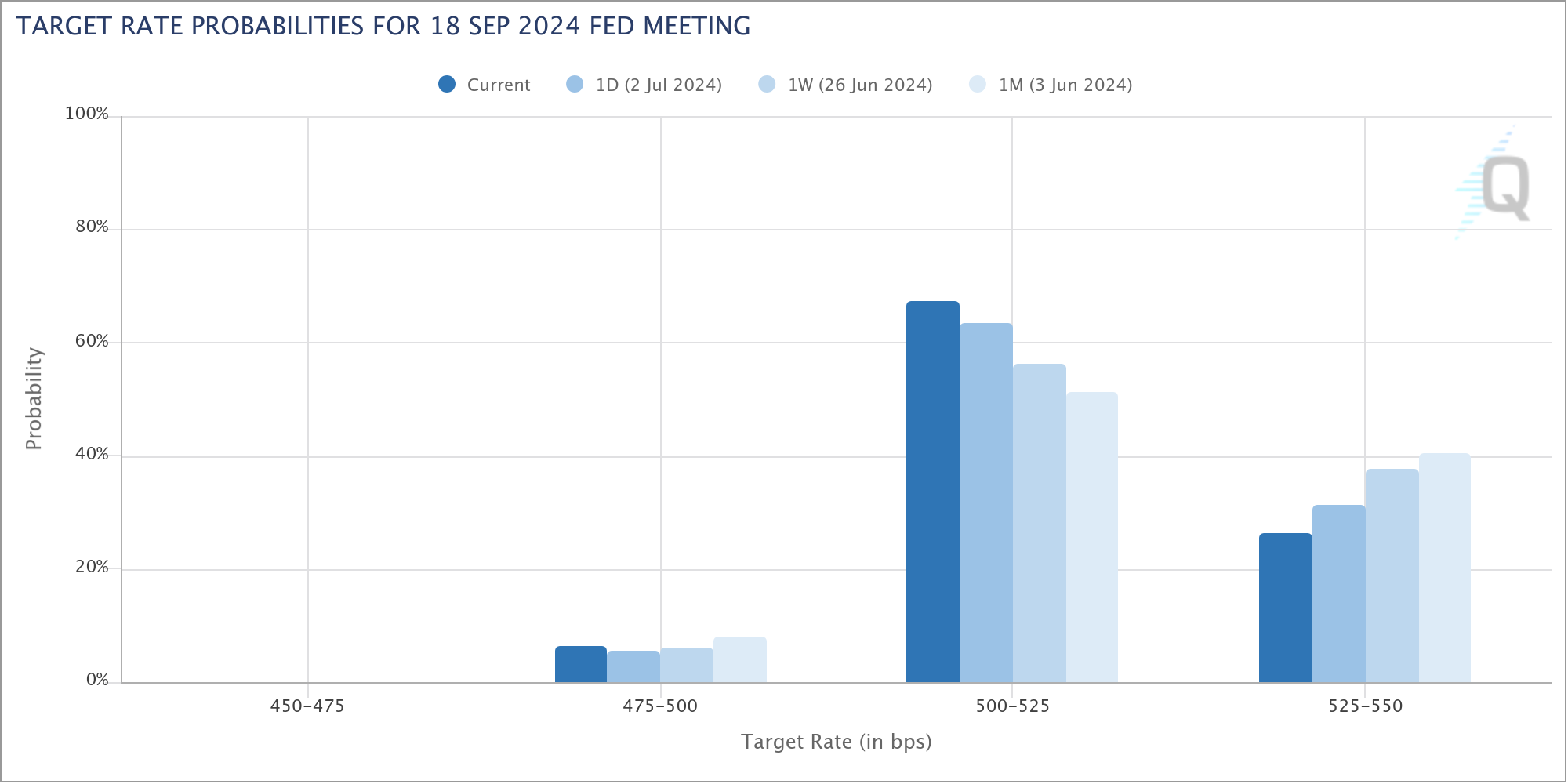

Markets focuses are on US Non-Farm Payroll report, a critical data release that could significantly influence market sentiment and monetary policy expectations. Dollar has been under selling pressure this week, driven by a series of disappointing economic data, particularly from ISM services. These developments have heightened expectations that Fed will begin cutting interest rates in September. Current fed funds futures suggest a nearly 73% probability of this outcome.

