Sterling rebounds broadly today, except versus Kiwi, as bears refuse to commit further selling. Stronger than expected UK wage growth in September does provide some support. But more importantly, there are rumors flying around about an imminent Brexit deal with the EU. It’s reported that the “texts” are ready and they’re just waiting for the nod from UK Prime Minister Theresa May. We’ll see if both sides can really agree on something that paves the way to a November EU summit.

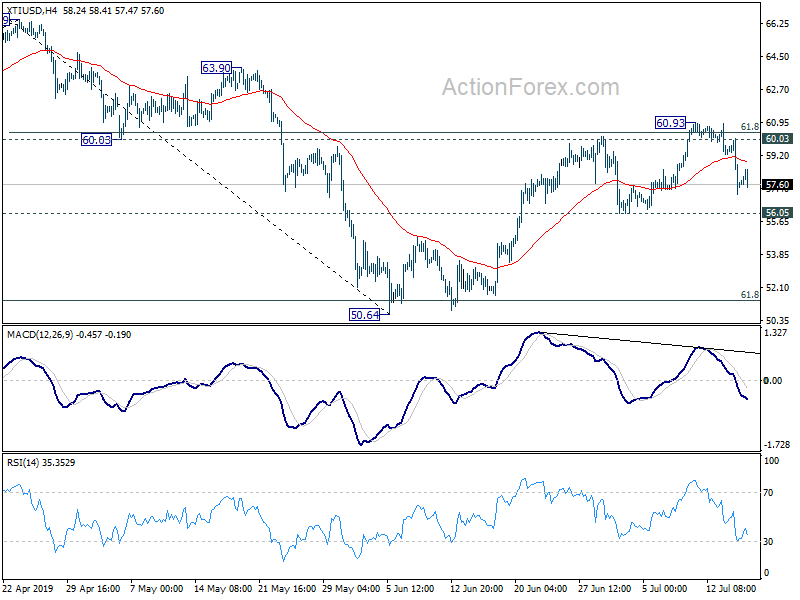

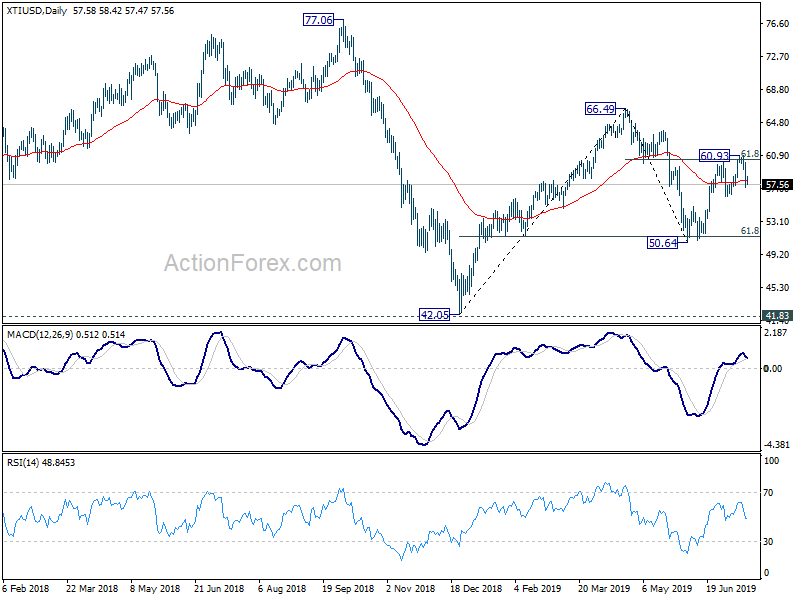

Australian and New Zealand Dollar are also strong on improved sentiment over optimism on US-China trade spat. China Vice Premier Liu He might travel to the US to meet with Treasury Secretary Steven Mnuchin shortly, to prepare for the meeting between Trump and Xi on November 30 at the G20 summit. Yen and Dollar are trading as the weakest ones, paring some of this week’s gain. Canadian Dollar is back under pressure as WTI crude oil resumes recent free fall and hit as low as 58.33.

In other markets, major European indices are trading higher at the time of writing:

- FTSE is up 0.23%

- DAX is up 0.91%

- CAC is up 0.54%

- German 10 year yield is up 0.003 at 0.404

- Italian 10 year yield is up 0.020 at 3.467. German-Italian spread is above 300

Earlier in Asia

- Nikkei closed down -2.06% at 21810.52

- Hong Kong HSI rose 0.62% to 25792.87

- China Shanghai SSE rose 0.93% to 2654.88

- Singapore Strait Times dropped -0.47% to 3053.6

- Japan 10 year yield dropped further by -0.0026 to 0.117

Eurozone goods expects down -2.7 yoy, imports fell -18.2% yoy

Eurozone exports of goods to the rest of the world dropped -2.7% yoy to EUR 227.8B in Jul. Imports fell -18.2% yoy to EUR 221.3B. Eurozone recorded EUR 6.5B trade surplus. Intra-Eurozone trade fell -7.9% yoy to EUR 211.8B.

In seasonally adjusted term, exports fell -1.7% mom to EUR 232.6B. Imports rose 0.7% mom to EUR 229.7B. Trade surplus narrowed from EUR 8.6B to EUR 2.9B, smaller than expectation of EUR 13.5B. Intra-Eurozone trade fell slightly from EUR 219.3B to EUR 218.7B.

Full Eurozone trade balance release here.