UK Prime Minister Boris Johnson is set to visit French President Emmanuel Macron and German Chancellor Angela Merkel this week. His spokesperson said that “Ahead of the G7, the prime minister believes it is important to speak to the leaders of France and Germany to deliver the message that he has been setting out through the phonecalls he’s had with leaders and face to face.”

And, she added, “it is likely they will discuss other issues: foreign policy issues, security issues and so on, but clearly Brexit will form a key part of both bilateral meetings.” However, she also reiterated that there will be no formal negotiations on Brexit until the EU dropped the Irish backstop in the withdrawal agreement.

On the other hand, European Commission spokesperson Natasha Bertaud warned that no-deal Brexit will “obviously cause significant disruption both for citizens and for businesses and this will have a serious negative economic impact:. And, “that would be proportionally much greater in the United Kingdom than it would be in the EU 27 states.” She also repeated President Jean-Claude Juncker’s comment that “it is the British who will unfortunately be the biggest losers”. if it came to a no-deal Brexit.

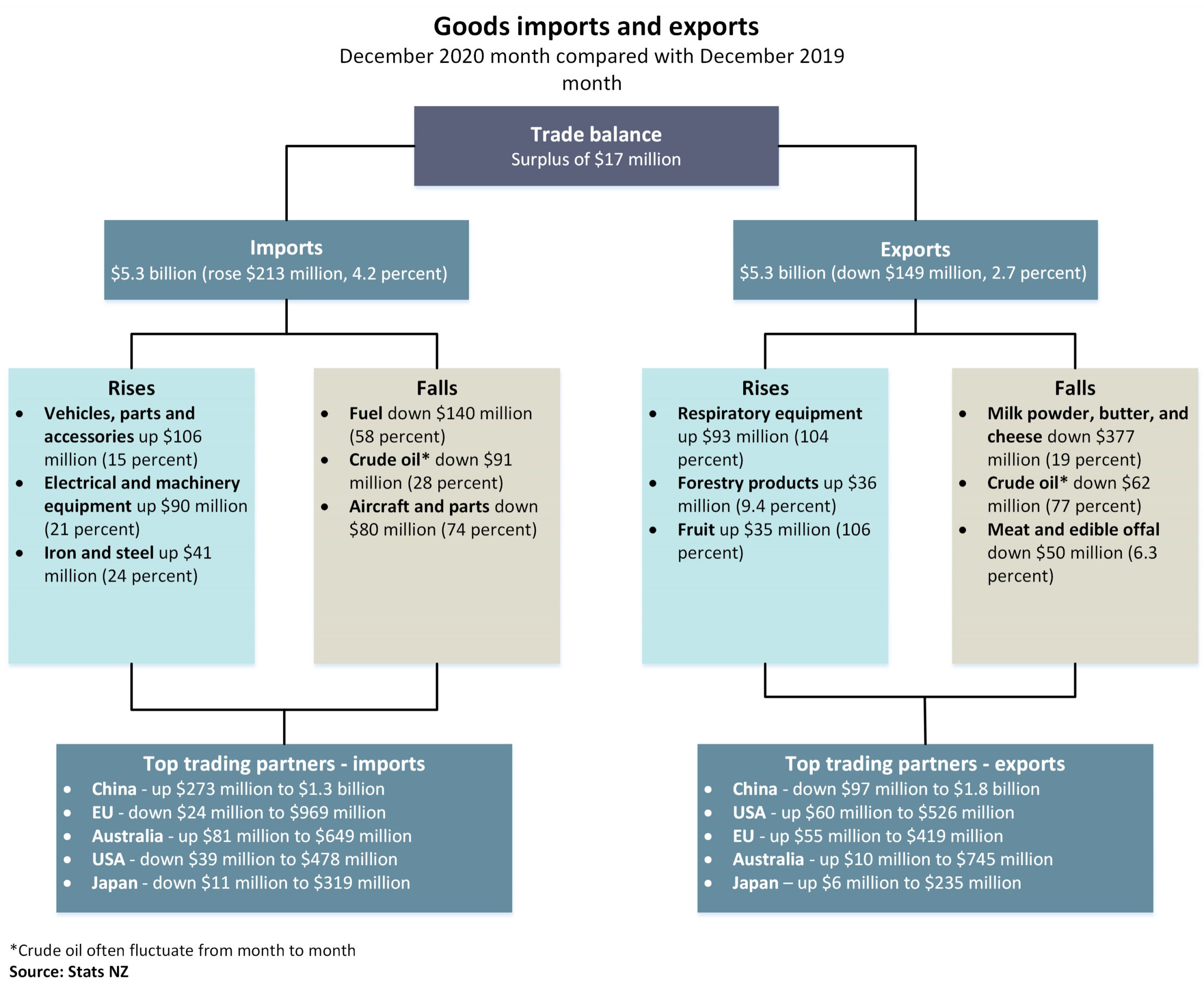

New Zealand goods exports dropped -2.7% yoy or NZD 149m to NZD 5.3B in December. Imports rose 4.2% yoy or NZD 213m to NZD 5.3B. Monthly trade surplus came in at NZD 17m, well below expectation of NZD 800m.