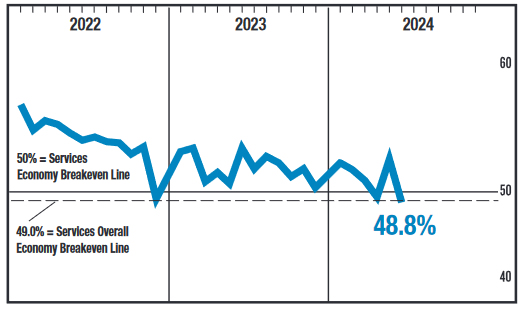

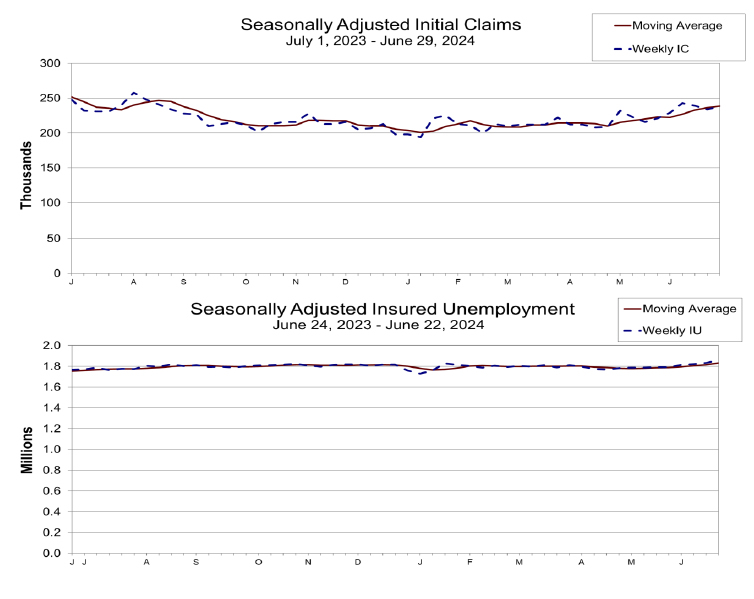

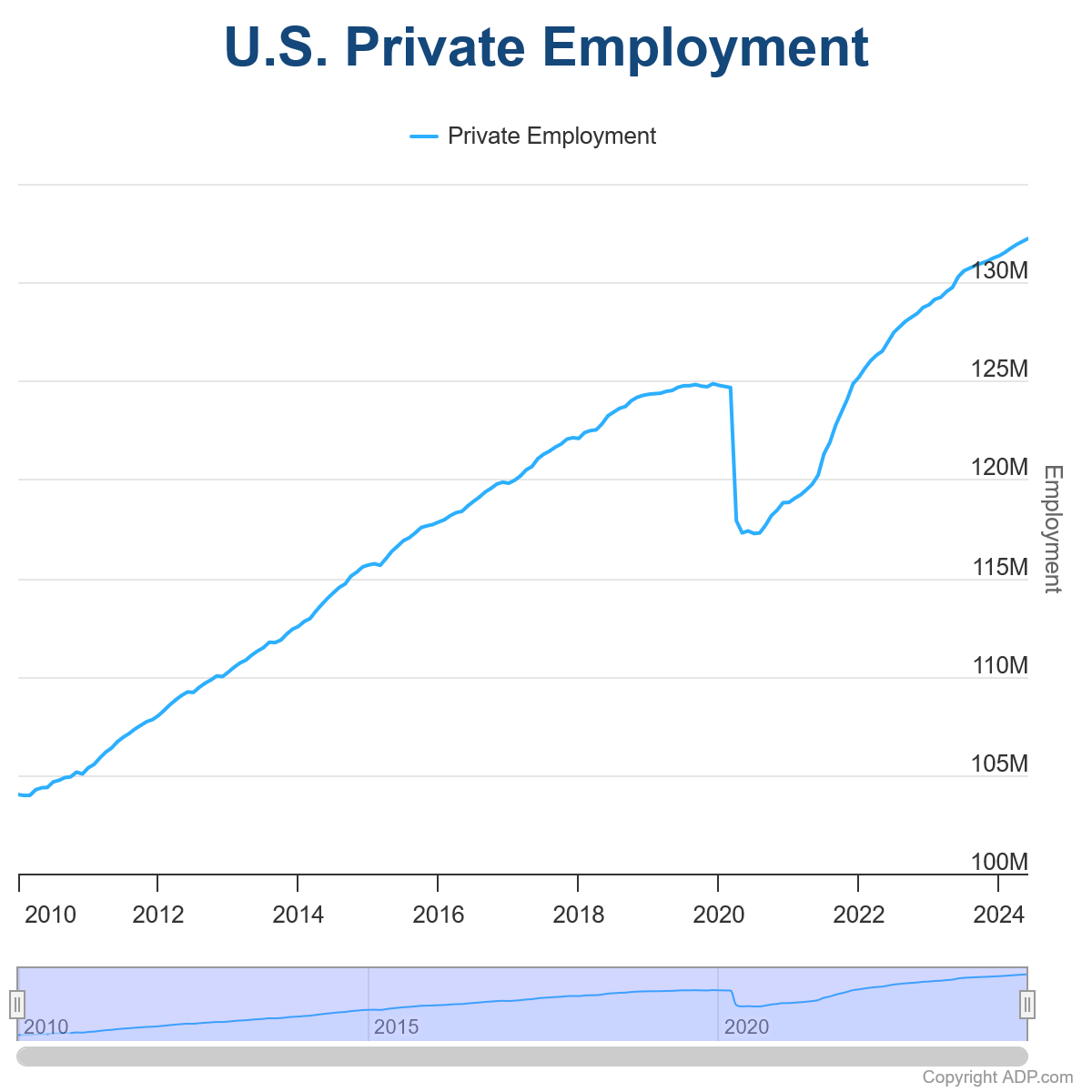

For June, markets are anticipating a headline job growth figure of 180k. Unemployment rate is expected to remain steady at 4.0%, while average hourly earnings are projected to increase by 0.3% mom. Recent economic indicators have painted a mixed picture: ISM Services Employment declined to 46.1 from 47.1, and ISM Manufacturing Employment fell to 49.3 from 51.1. ADP Employment report showed an addition of 150k net new jobs, and 4-week moving average of initial unemployment claims rose to 239,000, up from 222,000 last month, marking the highest level in ten months.

US stock markets have been responding to weak economic data with a “bad news is good news” attitude recently, where disappointing data increases the likelihood of an earlier rate cut by Fed. This sentiment is expected to persist with today’s NFP report. Market reactions could be pronounced, especially if unemployment rate rises or earnings growth falls short of expectations.

