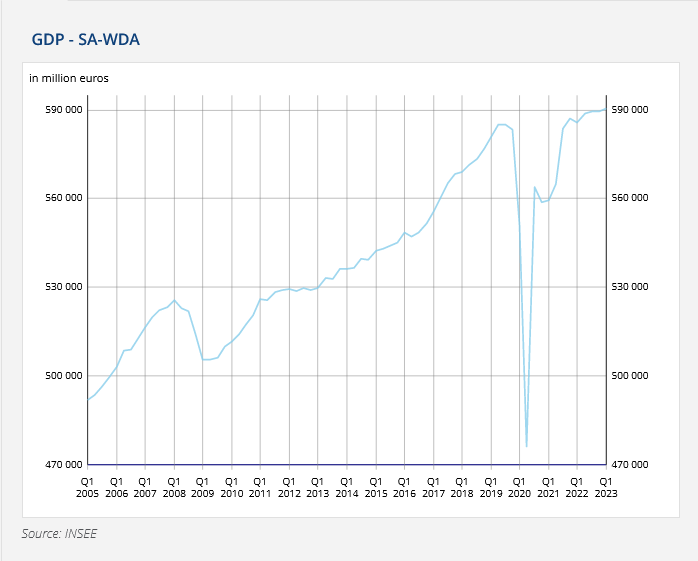

France’s Q1 GDP growth came in at a modest 0.2% qoq, slightly outperforming market expectations of 0.1% qoq.

Final domestic demand (excluding inventories) contributed negatively to GDP growth, albeit less so than in the previous quarter (-0.1 points in Q1 2023 after -0.4 points). This was due to household consumption stabilizing (0.0% after -1.0%), while gross fixed capital formation (GFCF) experienced a minor decline (-0.2% after 0.0%).

In contrast, foreign trade provided a positive contribution to GDP growth (+0.6 points after +0.2 points). Imports decreased this quarter (-0.6% after +0.1%), while exports remained strong (+1.1% after +0.9%).

Lastly, the contribution of inventory changes to GDP growth was negative this quarter (-0.3 points after +0.2 points in Q4 2022).

Australia NAB business confidence fell to -4, conditions down to 17

Australia NAB Business Confidence dropped sharply from 6 to -4 in February. Business Conditions dropped from 18 to 17. Looking at some details, trading conditions were unchanged at 27. Profitability conditions dropped from 18 to 14. Employment conditions rose from 11 to 12.

“Overall, the survey confirms the ongoing resilience of the economy through the first months of 2023, though we continue to expect a more material slowdown in demand later in the year when the full effect of rate rises has passed through,” said NAB.

Full release here.