In seasonally adjusted terms, Australia employment contracted by -19k to 12.9m in October, way below expectation of 16.2k growth. That’s also the largest monthly drop in three years since late 2016. Full-time jobs dropped -10.3k while part time jobs dropped -8.7k. Unemployment rate rose 0.1% to 5.3%, above expectation of 5.2%. At the same time, participation rate dropped -0.1% to 66.0.

Looking at some details, unemployment rate increased by 0.3 pts in New South Wales (4.8%), and by 0.1 pts in Victoria (4.8%). The seasonally adjusted unemployment rate decreased by 0.2 pts in Tasmania (5.9%), and by 0.1 pts in Queensland (6.5%), with Western Australia and South Australia recording no change.

Full release here.

The set of data suggests that Australia remains a long way from RBA’s full employment estimation, i.e., unemployment rate at around 4.5%. More monetary and fiscal stimulus is still needed to support the job and wage markets, and drive up inflation. RBA is still on track for more rate cuts or even QE next year.

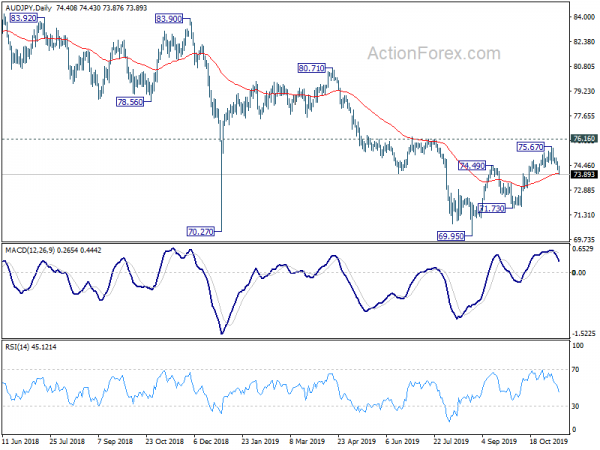

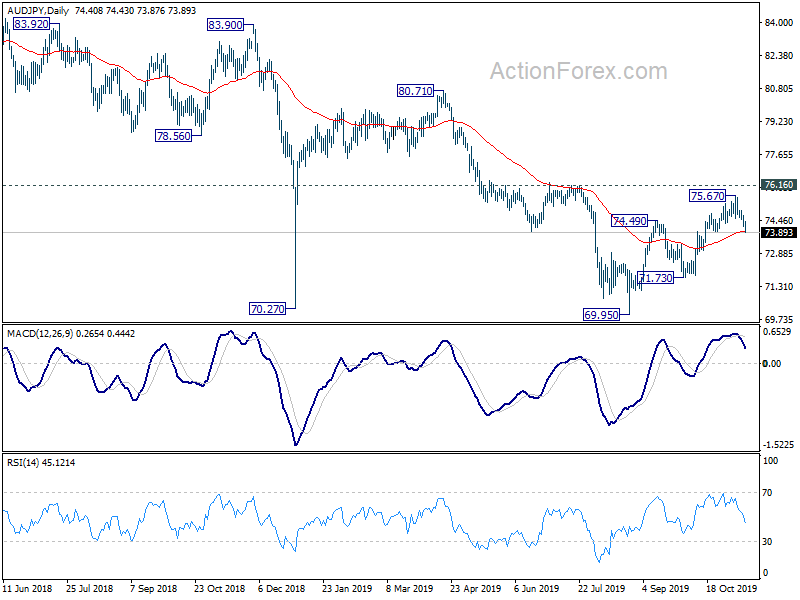

Today’s sharp fall in AUD/JPY firstly suggests short term topping at 75.67. More importantly, the break of 55 day EMA argues that corrective rise from 69.95 could have completed with three waves up to 75.67, just ahead of 76.16 structural resistance. Further fall is now in favor back to 71.73 support. Break there will reaffirm medium term bearishness for a new low below 69.95 ahead.

US ISM manufacturing dropped to 54.2, employment dropped to 52.3

US ISM manufacturing index dropped to 54.2 in February, down from 56.6, missed expectation of 56.0. Looking at the details, new orders dropped -2.8 to 55.5. Production dropped -5.7 to 54.8. Employment dropped -3.2 to 52.3. Prices dropped -0.2 to 49.4.

ISM noted that:

Full release here.