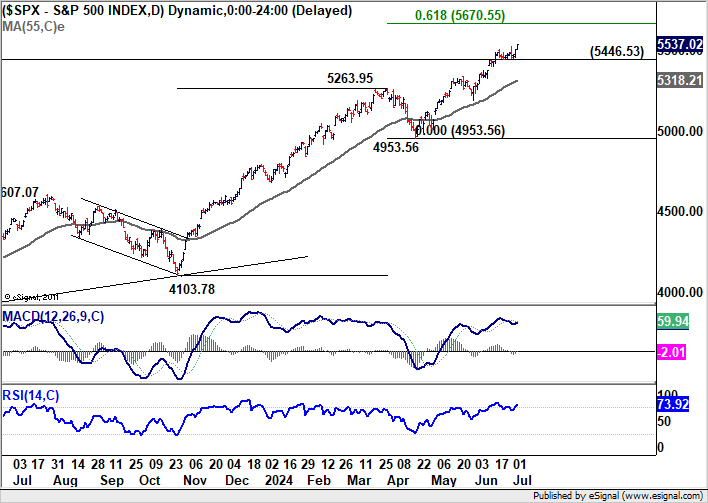

S&P 500 has been on a record-breaking run, and weaker-than-expected NFP report could further extend this rally. Current up trend is in progress for 61.8% projection of 4103.78 to 5263.95 from 4953.56 at 5670.55. Nevertheless, break of 5446.53 support will bring consolidations first, before extending the up trend at a later stage.

Eurozone retail sales rises 0.1% mom in May, EU up 0.1% mom too

Eurozone retail sales volume rose 0.1% mom in May, below expectation of 0.2% mom. Sales volume, increased by 0.7% mom for food, drinks, tobacco, and by 0.4% mom for automotive fuel in specialized stores. Sales volume fell -0.2% mom for non-food products (except automotive fuel).

EU retail sales also rose 0.1% mom. Among Member States for which data are available, the highest monthly increases in the total retail trade volume were recorded in Denmark (+2.3%), Lithuania (+1.8%) and Luxembourg (+1.7%). The largest decreases were observed in Slovakia (-1.0%), Ireland (-0.9%), Bulgaria and Malta (both -0.8%).

Full Eurozone retail sales here.