Exports to China was down NZD -97m, up to USA, EU, Australia and Japan. Imports from China was up NZD 273m, from AU was up NZD 81m, but down from EU, USA and Japan.

Minutes of August 4 RBA meeting showed board members “reaffirmed that there was no need to adjust the package of measures in Australia in the current environment.” Nevertheless, they agreed to “continue to assess the evolving situation” and “did not rule out adjusting the current package if circumstances warranted.”

RBA noted that “the worst of the global economic contraction had passed” but outlook remained “highly uncertain”, depending upon containment of the coronavirus. Australia’s downturn “had not been as severe as earlier expected” and “a recovery was under way in most of Australia”. Though, the recovery is likely “slower than earlier expected” too with outbreak in Victoria.

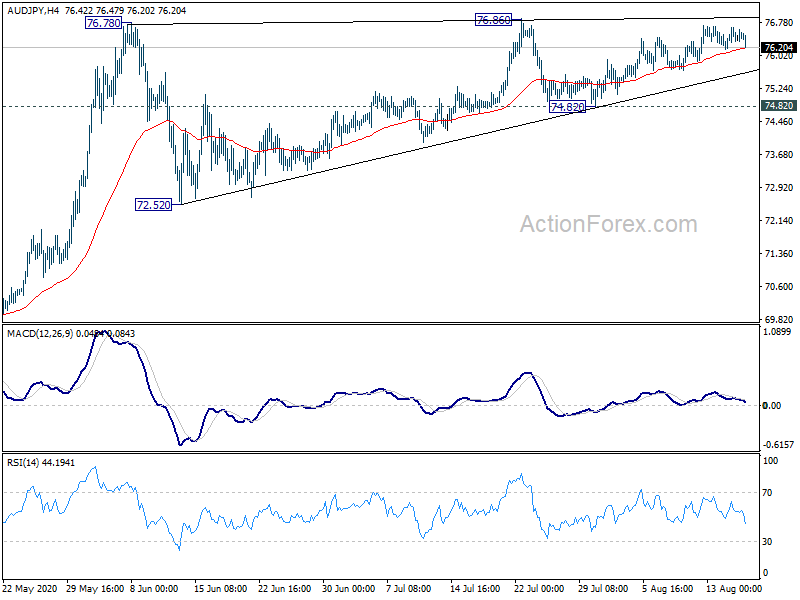

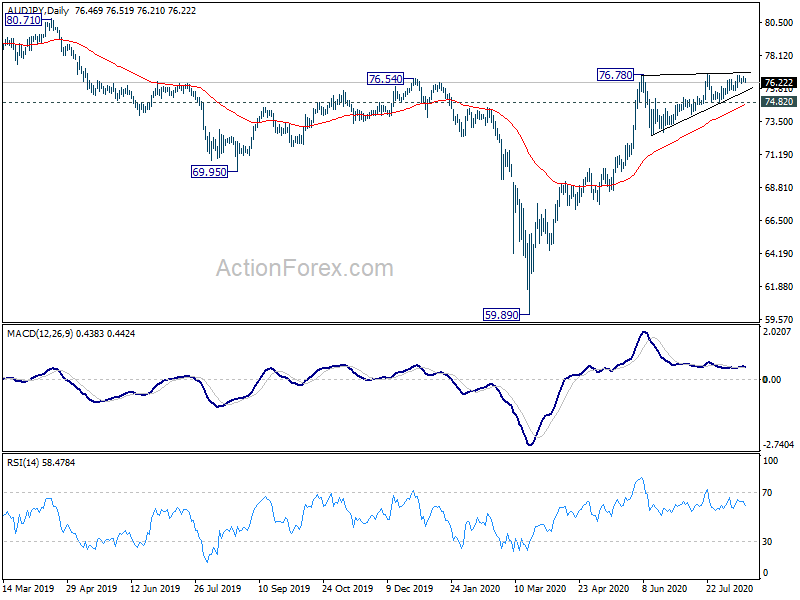

Australia Dollar is trading slightly softer after the release. AUD/JPY has been trading in a triangle pattern since early June. It should be around time for a breakout. At this point, a break above 76.86 resistance is mildly in favor as long as trend line support (now at 75.58) holds. However, the “thrust” following a triangle breakout is usually short-lived and terminal. Hence, attention would be on signs of a quick reversal in this case.

