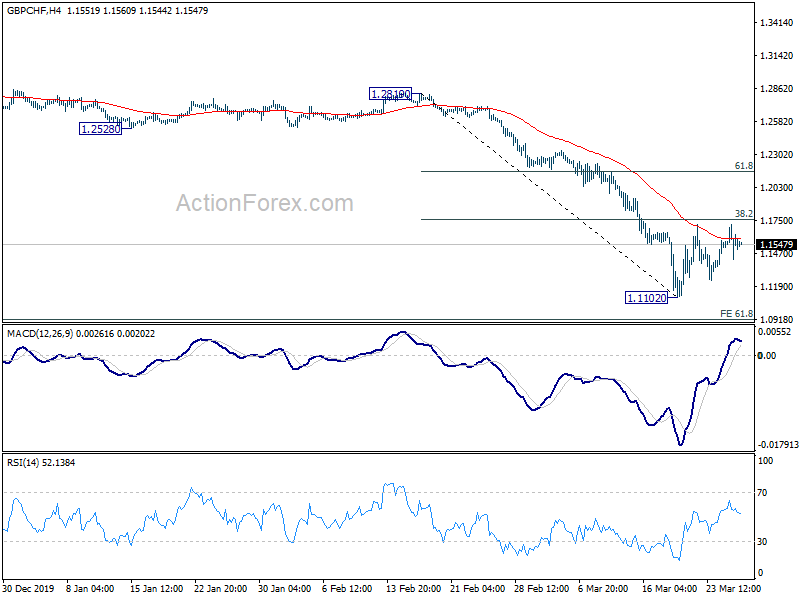

EUR/GBP has little reaction today the data. The cross pulled back this week after ECB President Mario Draghi hinted on more monetary stimulus earlier this week. For now, it’s holding on to 0.8871 minor support.