BoE raises Bank Rate by 0.25% to 0.50% today, by a slight majority of 5-4 vote. Four hawks (Jonathan Haskel, Catherine L Mann, Dave Ramsden, Michael Saunders) voted for a more aggressive 50bps hike to 0.75%. The other five (Andrew Bailey, Ben Broadbent, Jon Cunliffe, Huw Pill, Silvana Tenreyro) won the vote.

Meanwhile, the MPC voted unanimously to begin to reduce stock of government bonds by ceasing to reinvest maturing assets. It also decided to start reducing stock of corporate bonds by ceasing to reinvest maturing assets and complete a bond sales program no earlier than towards the end of 2023.

Going forward, the extent of any further tightening in monetary policy will “depend on the medium-term prospects for inflation”. If the economy develops broadly in line with the February Report central projections, “some further modest tightening in monetary policy is likely to be appropriate in the coming months.”

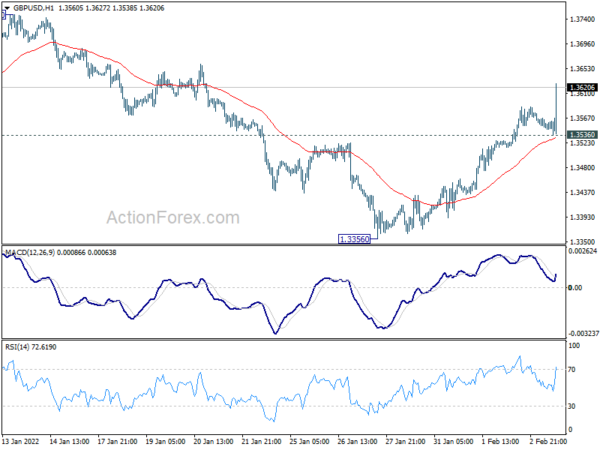

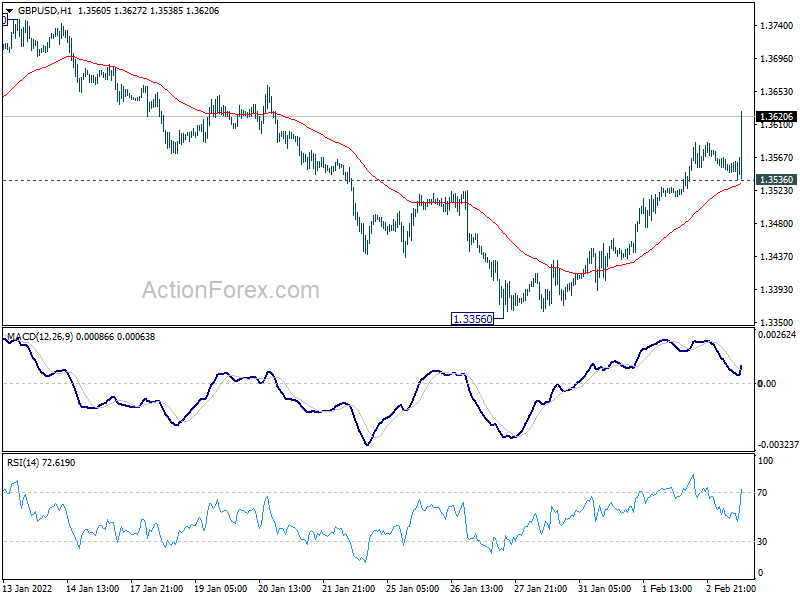

Sterling surges sharply after the release.

Full statement here.

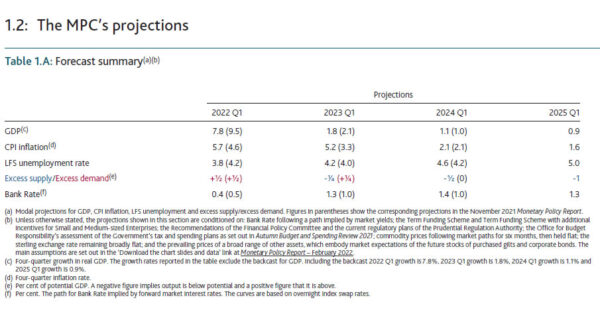

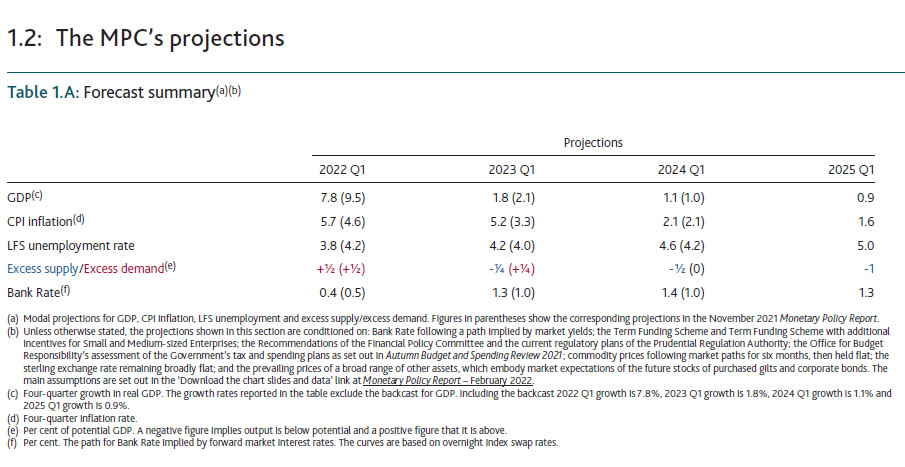

In the new four-quarter GDP projections:

- 2022 Q1 was revised down from 9.5% to 7.8%.

- 2023 Q1 was revised down from 2.1% to 1.8%.

- 2024 Q1 was revised up from 1.0% to 1.1%.

- 2025 Q1 was at 0.9% (new).

CPI inflation projections:

- 2022 Q1 raised from 4.6% to 5.7%.

- 2023 Q1 raised from 3.3% to 5.2%.

- 2024 Q1 unchanged at 2.1%.

- 2025 Q1 to slow to 1.6%.

Unemployment rate projections:

- 2022 Q1 lowered from 4.2% to 3.8%.

- 2023Q1 raised from 4.0% to 4.2%.

- 2024 Q1 raised from 4.2% to 4.6%.

- 2025 Q1 to rise to 5.0%.

Implied path for Bank Rate:

- 2022 Q1 lowered from 0.5% to 0.4%.

- 2023 Q1 raised from 1.0% to 1.3%.

- 2024 Q1 raised from 1.0% to 1.4%.

- 2025 Q1 at 1.3%.

Full Monetary Policy Report here.

RBNZ Hawkesby: Next rate move depends on global environment

RBNZ Assistant Governor Christian Hawkesby said in an interview that, after yesterday’s 50bps rate cut, “we’ve got a more balanced outlook for the OCR now”. However, he added, “even within those projections there’s some probability in there that we will need to reduce the OCR from where it is at the moment.”

Hawkesby explained that markets have already priced in a smaller 25bps before yesterday’s announce. And the New Zealand Dollar faced downward pressure after the decision, which could give an extra boost to exports. He added “it’s all part of the story of us getting back to our targets.” He hoped that the larger cut could help avoid further policy easing. But RBNA is “complete” open to use negative interest rates and other unconventional tools if necessary.

The main consideration for any next move is on global outlook. He said, “the obvious one is the global environment where we feel like the risks are tilted to the downside, and that was one of the factors that prompted us to ease with the 50 basis points this time around.”