Meanwhile, sustained break of the trend line support will be the first sign of near term bearish reversal. Focus would then be turned to 74.82 support for confirmation.

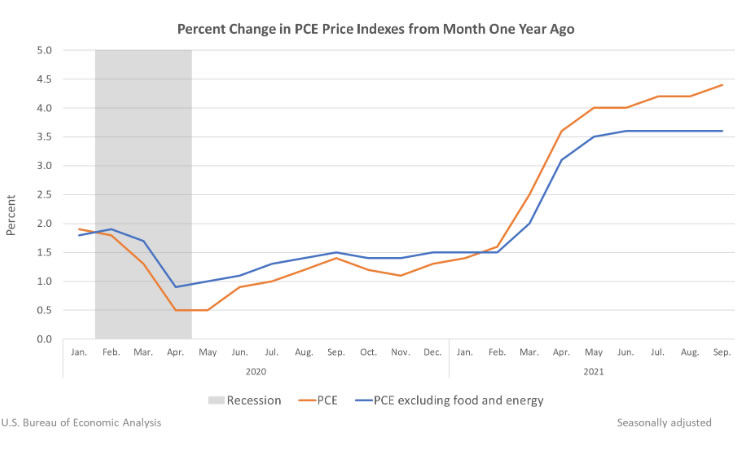

US personal income dropped -1.0% mom or USD 216.2B in September, much worse than expectation of 0.1% mom rise. Personal spending rose 0.6% mom or USD 93.4B, matched expectations. Headline PCE inflation accelerated to 4.4% yoy, below expectation of 4.7% yoy. Core PCE price index was unchanged at 3.6% yoy, below expectation of 3.7% yoy.

NIESR said the UK economy is course to contract by -0.2% in Q2, “mainly driven by the production and construction sectors”. That would be a “marked slowdown” from Q1 when growth was boosted by pre-Brexit “stockbuilding”. It added that recent surveys suggests “there has not been a material recovery in output in May”.

Garry Young, Head of Macroeconomic Modelling and Forecasting, said “The latest GDP data were weaker than expected, partly reflecting shifts in production around the original Brexit departure date, including a 24 per cent fall in car manufacturing. The underlying picture is also quite weak, with Brexit-related uncertainty at home and trade tensions abroad dragging on investment spending and economic growth”.

ECB President Mario Draghi said “the outlook for the euro area fundamentally depends on global growth momentum”. And he warned “the escalation of trade tensions, the downturn in global manufacturing and a turn in the tech cycle have increased the euro area’s external headwinds.”

ECB Chief Economist Peter Praet, on the other hand, sounds relatively more optimistic. He said “there are good reasons to say that the economy is going to stabilize, it’s probably stabilizing somewhere in the second quarter … That’s our scenario and I still believe in that scenario.”

On market pricing, Praet said “the OIS curve that came after the Watchers’ conference in Frankfurt is something that fits well with how we think financial conditions should be today”. Overnight Indexed Swap (OIS) curve suggests that money markets are not pricing in a rate hike from ECB for the next 21 months.

During a seminar today, BoE MPC member Jonathan Haskel emphasized the critical role of the labor market in shaping the UK’s inflation outlook.

Haskel pointed out that the labor market tightness, specifically the ratio of job vacancies to unemployment, is a key factor in assessing inflationary pressures. Although this ratio is gradually decreasing, Haskel expressed concern over the pace, stating it is “rather slowly” and it remains uncertain if it is sufficient to align inflation with the target levels.

“The persistence of inflation depends a lot on how quickly that ratio comes down,” Haskel remarked, underscoring the direct impact of labor market conditions on inflation trends.

German Chancellor Angela Merkel appeared at a business forum with Chinese Premier Li Keqiang in Beijing today, after part of her trip to China. Merkel said that her country welcomes all Chinese companies for investment. But the government checks investments in certain strategic sectors and critical infrastructure.

Merkel also urged “there will be a solution in the trade dispute with the United States since it affects everybody” in the world”

On the other hand, Li hoped that Germany will accept more Chinese companies and loosen up export rule for certain goods. Li also pledged that China is opening up its economy.

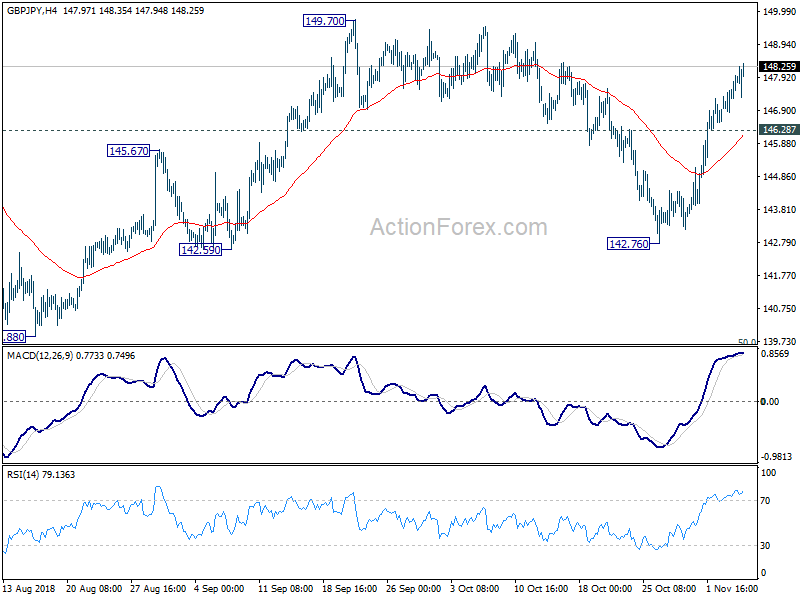

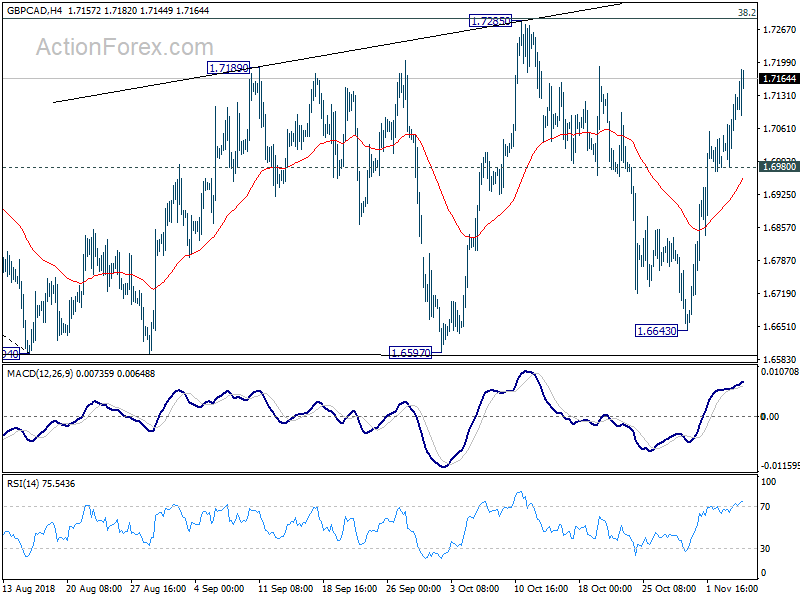

GBP/JPY and GBP/CAD are the two biggest movers today, thanks to broad based strength in the pound. Nonetheless, considering that they’re up 72 pips and 68 pips only, it’s indeed a very slow day.

For GBP/JPY, rise from 147.26 is in progress for 1349.70 resistance. Our views as discussed in the daily report is unchanged.

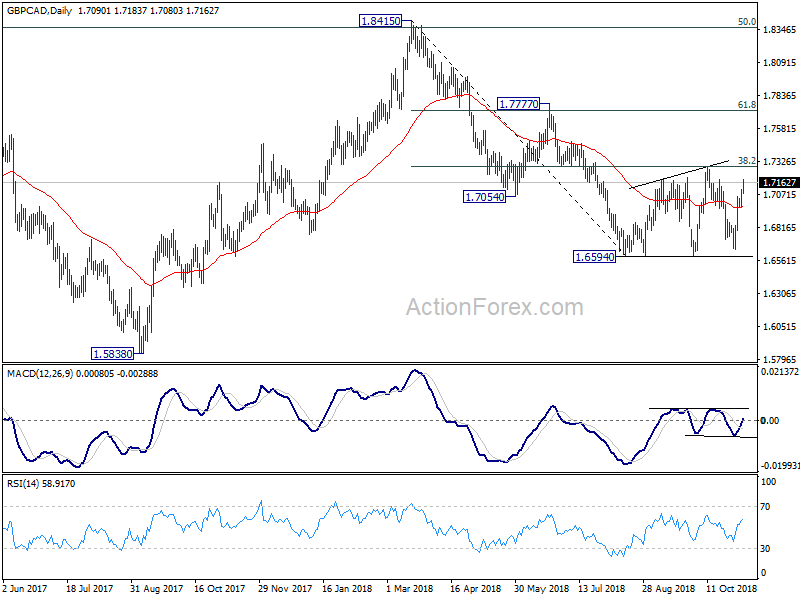

GBP/CAD’s rebound from 1.6643 accelerates higher today and reaches 1.7183 so far. Further rise is likely for 1.7285 resistance. However, for now, we’re viewing price actions from 1.6594 as forming a corrective pattern. That is, rise from 1.6643 is merely a leg inside the pattern. Hence, we’d expect strong resistance from 38.2% retracement of 1.8415 to 1.6594 at 1.7290 to limit upside. Break of 1.6980 minor support should bring retest of 1.6594 low.

Firm break of 1.7290 fibonacci level could bring stronger rebound to 61.8% retracement at 1.7719. But, we’ll still treat it as part of the correction from 1.6594 unless we see more evidence of trend reversal, in terms of price structure. The down trend from 1.8415 is still expected to resume, just at a later stage.

Bank of England, UK’s Financial Conduct Authority and US Commodity Futures Trading Commission announced measures today to ensure Brexit, in whatever form “will not create regulatory uncertainty regarding derivatives market activity between the UK and US”. Measures include continued supervisory co-operation, extension of existing CFTC relief to EU firms to UK after Brexit. Also, US trading venues, firms and CCPs will be able to continue providing services in the UK.

In a joint statement, BoE Governor Mark Carney said “As host of the world’s largest and most sophisticated derivative markets, the US and UK have special responsibilities to keep their markets resilient, efficient and open.

“The measures we are announcing today will do that. Market participants can be confident that the clearing and trading of derivatives between the UK and US will maintain the high standards of today when the UK leaves the EU”.

Carney also warned that “The biggest issue from a financial stability perspective, from a market integrity perspective, from a continuity perspective, is a no-deal scenario by the end of March.”

In the highly anticipated Jackson Hole speech, Fed chair Jerome Powell said “substantial further progress test has been “met for inflation”. And there has also been “clear progress toward maximum employment”.

At July’s FOMC meeting, he view was that if the economy “evolved broadly as anticipated”, it could be “appropriate to start” tapering this year. However, “the intervening month has brought more progress in the form of a strong employment report for July, but also the further spread of the Delta variant.”

He added that Fed will be “carefully assessing incoming data and the evolving risks”, without giving any hint of the timing and pace of tapering

Australian Dollar suffers another round of selloff today after RBA revealed rather dovish economic forecasts in the Statement on Monetary Policy. In the summary part, Governor Philip Lowe’s “balanced” turn was echoed.

The first scenario is “further progress in reducing unemployment and bringing inflation into the target range can reasonably be expected.” In this case, higher interest rate “would become appropriate at some point”. However, in other scenarios, “If there were then to be a sustained increase in unemployment and a lack of progress in returning inflation to target, it might instead be appropriate to lower the cash rate.”

RBA now judges ” the probabilities of these two sets of scenarios have shifted to be more evenly balanced than previously.”

In the new economic projections:

2019 year-end growth was revised to 3%, down from 3.25%.

2020 year-end growth was revised to 2.75%, down from 3%.

June 2020 unemployment rate was revised to 5%, up from 4.75%.

That is, unemployment rate will fall at a slower pace.

2019 year-end CPI was revised to 1.75%, down from 2.25%.

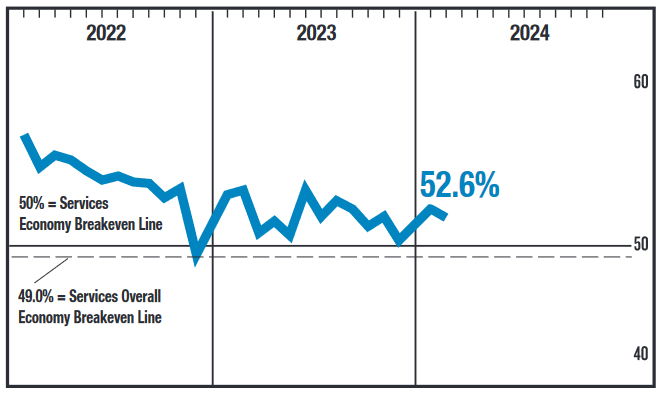

US ISM Services PMI fell from 53.4 to 52.6 in February, worse than expectation of 53.0. Looking at some details, business activity/production rose from 55.8 to 57.2. New orders rose from 55.0 to 56.1. Employment fell from 50.5 to 48.0, back in contraction. Prices fell from 64.0 to 58.6.

Anthony Nieves, Chair of ISM Services Business Survey Committee, said, “The slight decrease in the rate of growth in February is a result of faster supplier deliveries and the contraction in the Employment Index. The majority of respondents are mostly positive about business conditions. Respondents remain concerned about inflation, employment and ongoing geopolitical conflicts.”

“The past relationship between the Services PMI and the overall economy indicates that the Services PMI for February (52.6 percent) corresponds to a 1.2-percent increase in real gross domestic product (GDP) on an annualized basis.”

ECB Executive Board Member Fabio Panetta warned in a conference today, “the probability of a recession is increasing. If we will have a significant slowdown or even a recession, this would mitigate inflationary pressures.”

“I think that (policy) adjustments are possible but the most recent evolution of the economy should induce us to exercise one of the main features of central bankers which is prudence,” he said.

He also added that real rates are “not too far from the estimated neutral level.

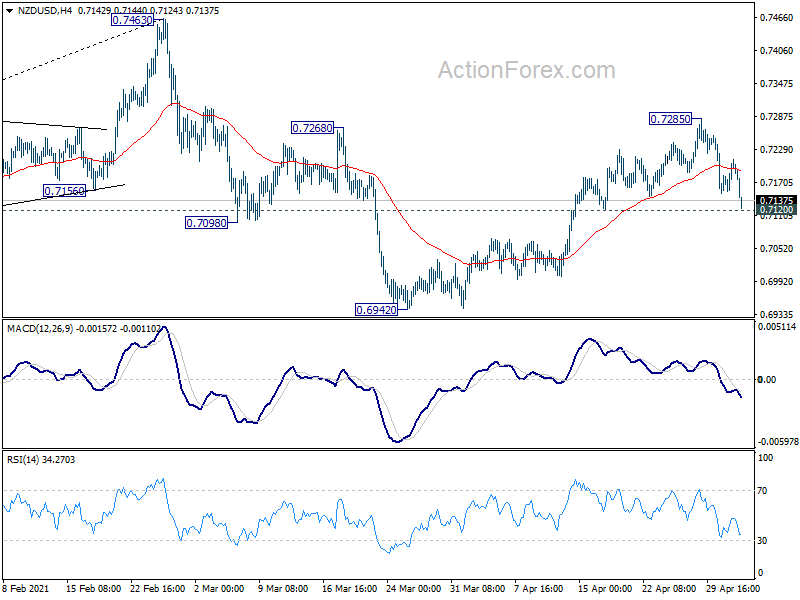

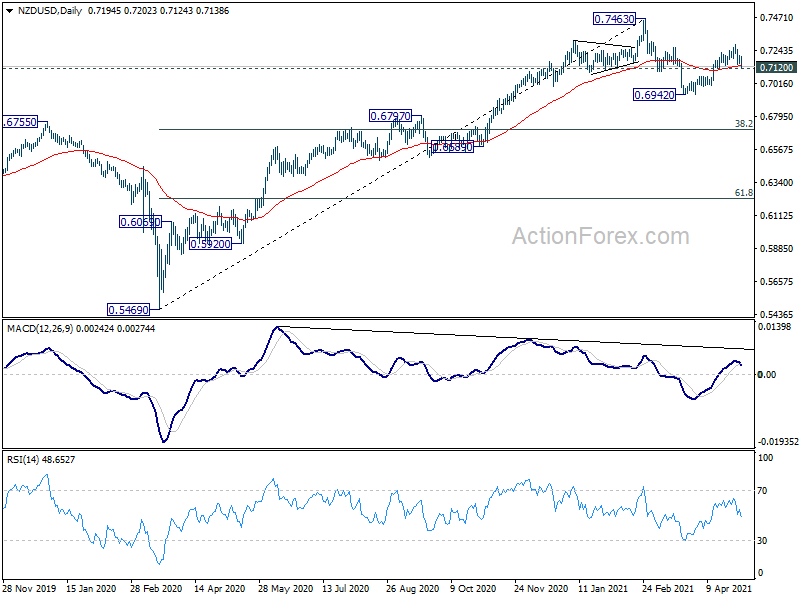

New Zealand Dollar weakens notably today, in particular against Dollar and Yen. NZD/USD was apparently rejected by 0.7268 resistance, after failing to sustain above it. Focus is now back o 0.7120 minor support. Break there will suggest that recovery from 0.6942 has completed at 0.7285. The corrective pattern from 0.7463 would have started the third leg back to 0.6942 support and below. Though, strong rebound from current level will retain near term bullishness. Break of 0.7285 will bring retest of 0.7463 high.

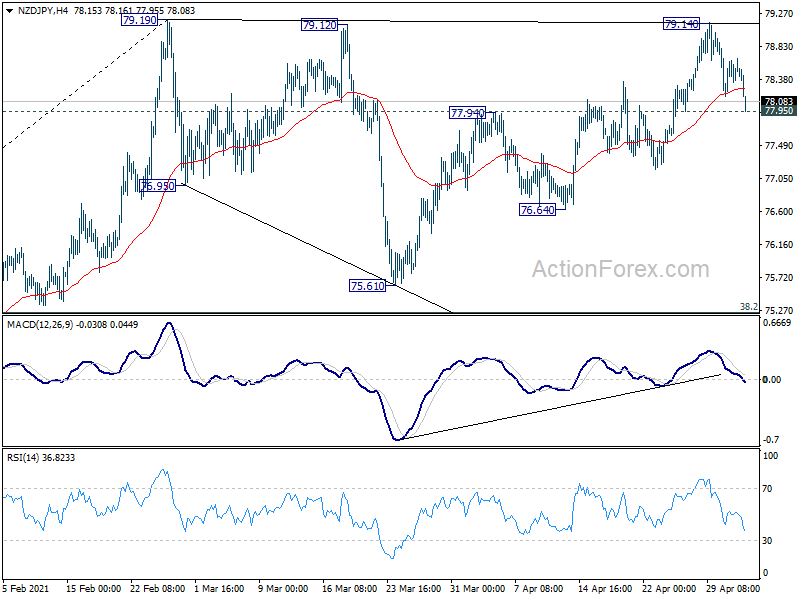

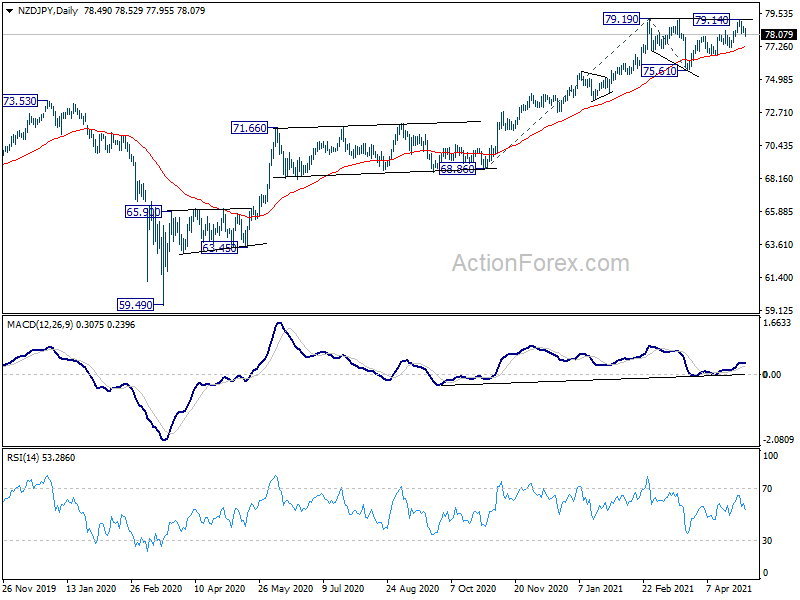

NZD/JPY was also rejected by 79.19 resistance an retreated notably. Focus is back on 77.94 support. Break there should indicate that consolidation pattern from 79.19 has started another falling leg. Deeper fall would then be seen back to 76.64 support and below. Though, rebound from current level will keep favor on the side of upside breakout. Break of 79.19 will resume larger uptrend.

RBNZ chief economist Paul Conway said today that 50bps rate hikes are the way forward, and he’s confident of soft landing as the labor market is strong.

“75 wasn’t seriously on the table because we are pretty convinced that we can get to where we need to get with 50-point increments,” he said. Also, the central bank was “signaling there’s probably some more 50 points coming over the next little while.”

On the economy, Conway said “it’s difficult to engineer a soft landing — typically a significant reduction in inflation is accompanied by negative economic growth — but there’s reasons to believe New Zealand is well placed to pull it off this time around.”

“The labor market is strong and that’s the underlying reason why the New Zealand economy is well placed to weather the storm,” he added.

Japan Prime Minister Shinzo Abe was asked in the parliament today about Trump intention to impose tariffs on car imports using national security as excuse. Abe said he would seek to convince Trump that Japan carmakers are important in boosting the US economy.

He noted that Japan automakes have “created jobs and made huge contributions to the US economy.” And he added that the number of cars Japanese automakers produce in the US is double the number it exports to the country.

And he emphasized that “as a country that prioritizes a rule-based, multilateral trade system, Japan believes that any steps taken on trade must be in line with World Trade Organization rules.”

Separately, he added that “Japan has explained to the United States its stance that TPP is the best format for both countries. We will continue to talk with the United States based on this view.”

ECB President Mario Draghi emphasized in a conference in Frankfurt yesterday that any monetary policy adjustments must be “predictable” and carried out “at a measured pace”. For now, he said ECB “still need to see further evidence that inflation dynamics are moving in the right direction”. Therefore, “monetary policy will remain patient, persistent and prudent.” Draghi also added that “sharp repricing” in the financial markets must be carefully monitored.

Regarding the steel and aluminum tariffs of the US, Draghi expected the initial impact to be small. However, he warned that “there are potential second-round effects that could have much more serious consequences.” And, risks include “retaliation across other goods and an escalation of trade tensions, and the potential for negative confidence effects which would weigh on business investment in particular.”

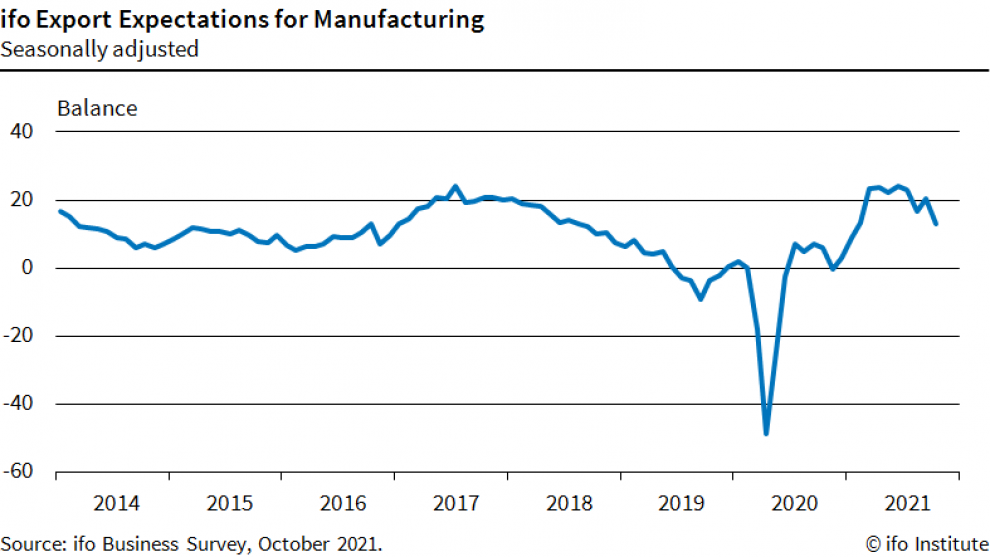

Germany’s Ifo export expectations dropped sharply from 20.5 to 13.0 in October, hitting the lowest level since February. Ifo said, “supply problems in intermediate products are now having an impact on manufacturing export”.

President of Ifo Clemens Fuest said: “In the electrical and electronics sector, export expectations have softened but remain at a high level, with companies continuing to expect good international business. However, the mood is bleaker in the chemical industry, where growth rates will be significantly slower. The situation is similar for the automotive industry. In the food and furniture industries, exports are expected to remain constant. The textile and leather industries are now preparing for declining international sales.”

UK Johnson to discuss foreign policy, security and Brexit with German Merkel and French Macron

UK Prime Minister Boris Johnson is set to visit French President Emmanuel Macron and German Chancellor Angela Merkel this week. His spokesperson said that “Ahead of the G7, the prime minister believes it is important to speak to the leaders of France and Germany to deliver the message that he has been setting out through the phonecalls he’s had with leaders and face to face.”

And, she added, “it is likely they will discuss other issues: foreign policy issues, security issues and so on, but clearly Brexit will form a key part of both bilateral meetings.” However, she also reiterated that there will be no formal negotiations on Brexit until the EU dropped the Irish backstop in the withdrawal agreement.

On the other hand, European Commission spokesperson Natasha Bertaud warned that no-deal Brexit will “obviously cause significant disruption both for citizens and for businesses and this will have a serious negative economic impact:. And, “that would be proportionally much greater in the United Kingdom than it would be in the EU 27 states.” She also repeated President Jean-Claude Juncker’s comment that “it is the British who will unfortunately be the biggest losers”. if it came to a no-deal Brexit.